WTMS Blog Today = What’s up in Mortgage Today (AM) – 03/30/2026

Mortgage-backed securities rallied Monday morning despite oil prices holding above $100 per barrel and ongoing Middle East tensions, with UMBS 5.0 coupons gaining 3/8ths and 10-year Treasury yields dropping 7 basis points to 4.36 percent. Three factors likely drove the gains: a correction in Fed Funds Futures that began Friday, pre-weekend defensive positioning unwinding without major escalation over the weekend, and month-end rebalancing flows creating technical demand. Consumer sentiment data released this morning showed the University of Michigan index falling to 53.3 in March from 56.6 previously, missing the 54.0 forecast and hitting the lowest level since December 2025.

One-year inflation expectations jumped to 3.8 percent from 3.4 percent, reflecting consumer anxiety over rising gas prices and falling stock portfolios, while five-year expectations held steady at 3.2 percent. Two Harbors Investment Corp terminated its merger agreement with UWM Holdings and will instead be acquired by CrossCountry Mortgage for $10.80 per share in all-cash, valuing the transaction at approximately $1.13 billion. CrossCountry will absorb the $25.4 million termination fee owed to UWM, adding Two Harbors’ capital markets platform and RoundPoint’s servicing infrastructure to potentially become the eighth-largest mortgage servicer by owned portfolio.

UWM issued a sharp rebuke calling the decision ego-driven and suggesting its stock-based offer carried superior value, hinting that legal challenges may follow with the full context to be “made public in due course.” The deal is expected to close in the second half of 2026, pending regulatory approvals and closing conditions. The USDA announced its Rural Housing Modernization Initiative, granting qualified lenders delegated authority to approve and close guaranteed rural housing loans without waiting for agency sign-off, aligning the program with HUD and VA processes. A final rule published March 19 will take effect June 17, 2026, with full implementation on September 28, 2028, while a pilot program called LITE (Lender Interactive Test Environment) launches September 1, 2026 for eligible lenders.

The agency also launched My RD Loan Portal, giving direct loan borrowers 24/7 self-service access to account information and payment capabilities. Eligibility standards, funding levels, and program safeguards remain unchanged—this is strictly a service delivery overhaul aimed at reducing delays and unnecessary back-and-forth. The USDA share of total mortgage applications remains below 1 percent nationally but carries significant weight in qualifying rural markets.

The housing market’s seller-buyer imbalance has widened to a record 630,000 homes, with 46 percent more sellers than buyers according to Redfin data stretching back to 2013. Affordability constraints are sidelining buyers as mortgage rates climbed to their highest levels since October, mortgage application volume dropped 10.5 percent last week, and canceled contracts hit a record 13.7 percent of homes under contract in February. Sun Belt cities that overbuilt during the pandemic boom face the worst imbalances, with Miami leading at sellers outnumbering buyers by 163 percent, followed by Nashville, Austin, West Palm Beach, and San Antonio.

The gap has grown 30 percent from a year ago, and buyers have technically held the numerical advantage since May 2024 reversed. This mismatch is creating downward price pressure in oversupplied markets while tighter inventory markets continue to see modest appreciation. CoStar Group amended its copyright infringement lawsuit against Zillow, now claiming the company has infringed on more than 53,000 watermarked photos across Zillow and syndicated platforms including Redfin and Realtor.com.

The original complaint filed in July 2025 identified nearly 47,000 CoStar-owned images, and CoStar alleges Zillow continued displaying approximately 8,000 of those specific images as of late September and has since infringed on thousands more. CoStar’s general counsel stated that Zillow re-published many of the same photographs after initially claiming to remove them, suggesting the company is deliberately using CoStar’s images to build listing pages, train algorithms like the Zestimate, and attract property owners to paid advertising services. Zillow called the amended complaint further proof of weaknesses in CoStar’s arguments and accused CoStar of leveraging litigation rather than competing on product quality.

The case represents what CoStar claims is one of the largest real estate image infringement disputes in history. The Federal Reserve continues its passive runoff of agency mortgage-backed securities holdings, now at $2.7 trillion after a 26 percent reduction since 2022, but at current pace it could take over a decade to return to an all-Treasury balance sheet. The portfolio remains heavily concentrated in low-coupon 30-year MBS, meaning any active sales—though unlikely—would disproportionately pressure those segments.

The feared risk of rapid prepayments flooding the market has diminished as rising Treasury yields pushed mortgage rates higher and sharply reduced refinancing activity, with the refinance share of mortgage activity falling to 49.6 percent last week from 52.3 percent previously. The adjustable-rate mortgage share is running around 8 percent of applications, while FHA accounts for roughly 20 percent, VA about 16 percent, and USDA less than 1 percent. Product mix remains stable despite the volatility in underlying rate markets, with originators maintaining defensive postures until bond market momentum shows a definitive shift requiring more than one or two days of improvement.

Locking vs Floating

MBS Live advises maintaining a defensive floating strategy despite Monday morning’s gains, noting the recovery does not signal a definitive top in rates. While intraday improvements provided some relief after last week’s climb to 2026 highs, the broader trend remains unfavorable until momentum shifts convincingly. Market participants should watch 10-year yield ceiling and floor levels to track bigger-picture bond market momentum rather than reacting to single-day movements.

Mixed blessings continue as rates pulled back from morning highs but remain elevated, requiring caution until a sustained reversal materializes over multiple sessions.

Today’s Events

Consumer Sentiment (Mar): 53.3 vs 54.0 forecast, 56.6 prior

Sentiment: 1-year Inflation (Mar): 3.8% vs 3.4% forecast, 3.4% prior

Sentiment: 5-year Inflation (Mar): 3.2% vs 3.2% forecast, 3.3% prior

Fed Chair Powell Speech: 10:30 AM ET

Bond Pricing

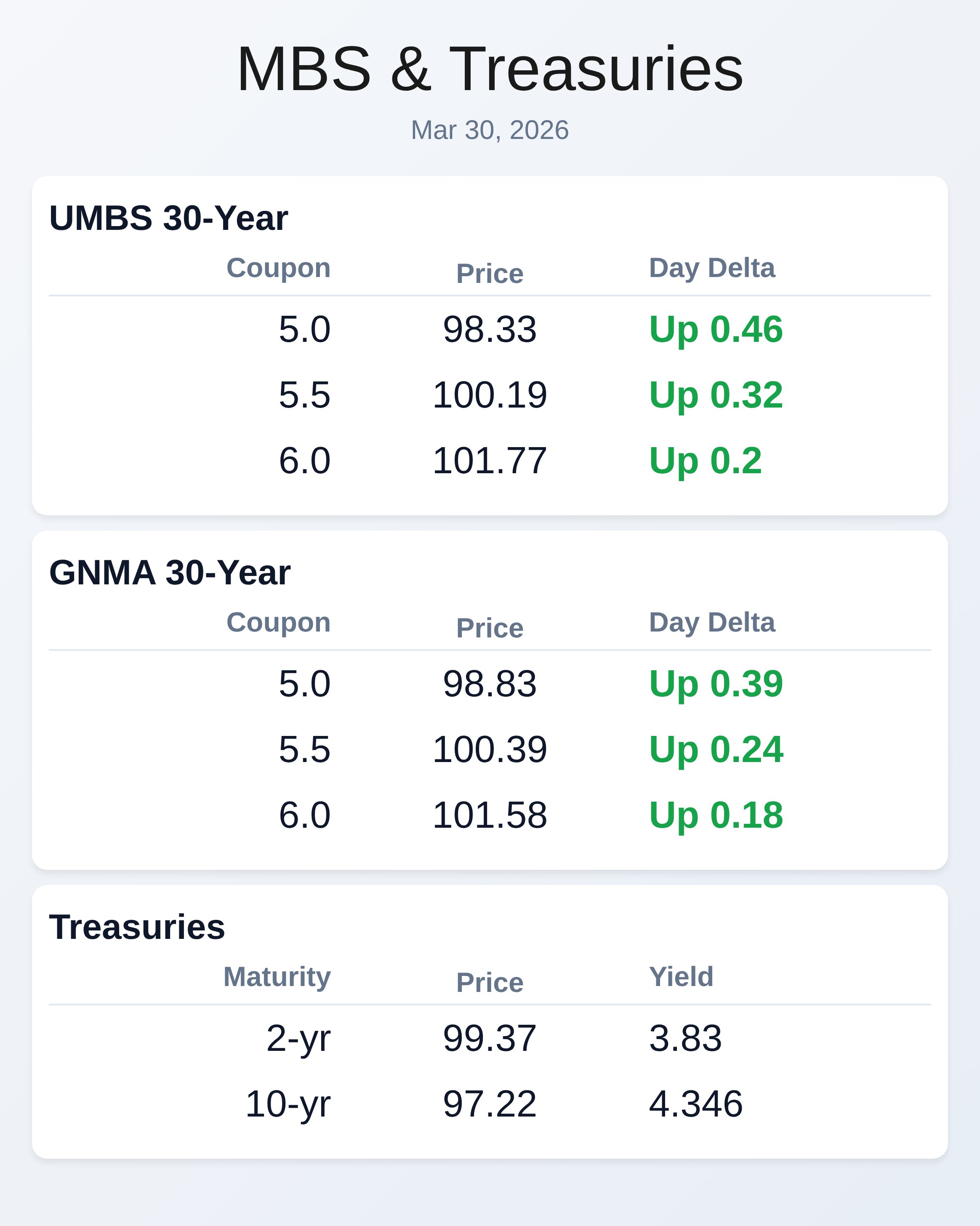

UMBS 30 yr

| Coupon | Price | Intra-Day Change |

| 5.0 | 98.33 | 0.46 |

| 5.5 | 100.19 | 0.32 |

| 6.0 | 101.77 | 0.20 |

GNMA 30 yr

| Coupon | Price | Intra-Day Change |

| 5.0 | 98.83 | 0.39 |

| 5.5 | 100.39 | 0.24 |

| 6.0 | 101.58 | 0.18 |

Treasuries

| Term | Yield | Price | Intra-Day Yield Change |

| 2 yr | 3.830 | 99.370 | -0.084 |

| 3 yr | 3.852 | 99.011 | -0.089 |

| 5 yr | 3.978 | 98.977 | -0.091 |

| 7 yr | 4.163 | 99.019 | -0.092 |

| 10 yr | 4.346 | 97.220 | -0.083 |

| 30 yr | 4.911 | 95.541 | -0.060 |