WTMS Blog Today = What’s up in Mortgage Today (AM) – 02/23/2026

Markets woke up to a tariff ruling that briefly rattled traders but ultimately failed to derail the bond rally. Despite headline noise about trade policy changes, mortgage-backed securities held their ground with modest gains across all coupons. The 10-year Treasury yield dropped 20 basis points to 4.064%, creating a window of opportunity for originators looking to improve their rate sheets.

Economic data painted a mixed picture that kept Fed watchers on edge. Core PCE inflation came in hotter than expected at 0.4% monthly and 3.0% annually, both above forecasts and signaling persistent price pressures. However, GDP growth disappointed dramatically at just 1.4% versus the 3.0% expectation, suggesting the economy may be cooling faster than anticipated.

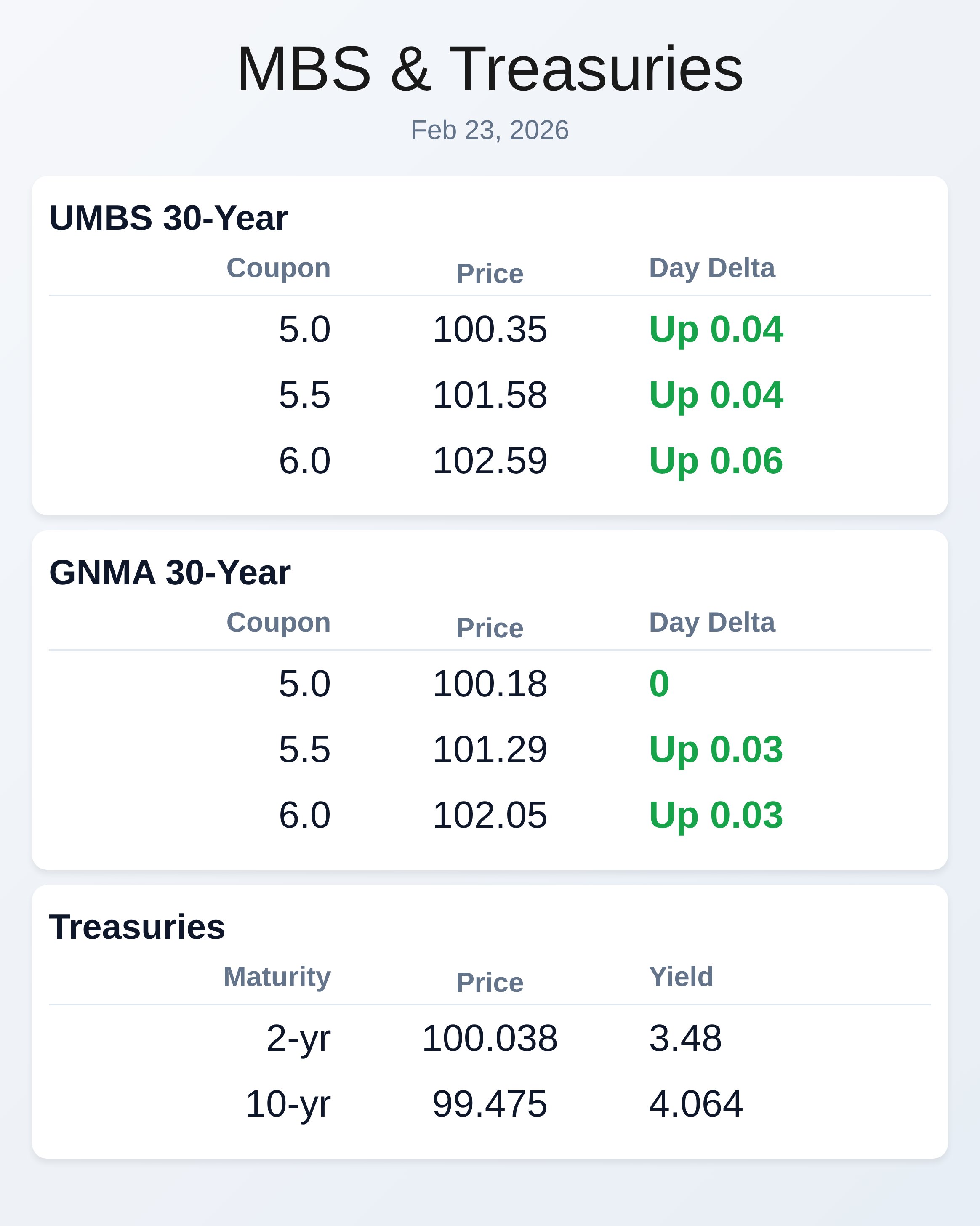

UMBS prices posted solid gains with the 6.0 coupon leading the charge at +0.06 points. The 5.5 and 5.0 coupons both added 0.04 points, reflecting steady demand for mortgage securities. This strength should translate into improved pricing for loan officers by midday.

Treasury yields fell across the entire curve with longer-term bonds showing the most improvement. The 30-year bond yield dropped 12 basis points to 4.712%, while the critical 10-year note declined 20 basis points. These moves typically signal rate sheet improvements within the next trading session.

Locking vs Floating

The current environment favors cautious optimism for floating borrowers with longer closing timelines. Core PCE inflation running above expectations at 3.0% annually keeps Fed rate cut hopes in check, but the dramatic GDP slowdown to 1.4% suggests economic weakness may force the central bank’s hand. Loans closing within two weeks should consider locking given the volatile economic crosscurrents.

The upcoming week features lighter economic data, but political developments around tariff policies could inject unexpected volatility. MBS prices provide good intraday risk management tools, while 10-year yield levels help track broader bond market momentum for longer-term positioning decisions.

Today’s Events

– Core PCE (m/m) (Dec): 0.4% vs 0.3% forecast, 0.2% previous

– Core PCE (y/y) (Dec): 3.0% vs 2.9% forecast, 2.8% previous

– Core PCE Prices Q/Q Q4: 2.7% vs 2.6% forecast, 2.9% previous

– GDP Q4: 1.4% vs 3% forecast, 4.4% previous

– GDP Final Sales Q4: 1.2% vs — forecast, 4.5% previous

– PCE (y/y) (Dec): 2.9% vs 2.8% forecast, 2.8% previous

– PCE prices (m/m) (Dec): 0.4% vs 0.3% forecast, 0.2% previous

– PCE Prices (Q/Q) Q4: 2.9% vs 2.8% forecast, 2.8% previous

Bond Pricing

UMBS 30 yr

| Coupon | Price | Intra-Day Change |

| 5.0 | 100.35 | 0.04 |

| 5.5 | 101.58 | 0.04 |

| 6.0 | 102.59 | 0.06 |

GNMA 30 yr

| Coupon | Price | Intra-Day Change |

| 5.0 | 100.18 | 0 |

| 5.5 | 101.29 | 0.03 |

| 6.0 | 102.05 | 0.03 |

Treasuries

| Term | Yield | Price | Intra-Day Yield Change |

| 2 yr | 3.48 | 100.038 | 0 |

| 3 yr | 3.491 | 100.024 | -0.01 |

| 5 yr | 3.629 | 100.548 | -0.019 |

| 7 yr | 3.828 | 101.05 | -0.021 |

| 10 yr | 4.064 | 99.475 | -0.02 |

| 30 yr | 4.712 | 98.613 | -0.012 |