WTMS Blog Today = What’s up in Mortgage Today (AM) – 03/18/2026

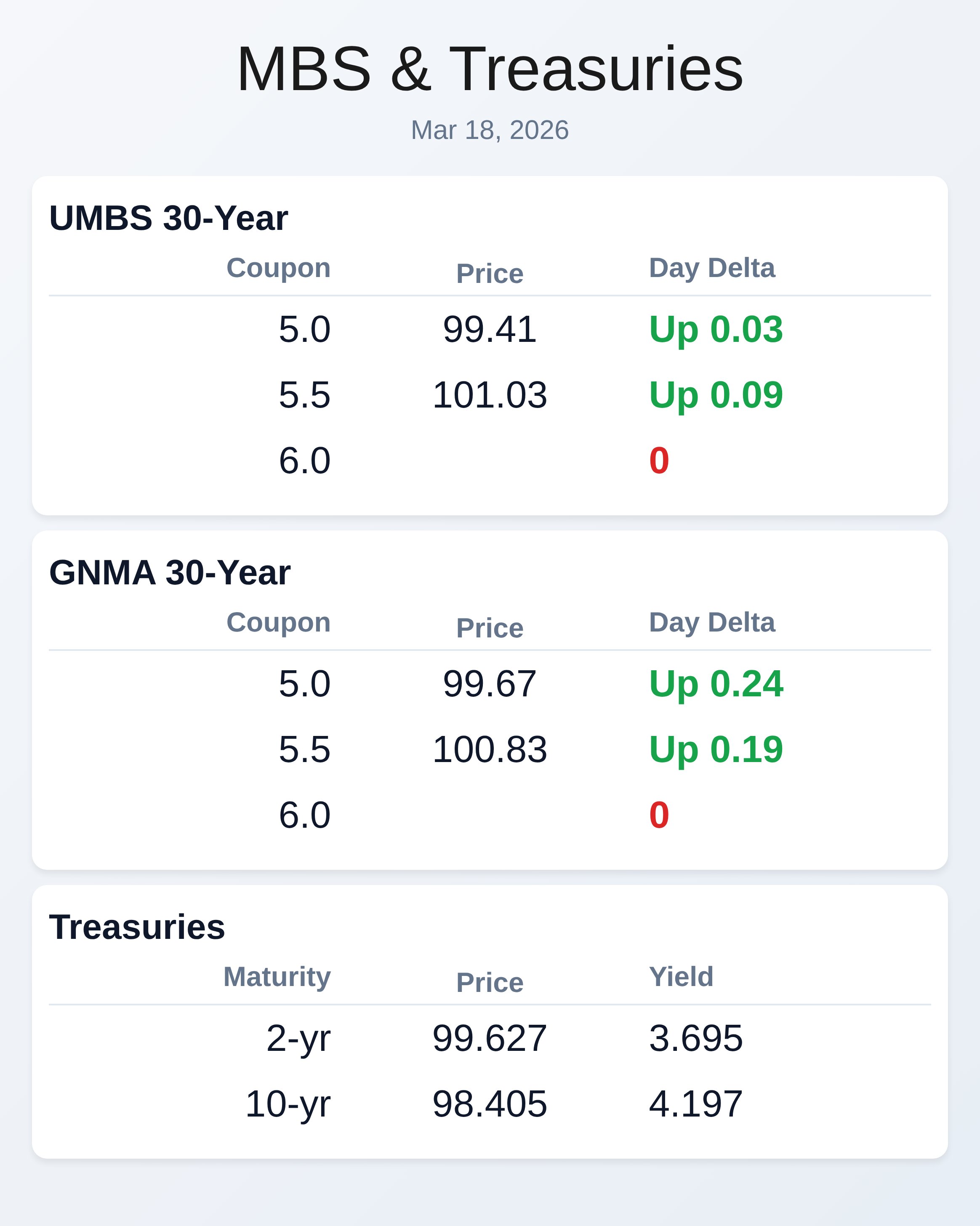

Markets are grinding through a sleepy pre-Fed day with modest gains across mortgage-backed securities despite disappointing manufacturing data. UMBS 30-year coupons posted small gains with the 5.5 coupon up 9 basis points, while GNMA securities showed even stronger performance with the 5.0 coupon climbing 24 basis points. The 10-year Treasury yield held relatively steady at 4.197%, down just 2 basis points intraday, as traders position defensively ahead of this afternoon’s Federal Reserve announcement.

Refinance demand collapsed last week, plunging 19% overall and 27% for conventional refinances as the 30-year fixed rate spiked to 6.30% from 6.19% the prior week. Geopolitical tensions surrounding the Iran conflict drove oil prices higher and rattled Treasury markets, pushing rates to their highest levels in weeks. Purchase applications managed a modest 1% gain and remain 12% above last year’s levels, offering a sliver of optimism as the spring buying season approaches.

Rates have edged slightly lower to start this week, but volatility remains elevated with all eyes on Fed Chair Powell’s commentary later today. The NY Fed manufacturing index came in at -0.2 versus a forecast of 3.2 and well below the prior reading of 7.1, signaling continued weakness in the manufacturing sector. This disappointing data initially provided modest support for bonds, though the market remains hesitant to make significant moves ahead of the Fed meeting.

While no rate cut is expected today, Powell’s tone regarding inflation concerns and the geopolitical risk premium could determine whether recent rate weakness continues or if we see renewed pressure. The manufacturing decline adds to concerns about tariff impacts on materials costs and supply chain disruptions affecting homebuilders. A federal judge delivered a significant ruling for mortgage originators who rely on CFPB data and oversight, ordering the agency to continue drawing funding from the Federal Reserve.

Acting director Russell Vought had attempted to effectively shutter the agency by arguing it couldn’t receive funding unless the Fed was profitable, a move the judge called “arbitrary, capricious and in violation of law.” Three nonprofits sued after the funding cutoff threatened to eliminate critical lending data used to track fair lending practices and compliance metrics that many lenders depend on for regulatory monitoring. Homebuilder sentiment inched up one point to 38 in March but remains below the critical 50 break-even threshold for the 23rd consecutive month, reflecting ongoing affordability challenges. Nearly two-thirds of builders continue offering sales incentives while 37% are cutting prices with average discounts holding at 6%, creating potential opportunities for purchase loan volume.

Tariffs on materials and appliances are squeezing builder margins while immigration enforcement at construction sites has thinned the available labor pool, driving up costs. NAHB Chief Economist Robert Dietz noted that down-payment hurdles and uncertainty from the Iran conflict will act as headwinds, though recent executive orders aimed at reducing regulatory burdens could eventually help increase attainable housing supply. NAR reported pending home sales rose 1.8% in February, offering another modestly positive data point for purchase mortgage volume heading into spring.

Meanwhile, Freedom Mortgage’s parent company struck a deal to acquire Seneca Mortgage Servicing, expanding their MSR platform as servicing rights continue to attract investor interest in a high-rate environment. On the real estate side, Zillow launched “Zillow Preview,” allowing brokerages to share listings publicly before they hit the MLS through a direct entry system that bypasses traditional MLS workflows, potentially changing how quickly purchase opportunities reach borrowers.

Locking vs Floating

Volatility risk remains elevated due to ongoing geopolitical uncertainty, with the entire month of March proving bearish for rates.

Market participants should maintain a defensive posture until the bearish trend clearly levels off, which will require more than two positive days given the false hope created by brief rallies on March 6th and 9th. With the Fed announcement looming this afternoon and rate momentum still negative, locking makes sense for loans closing within the next 15-30 days.

Today’s Events

– NY Fed Manufacturing Index: -0.2 vs 3.2 forecast, 7.1 previous

– 2:00 PM: FOMC Rate Decision (no change expected)

– 2:30 PM: Fed Chair Powell Press Conference

Bond Pricing

UMBS 30 yr

| Coupon | Price | Intra-Day Change |

GNMA 30 yr

| Coupon | Price | Intra-Day Change |

Treasuries

| Term | Yield | Price | Intra-Day Yield Change |

UMBS 30 yr

| Coupon | Price | Intra-Day Change |

| 4.5 | 97.44 | 0.06 |

| 5.0 | 99.41 | 0.03 |

| 5.5 | 101.03 | 0.09 |

GNMA 30 yr

| Coupon | Price | Intra-Day Change |

| 4.5 | 97.39 | 0.1 |

| 5.0 | 99.67 | 0.24 |

| 5.5 | 100.83 | 0.19 |

Treasuries

| Term | Yield | Price | Intra-Day Yield Change |

| 2 yr | 3.695 | 99.627 | 0.02 |

| 3 yr | 3.693 | 99.456 | 0.016 |

| 5 yr | 3.793 | 99.805 | -0.001 |

| 7 yr | 3.98 | 100.121 | -0.001 |

| 10 yr | 4.197 | 98.405 | -0.002 |

| 30 yr | 4.834 | 96.713 | -0.009 |

Subscribe free at WellThatMakesSense.com to get this analysis in your inbox daily.