WTMS Blog Today = What’s up in Mortgage Today (AM) – 03/09/2026

Oil prices are wreaking havoc on mortgage markets this morning as geopolitical tensions in Iran drive crude to $118 before pulling back. UMBS securities are down roughly a quarter point while the 10-year Treasury yield spiked to 4.21% overnight before settling at 4.17%.

This represents a 17 basis point climb over just the past week, directly translating to higher mortgage rates for your borrowers. The Strait of Hormuz closure has essentially halted oil tanker traffic, creating the strongest correlation yet between rising oil prices and climbing bond yields. While Europe and China face actual supply shortages, the US relies primarily on domestic West Texas Intermediate crude.

The good news is that numerous previously drilled wells become economically viable at these price levels, meaning domestic supply will increase if prices remain elevated. Stock markets are taking it on the chin with the Dow falling 1.6% and small-cap Russell 2000 dropping nearly 2%. Rising Treasury yields are pressuring equities as investors grow increasingly skeptical about multiple rate cuts materializing this year.

The combination of elevated energy prices and persistent inflation is forcing traders to recalibrate their Federal Reserve expectations. Fed chair nominee Kevin Warsh may provide some relief down the road, as he’s argued that inflation stems primarily from fiscal policy and money supply rather than energy shocks. This suggests he might still pursue rate cuts once confirmed despite the oil price surge.

However, the FOMC’s immediate focus remains locked on labor market strength, especially after February’s disappointing employment report. February’s jobs data revealed the economy shed 92,000 positions, with the prior two months revised lower by a combined 69,000. The rolling three-month average now shows only 6,000 jobs added per month.

The unemployment rate ticked up to 4.44%, though population estimate revisions affected this figure. Retail sales present a mixed picture with January down 0.2% overall, but the control group that aligns with GDP calculations rose 0.4%. Credit card transaction data and winter weather impacts suggest February retail numbers won’t show much improvement.

Both ISM surveys remained in expansion territory during February, with gains in new orders and production providing some economic bright spots. The refinance opportunity window could open wider with modest rate declines across different loan types. In conventional 30-year mortgages, rates near 5.90% would put roughly $153 billion in borrower balances on the cusp of refinancing.

A drop to 5.75% would expand the incentive pool by 2.9% of total unpaid principal balance, particularly benefiting servicers like Rocket, Lakeview, and Pennymac. FHA borrowers show even greater rate sensitivity, with similar rate declines potentially expanding refinance eligibility by 6.5% of unpaid balances. Freedom, NewRez, and Pennymac stand to capture the largest incremental gains in this segment.

VA loans already enjoy lower prevailing rates, meaning a move to 5.5% opens approximately $34 billion to refinancing, while reaching 5.25% could unlock an additional $64 billion. This week’s economic calendar is loaded with market-moving data including NFIB Small Business Optimism, Existing Home Sales, CPI, housing starts and permits, personal income and spending, PCE, and Q4 GDP revisions. Treasury auctions of 3-year and 10-year notes will also command attention.

With no major economic releases scheduled for today, oil price movements remain the primary driver of bond market direction. The US Navy’s plan to shepherd tankers through the Strait should help stabilize global supply over time. However, the longer this conflict persists, the worse it becomes for commodity prices and consumer confidence.

Summer driving season is approaching, and elevated gas prices will directly impact borrower psychology and purchasing power. Housing affordability continues deteriorating as some buyers resort to draining their 401(k) accounts for down payments. The widening gap between home prices and income represents one of the biggest obstacles facing potential homebuyers today.

This desperation move signals just how challenging the purchase market has become for first-time buyers.

Locking vs Floating

Volatility risk remains substantially elevated due to the dual pressures of geopolitical uncertainty and this week’s heavy economic data schedule. The overnight oil spike pushed 10-year yields to 4.21% before retreating to current levels around 4.17%.

MBS prices provide some intraday risk management, but the 10-year yield ceilings and floors offer better guidance for tracking broader bond market momentum over longer timeframes.

Today’s Events

No economic data releases scheduled for today.

Bond Pricing

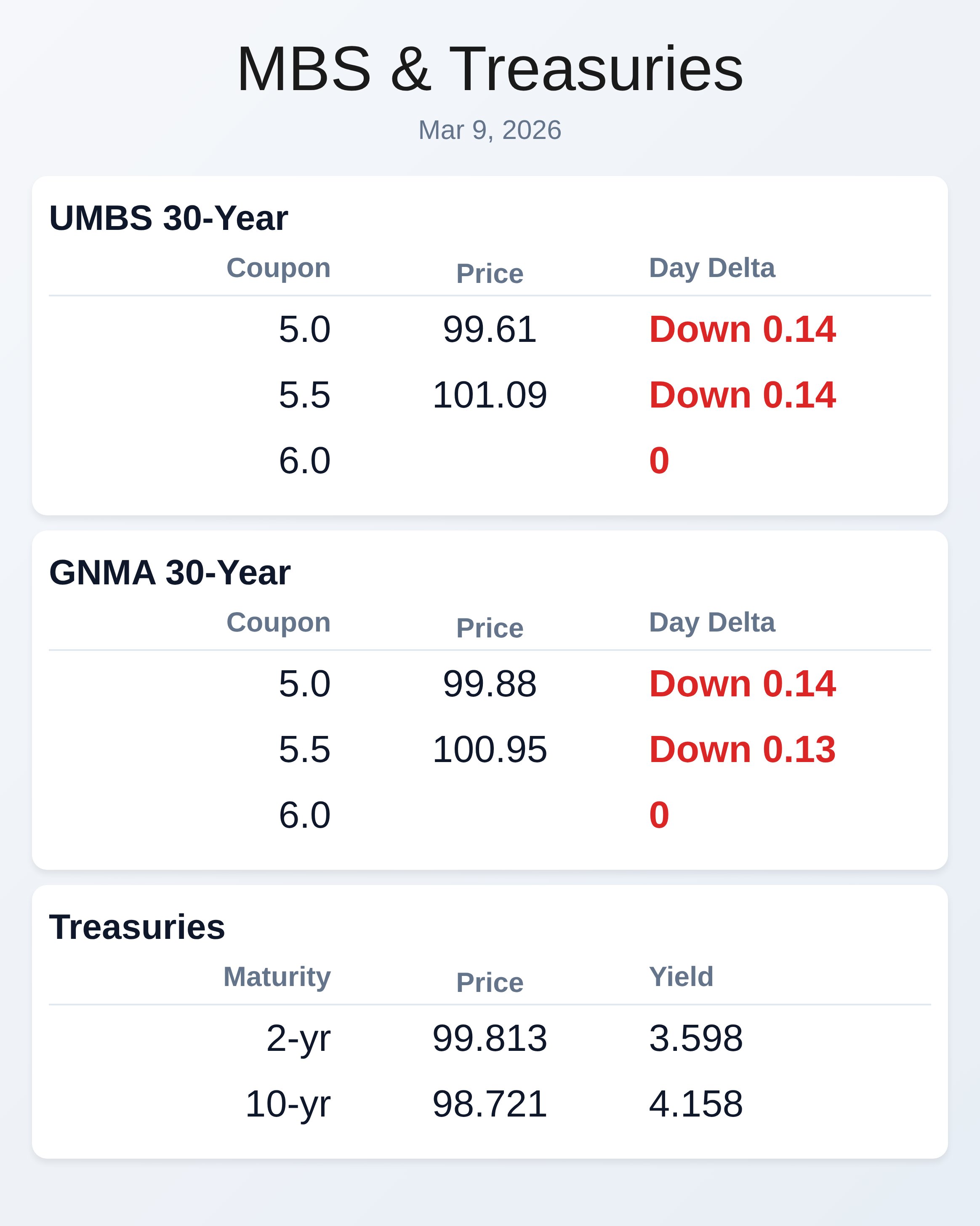

UMBS 30 yr

| Coupon | Price | Intra-Day Change |

GNMA 30 yr

| Coupon | Price | Intra-Day Change |

Treasuries

| Term | Yield | Price | Intra-Day Yield Change |

UMBS 30 yr

| Coupon | Price | Intra-Day Change |

| 4.5 | 97.59 | -0.20 |

| 5.0 | 99.61 | -0.14 |

| 5.5 | 101.09 | -0.14 |

GNMA 30 yr

| Coupon | Price | Intra-Day Change |

| 4.5 | 97.89 | -0.12 |

| 5.0 | 99.88 | -0.14 |

| 5.5 | 100.95 | -0.13 |

Treasuries

| Term | Yield | Price | Intra-Day Yield Change |

| 2 yr | 3.598 | 99.813 | 0.048 |

| 3 yr | 3.62 | 99.661 | 0.045 |

| 5 yr | 3.751 | 99.996 | 0.026 |

| 7 yr | 3.946 | 100.329 | 0.033 |

| 10 yr | 4.158 | 98.721 | 0.028 |

| 30 yr | 4.77 | 97.707 | 0.005 |

Subscribe free at WellThatMakesSense.com to get this in your inbox daily.