WTMS Blog Today = What’s up in Mortgage Today (AM) – 03/31/2026

Bonds are rallying despite surging oil prices as markets shift focus from inflation fears to growth concerns amid the ongoing Middle East conflict. Treasury yields dropped across the curve Monday with the 10-year falling to 4.33% from last week’s eight-month high of 4.48%, while UMBS prices gained ground with most coupons showing solid improvements. The tug-of-war between stagflation risks has markets oscillating between worrying about higher prices from oil disruptions versus slower economic growth from geopolitical instability.

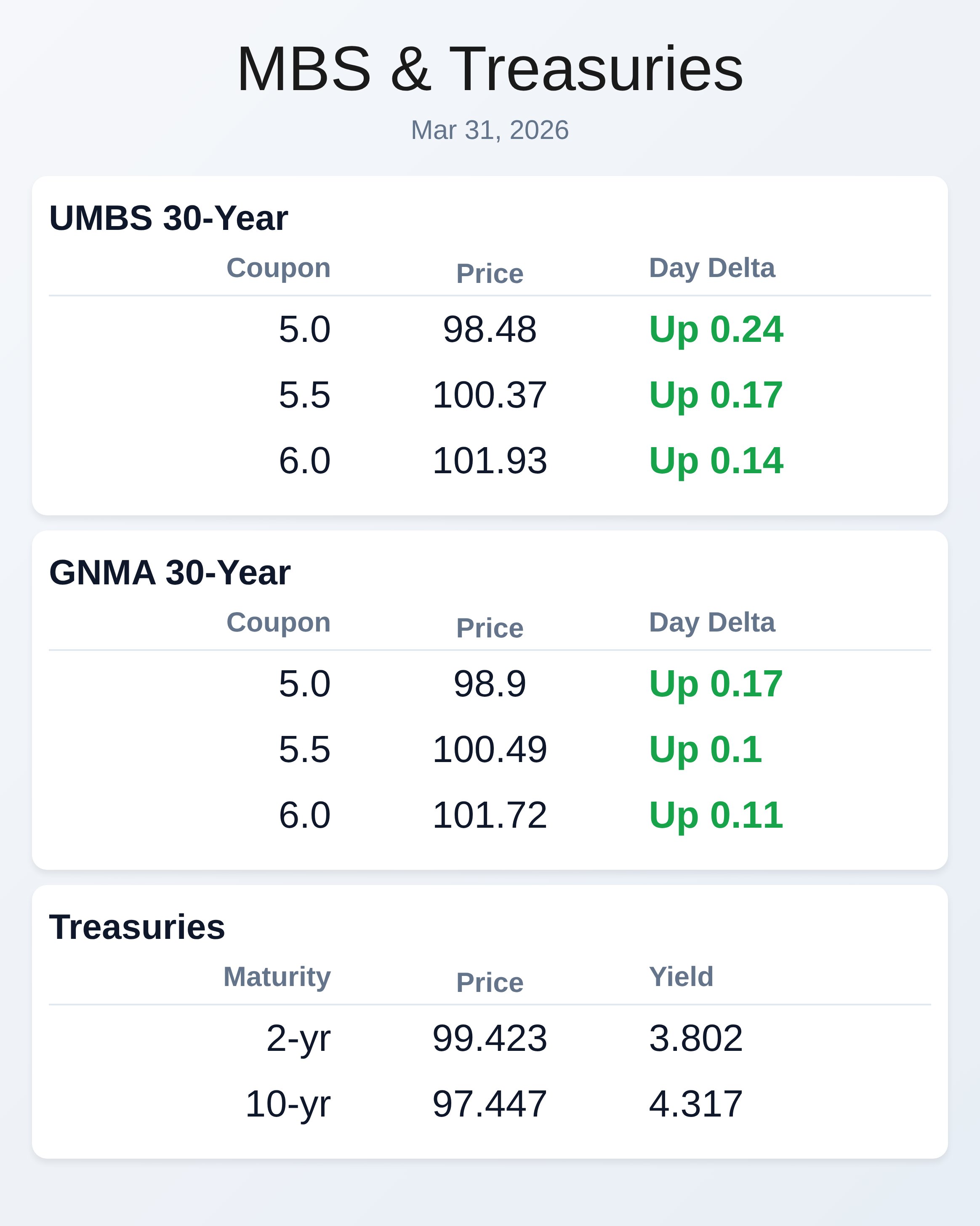

Traders are now betting the Fed will hold rates steady in the 3.5% to 3.75% range this year with only a small chance of cuts by mid-2027. This marks a notable shift from earlier positioning when Iran’s near-total blockade of the Strait of Hormuz first sent crude soaring nearly 50%. UMBS securities showed resilient performance with the 5.0 coupon gaining 24 basis points to 98.48, while the liquid 5.5s advanced 17 basis points to 100.37.

GNMA bonds also participated in the rally with similar coupon performance, though gains were slightly more modest than their UMBS counterparts. The mortgage-backed securities market appears to be benefiting from the broader Treasury rally as duration risk concerns ease with falling yields. Current dollar prices suggest origination margins remain under pressure but are stabilizing from recent lows.

The spread relationships between coupons continue to normalize as rate volatility moderates. European inflation data added another layer to the global monetary policy puzzle with eurozone CPI rising to 2.5% in March, faster than February’s pace but below analyst expectations. This acceleration, driven primarily by energy costs from the Iran conflict, reinforces expectations for ECB rate hikes with markets pricing three quarter-point increases this year.

The inflation surge represents the steepest jump since 2022 and highlights how geopolitical tensions are reshaping central bank calculus worldwide. German 10-year yields fell despite the hotter inflation print, mirroring U.S. Treasury performance as growth fears override price pressures.

UK bonds followed suit with 10-year gilts dropping to 4.92% as the Bank of England faces similar stagflation trade-offs. President Trump’s signals about potentially ending the U.S. military campaign against Iran provided some relief to energy markets, though the Strait of Hormuz remains largely closed.

Wall Street Journal reports suggest Trump told aides the U.S. should achieve its main goals of weakening Iran’s naval capabilities while pursuing diplomatic pressure to restore trade flows. Iranian drone strikes on Kuwaiti oil tankers off Dubai underscore continuing dangers despite talks of de-escalation.

Brent crude wavered around $108 per barrel as traders weighed ceasefire prospects against ongoing supply disruptions. Trump’s April 6 deadline for reopening the strait continues to loom over market sentiment. The mortgage origination landscape faces headwinds from elevated borrowing costs even as bonds show signs of stabilization.

With the 10-year Treasury still 40+ basis points higher since the conflict began, purchase applications remain under pressure while refinance activity stays dormant. Loan officers report continued margin compression as competition intensifies for scarce volume, particularly in the jumbo market where rates have pushed many borrowers to the sidelines. The MBA Secondary & Capital Markets Conference in May will provide crucial insights into how lenders are adapting to this challenging environment.

Industry participants are watching closely for any Fed pivot that might provide relief to mortgage demand. Today’s Treasury performance suggests investors are beginning to price in economic slowdown risks over pure inflation concerns, but one day’s move doesn’t establish a trend. The bond market remains caught between competing forces of energy-driven price pressures and growth-dampening geopolitical uncertainty.

Fed officials including Vice Chair Bowman and Governor Barr speak later today and may provide guidance on how policymakers view these crosscurrents. Economic data including the Chicago PMI and consumer confidence could offer early glimpses into March sentiment before Friday’s crucial payroll report. For mortgage professionals, the key remains whether this nascent bond rally can sustain itself long enough to meaningfully improve funding costs and borrower demand.

Locking vs Floating

Despite yesterday’s fairly significant bond rally, we remain just one day removed from the weakest closing levels in months, making it premature to conclude that rising rate pressure has run its course. MBS prices provide helpful guidance for intraday risk management, but monitoring 10-year Treasury yield ceilings and floors offers better insight into broader bond market momentum shifts. Until we see more than a day or two of sustained recovery, the prudent approach remains cautious given how quickly sentiment can reverse in this volatile environment.

Bond Pricing

UMBS 30 yr

| Coupon | Price | Intra-Day Change |

GNMA 30 yr

| Coupon | Price | Intra-Day Change |

Treasuries

| Term | Yield | Price | Intra-Day Yield Change |

UMBS 30 yr

| Coupon | Price | Intra-Day Change |

| 5.0 | 98.48 | 0.24 |

| 5.5 | 100.37 | 0.17 |

| 6.0 | 101.93 | 0.14 |

GNMA 30 yr

| Coupon | Price | Intra-Day Change |

| 5.0 | 98.9 | 0.17 |

| 5.5 | 100.49 | 0.1 |

| 6.0 | 101.72 | 0.11 |

Treasuries

| Term | Yield | Price | Intra-Day Yield Change |

| 2 yr | 3.802 | 99.423 | -0.028 |

| 3 yr | 3.821 | 99.1 | -0.034 |

| 5 yr | 3.947 | 99.115 | -0.039 |

| 7 yr | 4.132 | 99.205 | -0.035 |

| 10 yr | 4.317 | 97.447 | -0.035 |

| 30 yr | 4.892 | 95.827 | -0.023 |

Subscribe free at WellThatMakesSense.com for daily market insights that help you navigate the mortgage landscape.