WTMS Blog Today = What’s up in Mortgage Today (AM) – 03/19/2026

Fed Holds, Market Freaks

The Federal Reserve held rates steady at 3.50 to 3.75 percent yesterday while Chair Powell acknowledged rising energy prices will add near-term inflationary pressure, pushing rate-cut expectations further into the future. Updated dot plot projections showed a modestly more inflationary outlook with a growing share of policymakers expecting just one cut this year or none at all. The Fed remains firmly in wait-and-see mode as it balances sticky inflation against a gradually cooling economy.

Powell’s measured tone avoided signaling any urgency, reinforcing the “higher for longer” narrative that’s now rattling markets. Odds of an April rate hike jumped from 4 percent to over 10 percent this morning, reflecting how dramatically sentiment has shifted. Bonds Ignore Oil, Focus on Rate Repricing

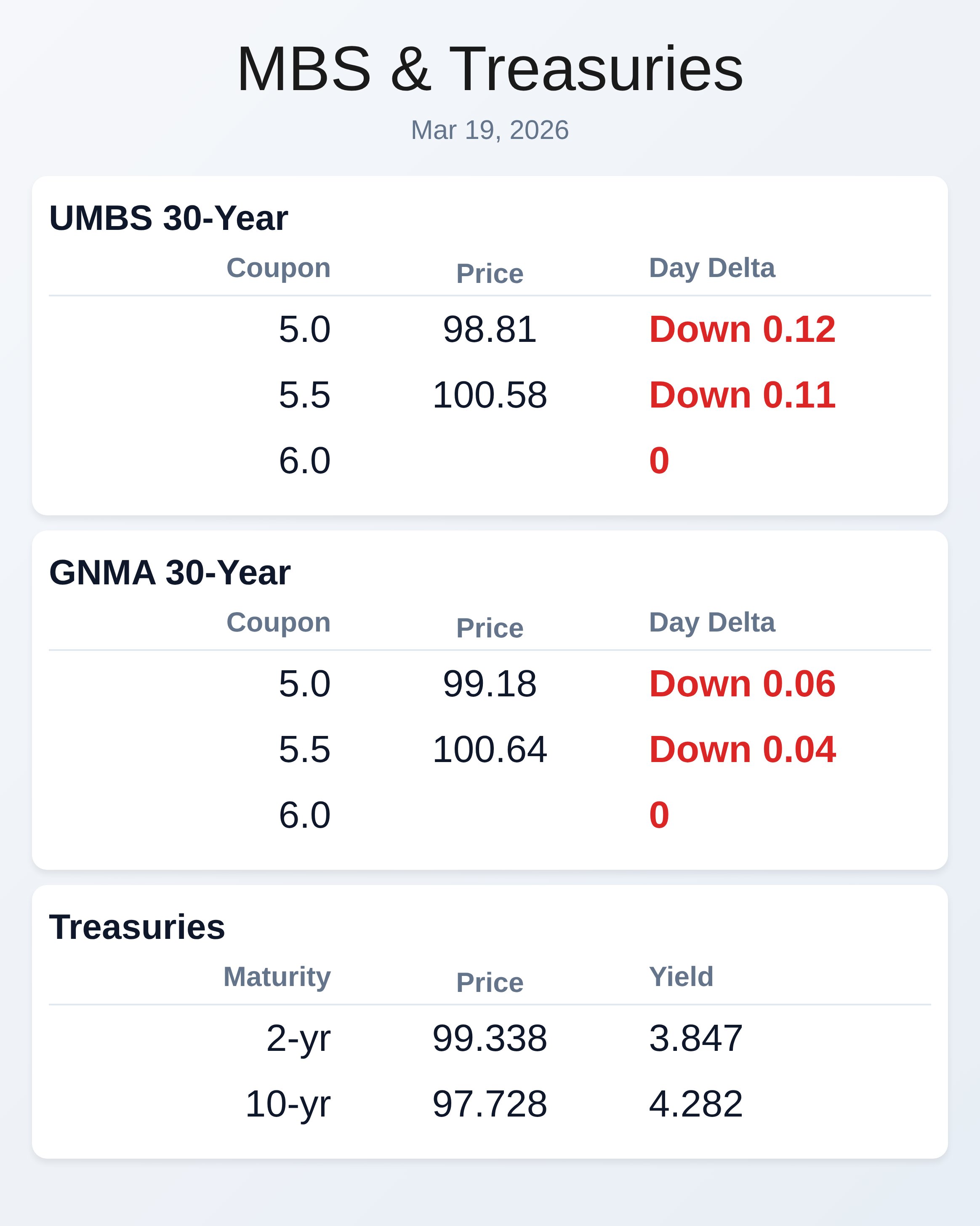

UMBS prices dropped another 12 to 26 basis points overnight while the 10-year Treasury yield climbed to 4.31 percent, continuing Wednesday’s selloff after a hotter-than-expected PPI report.

Throughout March, the “10-year versus oil price” chart has shown enough correlation to blame the bond rout on surging energy costs, but today oil traded flat while bonds sold off hard. The 2-year Treasury took the worst hit with yields surging to 3.92 percent, reflecting a rapidly changing outlook for Fed Funds. This large-scale repositioning for higher short-term rates is drowning out both oil price movements and economic data.

The market is repricing risk around sticky inflation and a stagflationary mix that keeps sentiment deeply cautious. Energy Attacks Fuel Stagflation Fears

Global stocks extended losses as Brent crude climbed toward $113 per barrel following attacks on critical Middle East energy infrastructure, pushing oil gains since the conflict began past 55 percent. Saudi Arabia reported a drone strike on its Samref refinery after Israel hit Iran’s South Pars gas field, with Iran retaliating against Qatar’s largest LNG export plant.

European natural gas jumped as much as 35 percent while European equities fell 2.1 percent to their lowest level this year. Higher fuel and diesel costs are filtering through transportation channels into consumer prices, with history suggesting these effects linger even after energy shocks fade. President Trump called on Israel and Iran to stop attacking energy infrastructure, but the risk of lasting damage continues to escalate.

Jobs Data and Manufacturing Beat Expectations

Weekly jobless claims fell 8,000 to 205,000 versus the 215,000 forecast, while continuing claims rose slightly to 1.857 million for the week ending March 7. The Philadelphia Fed Business Index surged to 18.1, crushing the forecast of 10.0 and up from 16.3 previously. More concerning for inflation hawks, the Philly Fed Prices Paid component jumped to 44.70 from 38.90, signaling accelerating input costs for manufacturers.

The labor market remains resilient with the four-week moving average for claims at just 210,750. These stronger-than-expected figures reinforce the Fed’s cautious stance and support the case for keeping rates higher for longer. Global Central Banks Stay Unanimous

The Bank of England and Bank of Japan both held rates unchanged Thursday, following the Fed’s lead and signaling that the Middle East conflict has clouded the policy outlook.

UK policymakers voted unanimously to hold with all members standing “ready to act” to contain inflation, sending 2-year gilt yields up 28 basis points to 4.38 percent, the highest since January 2025. Traders are now fully pricing in two rate hikes by both the European Central Bank and Bank of England this year, a dramatic reversal from recent expectations. The ECB announces its decision later today after Swiss and Swedish policymakers also held steady.

Money markets now see just a 40 percent chance of a quarter-point Fed cut this year, down from 55 percent yesterday. Mortgage Markets Brace for More Volatility

Agency MBS prices worsened another 12 to 25 basis points today with all coupons under pressure as the repricing continues. The 2-year versus 10-year yield curve shifts reflect investors repositioning for an extended period of elevated short-term rates.

Today’s calendar includes delayed new home sales data for January, wholesale inventories, Treasury announcing month-end supply totaling $211 billion across multiple maturities, and a $19 billion reopened 10-year TIPS auction. The toxic mix of geopolitics, sticky inflation, and hawkish central bank messaging has mortgage originators in full risk-off mode. With March shaping up as a one-way trade for bonds punctuated by brief corrective moments, the dust needs to settle before anyone takes major risks with float strategies.

Locking vs Floating

The Fed’s reaction added more volatility than expected to an already turbulent environment driven by geopolitical uncertainty and the energy price collapse. All of March has been essentially a one-way losing trade for bonds with only a few small corrective bounces. Risks remain elevated as the market reprices rate expectations higher while oil-driven inflation concerns mount.

The recommendation is to continue waiting for the dust to definitively settle before taking any major risks with floating, as the current environment favors defensive positioning and locking strategies.

Today’s Events

Jobless Claims (Mar 14): 205K vs 215K forecast, 213K prior

Continued Claims (Mar 7): 1,857K vs 1,850K forecast, 1,850K prior

Philly Fed Business Index (Mar): 18.1 vs 10.0 forecast, 16.3 prior

Philly Fed Prices Paid (Mar): 44.70 vs 38.90 prior

New Home Sales (Jan): 0.72M forecast, 0.745M prior

Bond Pricing

UMBS 30 yr

| Coupon | Price | Intra-Day Change |

| 5.0 | 98.81 | -0.12 |

| 5.5 | 100.58 | -0.11 |

| 5.0 | 99.18 | -0.06 |

GNMA 30 yr

| Coupon | Price | Intra-Day Change |

Treasuries

| Term | Yield | Price | Intra-Day Yield Change |

| 2 yr | 3.847 | 99.338 | 0.077 |

| 3 yr | 3.842 | 99.039 | 0.066 |

| 5 yr | 3.92 | 99.237 | 0.043 |

| 7 yr | 4.091 | 99.453 | 0.032 |

| 10 yr | 4.282 | 97.728 | 0.021 |

| 30 yr | 4.866 | 96.212 | -0.017 |