—

WTMS Blog Today = What’s up in Mortgage Today (AM) – 03/23/2026

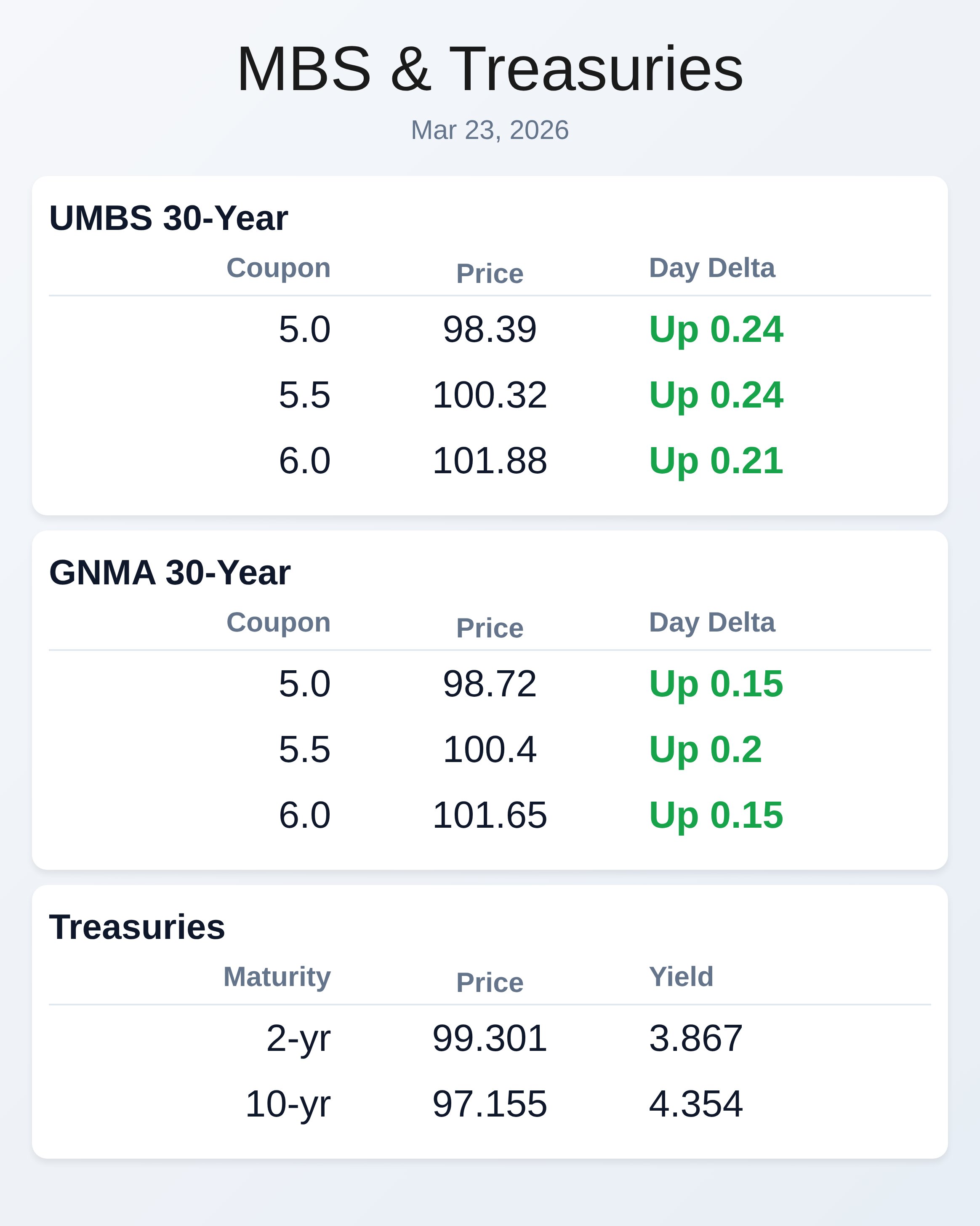

Bond markets whipsawed overnight after President Trump announced a five-day pause on strikes against Iranian energy infrastructure, citing progress in talks to reopen the Strait of Hormuz. The 10-year Treasury yield had surged to 4.443% by 6:45am before plummeting to 4.308% within minutes of the 7:04am announcement, ultimately settling around 4.354%. UMBS 5.0 coupons rallied 24 basis points to 98.39, while GNMA 5.0s gained 15 basis points to 98.72.

Oil prices collapsed on the news, though some confusion remains as certain sources report no direct talks occurred with Iran, only intermediary discussions. The dramatic reversal pulled mortgage pricing back from the brink after what had been a brutal overnight session. Repricing Risk and Rate Reality

Mortgage rates remain stubbornly elevated around 6.875%, with borrowers now fortunate to find anything near 6.375% after lenders repeatedly raised pricing throughout last week.

March has been essentially a one-way trade against bonds with only brief corrective moments, as geopolitical uncertainty and inflation fears dominate market sentiment. The morning’s rally offers some relief, but the volatility underscores how quickly conditions can shift based on Middle East developments. Lenders may issue improvement reprices today if current levels hold, though caution remains warranted given the whipsaw nature of recent trading.

Fed Rate Hike Odds Climbing

Bond traders now assign roughly 50% probability to a Federal Reserve rate hike by October, a dramatic shift from earlier expectations of continued cuts. President Trump’s decision to engage militarily in the Middle East has convinced markets that inflation pressures will intensify rather than subside, fundamentally altering the policy outlook. Surging inflation expectations have widened TIPS breakeven spreads, reflecting growing concern about persistent price pressures ahead.

Even with this morning’s geopolitical reprieve, the underlying trajectory suggests rates may stay elevated longer than many anticipated. Softer economic data showing cooling GDP growth and weakening consumer spending could eventually counterbalance these concerns if tensions genuinely de-escalate. Agency Buying Activity Provides Support

Both Freddie Mac and Fannie Mae are reportedly placing large orders to buy MBS, providing crucial support to mortgage-backed securities markets during this turbulent period.

This buying activity helps explain why MBS spreads haven’t blown out even wider despite the recent rate volatility. The GSEs’ presence in the market offers some stability for originators trying to price loans amid rapidly changing conditions. However, this institutional support can only do so much against broader macroeconomic headwinds and geopolitical shocks.

Originators should view this as a helpful backstop rather than a cure-all for current market challenges. Housing Market Fundamentals Weakening

Buyer demand has dropped to record lows as elevated rates continue to suppress affordability across most markets. Home prices are declining in the majority of metros, signaling a potential shift toward a more balanced housing market after years of seller dominance.

Persistent affordability challenges combined with structurally low housing inventory continue to cap upside potential in residential lending volumes. The industry remains constrained by these fundamental headwinds regardless of short-term rate movements. Any sustained improvement in mortgage rates would be needed to meaningfully revive purchase activity from current depressed levels.

Private Credit Stress Building

Stress in private credit markets continues to quietly build, with both investors and the Federal Reserve flagging risks tied to lending to weaker borrowers. These concerns previously helped push rates lower and could do so again if geopolitical tensions genuinely ease in coming weeks. The Fed’s increased scrutiny of non-bank lending suggests policymakers are monitoring financial stability risks beyond traditional banking channels.

Cracks in the economy including slower GDP growth and cooling labor markets may become a bigger focus for policymakers ahead. This week’s economic calendar remains relatively light with mostly second-tier data, allowing geopolitical developments and Fed speakers to drive market direction.

Locking vs Floating

The current environment strongly favors locking rather than floating.

Bond markets have traded in a predominantly negative direction throughout March with only brief corrective bounces. While this morning’s rally on Middle East news provides temporary relief, attempting to time additional improvements amounts to catching falling knives in a treacherous market. Wait for dust to definitively settle before taking major risks with floating strategies.

The only reason to float involves predicting future geopolitical outcomes, which carries substantial downside risk.

Today’s Events

Construction Spending for January at 10:00 AM (Forecast: 0.1%, Prior: 0.3%)

Bond Pricing

UMBS 30 yr

| Coupon | Price | Intra-Day Change |

| 5.0 | 98.39 | 0.24 |

| 5.5 | 100.32 | 0.24 |

| 6.0 | 101.88 | 0.21 |

GNMA 30 yr

| Coupon | Price | Intra-Day Change |

| 5.0 | 98.72 | 0.15 |

| 5.5 | 100.4 | 0.2 |

| 6.0 | 101.65 | 0.15 |

Treasuries

| Term | Yield | Price | Intra-Day Yield Change |

| 2 yr | 3.867 | 99.301 | -0.038 |

| 3 yr | 3.883 | 98.926 | -0.037 |

| 5 yr | 3.981 | 98.963 | -0.027 |

| 7 yr | 4.171 | 98.971 | -0.027 |

| 10 yr | 4.354 | 97.155 | -0.029 |

| 30 yr | 4.915 | 95.479 | -0.027 |