WTMS Blog Today = What’s up in Mortgage Today (AM) – 03/12/2026

Geopolitical tensions just slammed the mortgage market with MBS dropping an eighth of a point in minutes. President Trump’s comments about prioritizing stopping Iran over oil prices triggered immediate bond selling, followed by Iran’s Khamenei announcing the Strait of Hormuz should remain closed. UMBS 5.0 coupons fell to 99.15, down 12 ticks, while the 10-year Treasury yield spiked 2.2 basis points to 4.248%.

Early-pricing lenders are already eyeing negative reprices as volatility continues to dominate March trading. This morning’s economic data painted a mixed housing picture that markets largely ignored amid the geopolitical chaos. Housing starts jumped 7.2% month-over-month to 1.487 million units, beating expectations and showing 9% year-over-year growth.

Building permits disappointed at 1.376 million, down 5.4% and missing forecasts. Weekly jobless claims hit 213,000 as expected, while the January trade deficit narrowed significantly to $54.5 billion from $70.3 billion, driven by a surge in exports. Yesterday’s rate deterioration felt more severe than typical daily swings due to technical factors in mortgage pricing.

The 10-year Treasury yield broke decisively above the closely watched 4.20% level, triggering widespread bond selling that hit MBS even harder than Treasuries. Many mortgage securities are trading near par value, meaning their pricing relies heavily on interest-only valuations that amplify rate movements when markets shift quickly. The widening spread between MBS and Treasury prices forced lenders to reprice for the worse to protect margins.

Oil prices are driving inflation concerns as crude has surged 25% since late February amid the Iran conflict. The February CPI report offered no relief on inflation, coming in as expected and reinforcing that disinflationary progress has stalled. Core Personal Consumption Expenditure is expected to post another solid 0.4% monthly gain when it prints tomorrow.

Despite inflation pressures, the Federal Reserve is still expected to deliver two modest rate cuts later this year while focusing primarily on energy dynamics and geopolitical risks. March has been relentlessly bearish for mortgage rates with yields climbing across the curve. Treasury yields closed above their 200-day moving averages yesterday after weak demand at a $39 billion 10-year note reopening.

Today brings a $22 billion reopened 30-year bond auction and remarks from Fed Vice Chair Bowman on Basel III bank capital rules. The New York Fed will also conduct a buyback operation for $4 billion in 7-year to 10-year coupons to support liquidity.

Locking vs Floating

Volatility risk remains significantly elevated due to ongoing geopolitical uncertainty surrounding the Iran conflict and potential Strait of Hormuz disruptions.

March has delivered consistent selling pressure for rates without any clear signs of leveling off. Given the heightened risk environment and bearish momentum, defensive postures make sense until this negative trend shows clear signs of stabilization. Markets are reacting sharply to headlines, making float strategies particularly risky in the current environment.

Today’s Events

Building Permits (Jan): 1.376M vs 1.41M forecast, 1.455M previous

Continued Claims (Feb 28): 1,850K vs 1,850K forecast, 1,868K previous

Housing Starts (Jan): 1.487M vs 1.35M forecast, 1.404M previous

Jobless Claims (Mar 7): 213K vs 215K forecast, 213K previous

Trade Gap (Jan): -$54.50B vs -$66.6B forecast, -$70.3B previous

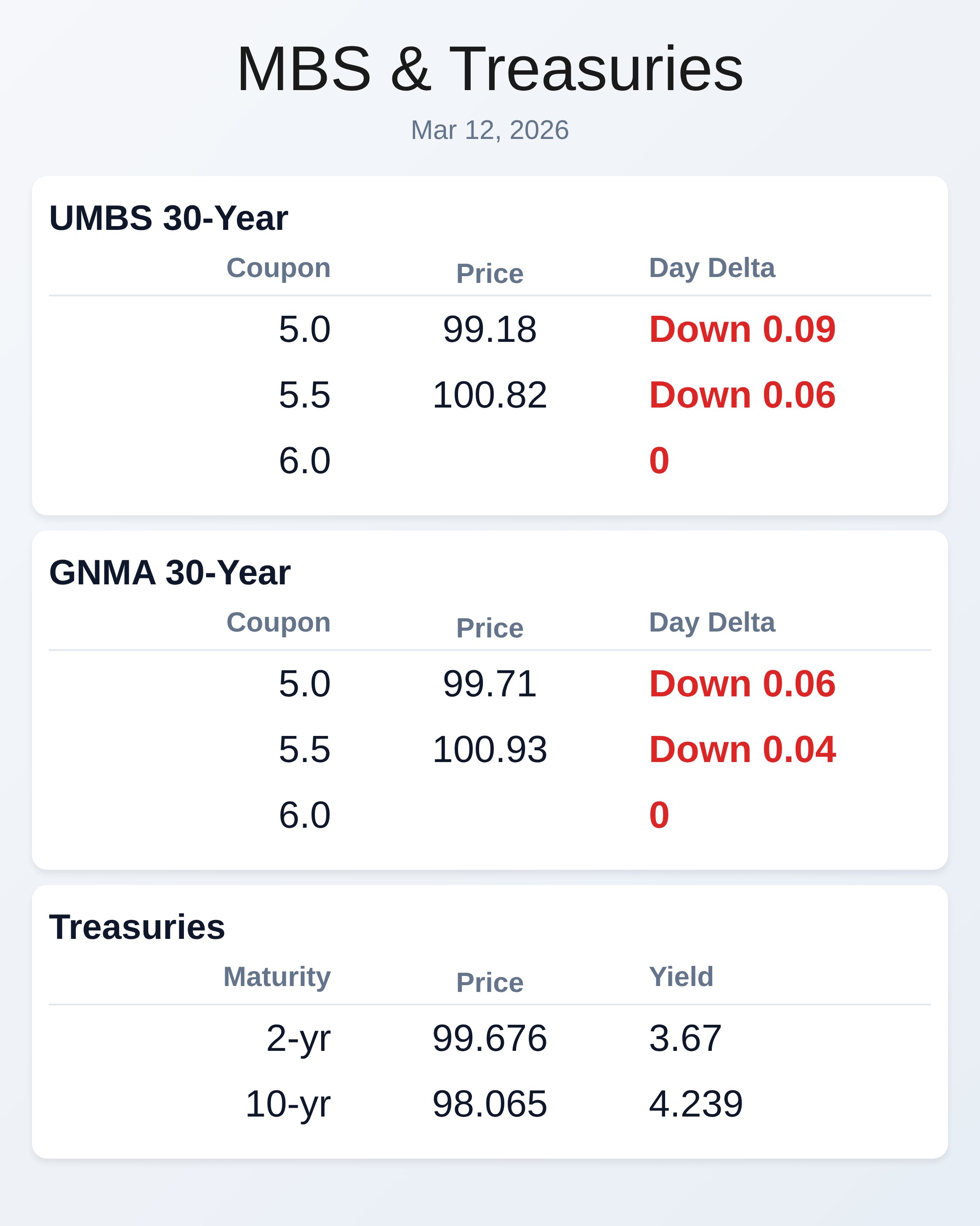

Bond Pricing

UMBS 30 yr

| Coupon | Price | Intra-Day Change |

| 5.0 | 99.18 | -0.09 |

| 5.5 | 100.82 | -0.06 |

| 5.0 | 99.71 | -0.06 |

GNMA 30 yr

| Coupon | Price | Intra-Day Change |

Treasuries

| Term | Yield | Price | Intra-Day Yield Change |

| 2 yr | 3.67 | 99.676 | 0.019 |

| 3 yr | 3.69 | 99.465 | 0.013 |

| 5 yr | 3.818 | 99.692 | 0.013 |

| 7 yr | 4.018 | 99.893 | 0.011 |

| 10 yr | 4.239 | 98.065 | 0.012 |

| 30 yr | 4.886 | 95.92 | 0.003 |