**WTMS Blog Today = What’s up in Mortgage Today (PM) – 05/29/2026**

Markets became skeptical of midday peace negotiations and proved right. Trump’s announcement of a final determination on Iran de-escalation initially drove yields to their weekly lows, but by day’s end no decision had materialized and bonds retreated to opening levels. The week brought solid economic data that surprised investors, with Chicago PMI crushing expectations at 62.7 versus a 50.5 forecast, while wholesale inventories came in softer at 0.5 percent against 0.8 percent consensus.

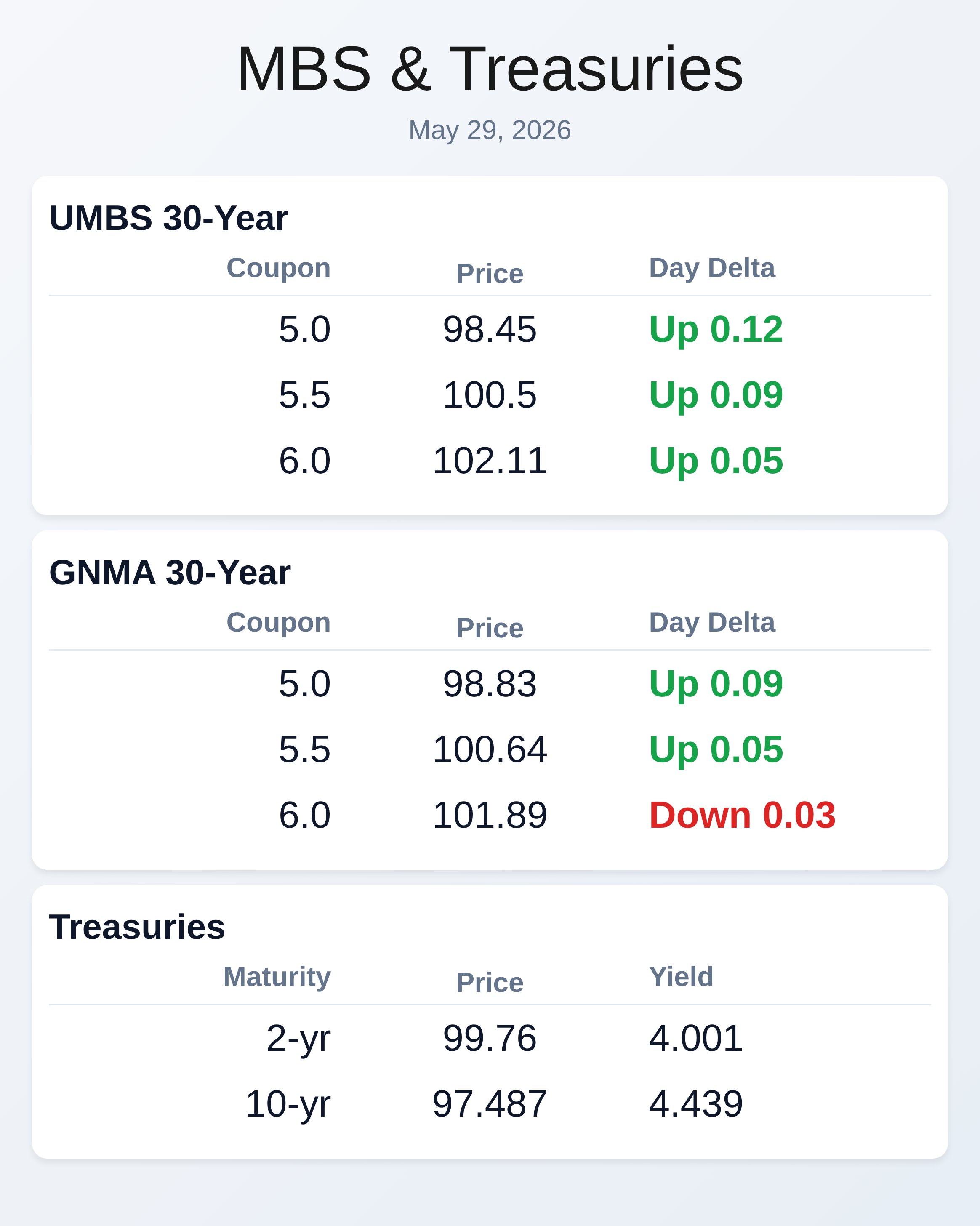

UMBS securities moved modestly higher, with 5.0 coupons gaining 12 basis points and 5.5 coupons up 9 basis points, reflecting cautious optimism on geopolitical resolution. Despite the headline volatility, mortgage originators should recognize that rates maintain upside potential once peace becomes official, suggesting modest caution on aggressive floating strategies remains justified. Property taxes and homeowners insurance have become the invisible affordability crisis plaguing borrowers and lenders alike.

Rising property taxes are climbing across every major metropolitan area, with some states seeing double-digit increases that add hundreds of monthly dollars to housing payments and compress qualification amounts for potential buyers. Insurance premiums continue their own upward march, creating a compound affordability squeeze that extends far beyond mortgage rates—the traditional focus of origination conversations. Loan officers increasingly must educate clients that the full cost of ownership now demands sophisticated budgeting and can significantly limit purchasing power even when rates improve.

This structural headwind deserves equal attention to rate strategies when managing expectations with purchase applicants, particularly in high-tax or high-insurance-cost regions where affordability barriers have dramatically worsened. Fair housing advocates filed a federal lawsuit challenging the Consumer Financial Protection Bureau’s elimination of disparate impact liability standards in Regulation B. The lawsuit, brought by the National Fair Housing Alliance and others, argues the May 2026 rule reversal dismantled 50 years of fair lending policy and left borrowers vulnerable to algorithmic discrimination.

Plaintiffs also challenge Acting Director Andrew Vought’s authority to issue the rule, questioning whether an unconfirmed official can legally lead the agency. The urban lending community should track this case closely, as any judicial reversal could restore disparate impact enforcement and create retroactive compliance exposure. Mortgage servicers and originators operating in protected-class markets should begin documenting AI decision-making processes now to prepare for potential reinstatement of these lending standards.

Urban Institute research shows the Federal Housing Administration could safely offer zero-down-payment mortgages to first-time homebuyers without materially increasing default risk or threatening the insurance fund. The analysis found moving from 96-99 percent loan-to-value to 100-104 percent LTV raises default probability by only 12 basis points—considered statistically insignificant by the authors. Restricting eligibility to borrowers with credit scores above 700 or those with 24 months of documented on-time rent payments would further limit risk exposure.

The study estimates that 6.5 million additional renter households could become qualified homebuyers if the down payment barrier were eliminated, potentially expanding the addressable market without fueling home price inflation. Such a program could represent a meaningful growth opportunity for originators positioned to compete in the first-time buyer segment, though it would require modest pricing adjustments—approximately 25 to 35 basis points in increased mortgage insurance—to keep FHA fund reserves whole. Median mortgage payments for purchase applicants climbed to $2,152 in April, up from $2,131 in March, as rates edged higher and loan sizes grew despite slightly softening economic data.

The payment increase reflects rising borrowing costs paired with persistent demand for larger loan amounts, though the April 2026 median remains $35 lower than April 2025 when accounting for concurrent income growth of approximately four percent. Geographic disparities in affordability remain stark, with Idaho, Nevada, and Rhode Island posting the highest payment-to-income ratios while Louisiana, Hawaii, and D.C. emerged as most affordable.

The mortgage Bankers Association noted that while affordability conditions weakened slightly, the trajectory year-over-year demonstrates improvement driven largely by rate compression and consistent wage growth. For originators managing capacity and pipeline mix, this data confirms that refinance demand will likely remain under pressure unless rates fall further, making purchase origination a more stable revenue driver in near-term planning. A new AI implementation at TD Bank demonstrates the transformative potential of large language models in mortgage operations, cutting traditional 15-hour document review and data extraction tasks down to just minutes.

The AI agent screens mortgage applications by analyzing documents, extracting relevant data, and performing verification, leaving final credit decisions to human adjudicators who now receive faster and more complete packages. TD deliberately selected mortgage processing because the workflow represents a well-defined, document-heavy task perfectly suited to LLM architecture, with numerical calculations routed to deterministic tools rather than AI inference. The success prompted the bank to plan broader AI transformation across its lending journey, with commercial real estate loans targeted next.

For mortgage servicing and origination platforms, this case study signals that immediate productivity gains are available in heavily-documents workflows—a critical advantage in rising-rate environments where operational efficiency directly impacts profit margins.

**Locking vs Floating**

Peace developments remain the critical rate driver, with improving geopolitical prospects suggesting rates have room to improve further once negotiations conclude officially. However, markets have repeatedly misjudged the timeline and substance of peace announcements, creating whipsaw risk that warrants cautious approach to aggressive floating positions.

Borrowers should consider locking in current levels if closing occurs within 30 days, while those with longer timelines can monitor geopolitical headlines and consider floating if confidence in de-escalation strengthens with concrete outcomes rather than negotiation updates alone.

**Today’s Events**

Wholesale Inventories: 0.5 versus 0.8 forecast, 1.3 previous

Chicago PMI: 62.7 versus 50.5 forecast

**Bond Pricing**

**UMBS 30 yr**

| Coupon | Price | Intra-Day Change |

**GNMA 30 yr**

| Coupon | Price | Intra-Day Change |

**Treasuries**

| Term | Yield | Price | Intra-Day Yield Change |

| 2 yr | 4.001 | 99.76 | -0.023 |

| 10 yr | 4.439 | 97.487 | -0.012 |

| 30 yr | 4.976 | 96.496 | -0.003 |