WTMS Blog Today = What’s up in Mortgage Today (AM) – 03/27/2026

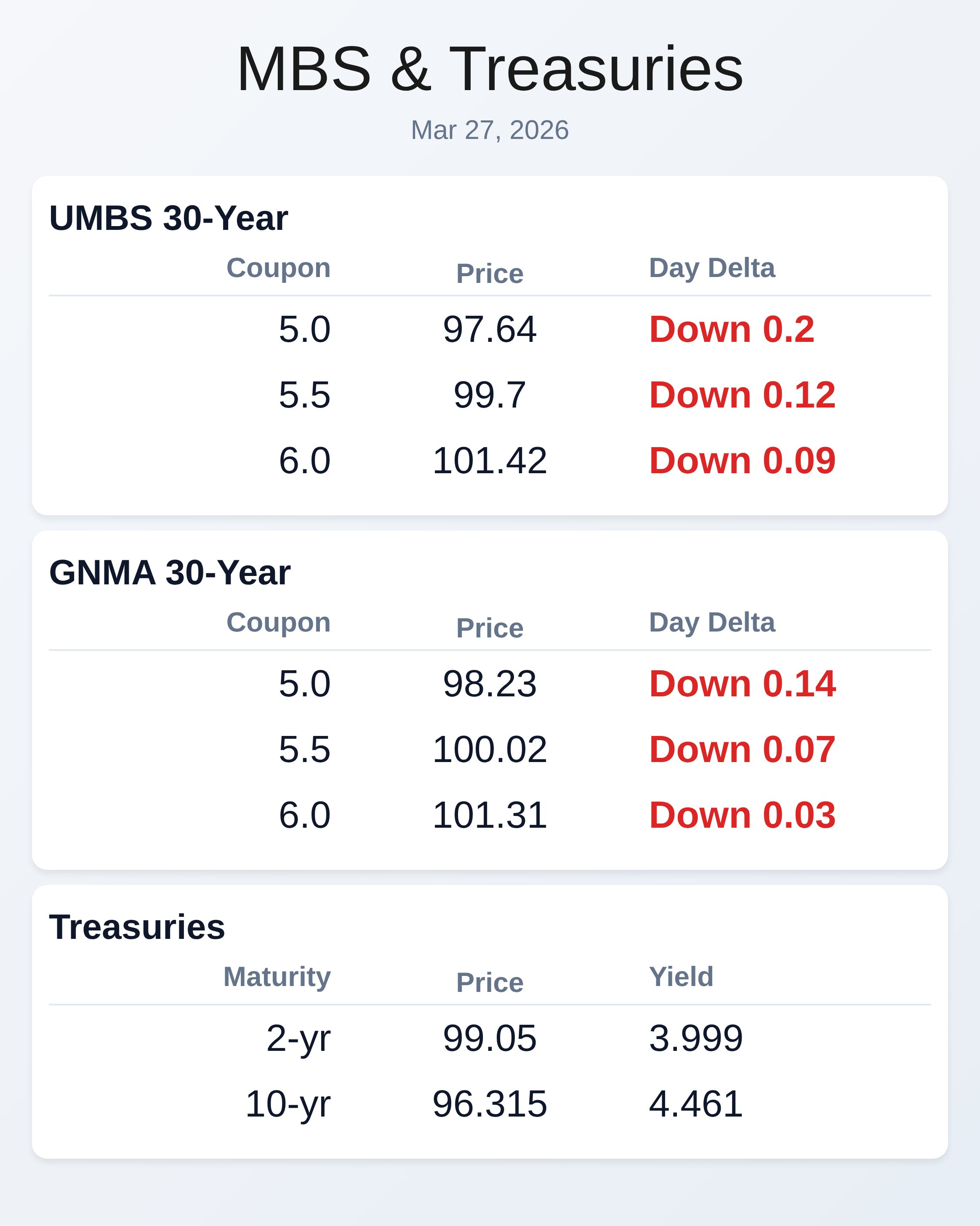

The bond market’s March volatility trap just claimed another victim as 10-year Treasury yields spiked 4.5 basis points to 4.455% this morning, confirming that the month-long weakness continues to punish floating strategies. MBS prices followed suit with UMBS 5.0 coupons dropping 20 basis points to 97.64, while GNMA 5.0s fell 14 basis points to 98.23. This morning’s move validates the persistent warning that March has been a “perpetual lock opportunity” due to elevated volatility and bond market weakness.

Thursday’s jobless claims data came in exactly at forecast with 210K initial claims, while continued claims dropped to 1,819K versus the 1,850K forecast. Despite the slightly better employment picture, bond markets ignored the positive news and continued their relentless march higher in yields. The disconnect between improving labor data and worsening bond performance highlights how technical factors and positioning are driving markets more than fundamentals.

UMBS securities across all coupons posted losses with the 5.0 coupon leading declines at negative 20 basis points, followed by 5.5s down 12 basis points and 6.0s off 9 basis points. GNMA bonds showed similar but slightly less severe weakness with 5.0s down 14 basis points, 5.5s off 7 basis points, and 6.0s declining just 3 basis points. The relative outperformance of higher coupons suggests some flight-to-quality within the mortgage-backed securities space.

Treasury yields rose across the entire curve with longer-term bonds bearing the brunt of selling pressure. The 30-year bond yield jumped 3.9 basis points to 4.976%, while the 7-year note saw the steepest increase at 5.9 basis points to 4.302%. The 2-year note held relatively steady with just a 0.7 basis point increase to 3.999%, creating a steepening bias that typically signals growth and inflation concerns.

Mortgage originators continue to face challenging conditions as the yield curve steepening and MBS underperformance compress profit margins. Rate sheets are expected to deteriorate further today following the morning’s weakness in both Treasuries and mortgage-backed securities. The persistent volatility makes intraday pricing adjustments likely, requiring constant attention to rate lock timing and inventory management.

Market technicals suggest the bond market weakness that has dominated March shows no signs of abating as we head into month-end. The 10-year yield ceiling/floor analysis mentioned in trading commentary indicates broader momentum remains negative for bonds. Originators who have maintained floating positions through March are learning expensive lessons about the importance of locking in volatile environments.

Locking vs Floating

Current market conditions strongly favor locking strategies as March volatility continues to punish floating positions with persistent bond market weakness. The combination of elevated volatility and negative momentum makes any short-term gains unreliable indicators of trend shifts. Rate spikes like today’s serve as reminders that floating strategies carry significant risk in the current environment.

Today’s Events

Continued Claims (March 14): 1,819K vs 1,850K forecast, 1,857K previous

Jobless Claims (March 21): 210K vs 210K forecast, 205K previous

Bond Pricing

UMBS 30 yr

| Coupon | Price | Intra-Day Change |

| 5.0 | 97.64 | -0.2 |

| 5.5 | 99.7 | -0.12 |

| 6.0 | 101.42 | -0.09 |

GNMA 30 yr

| Coupon | Price | Intra-Day Change |

| 5.0 | 98.23 | -0.14 |

| 5.5 | 100.02 | -0.07 |

| 6.0 | 101.31 | -0.03 |

Treasuries

| Term | Yield | Price | Intra-Day Yield Change |

| 2 yr | 3.999 | 99.05 | 0.007 |

| 3 yr | 4.018 | 98.549 | 0.021 |

| 5 yr | 4.131 | 98.294 | 0.032 |

| 7 yr | 4.302 | 98.19 | 0.059 |

| 10 yr | 4.461 | 96.315 | 0.041 |

| 30 yr | 4.976 | 94.562 | 0.039 |