WTMS Blog Today = What’s up in Mortgage Today (AM) – 04/07/2026

Bond markets find themselves in a holiday-adjacent holding pattern as traders exercise caution ahead of potential geopolitical developments. March’s significant rate spike appears to have cooled in early April, though volatility risks persist with ongoing tensions in Iran casting uncertainty over defensive momentum. The 10-year Treasury yield moved slightly higher to 4.343%, up 0.008 basis points from the previous close, signaling continued market hesitancy.

Mortgage-backed securities showed mixed performance with UMBS 30-year coupons displaying minimal movement across the board. This sideways action reflects the market’s wait-and-see approach as participants assess whether recent stabilization can maintain momentum. ISM services data delivered a mixed bag that reinforced the current cautious tone in fixed-income markets.

The ISM Non-Manufacturing PMI came in at 54.0, missing the 55.0 forecast and declining from the previous 56.1 reading, suggesting some cooling in the services sector. However, the Services New Orders component jumped to 60.6 from 58.6, indicating underlying demand remains robust. Most concerning for bond traders was the Services Prices index, which surged to 70.7 from 63.0, well above expectations and signaling persistent inflationary pressures.

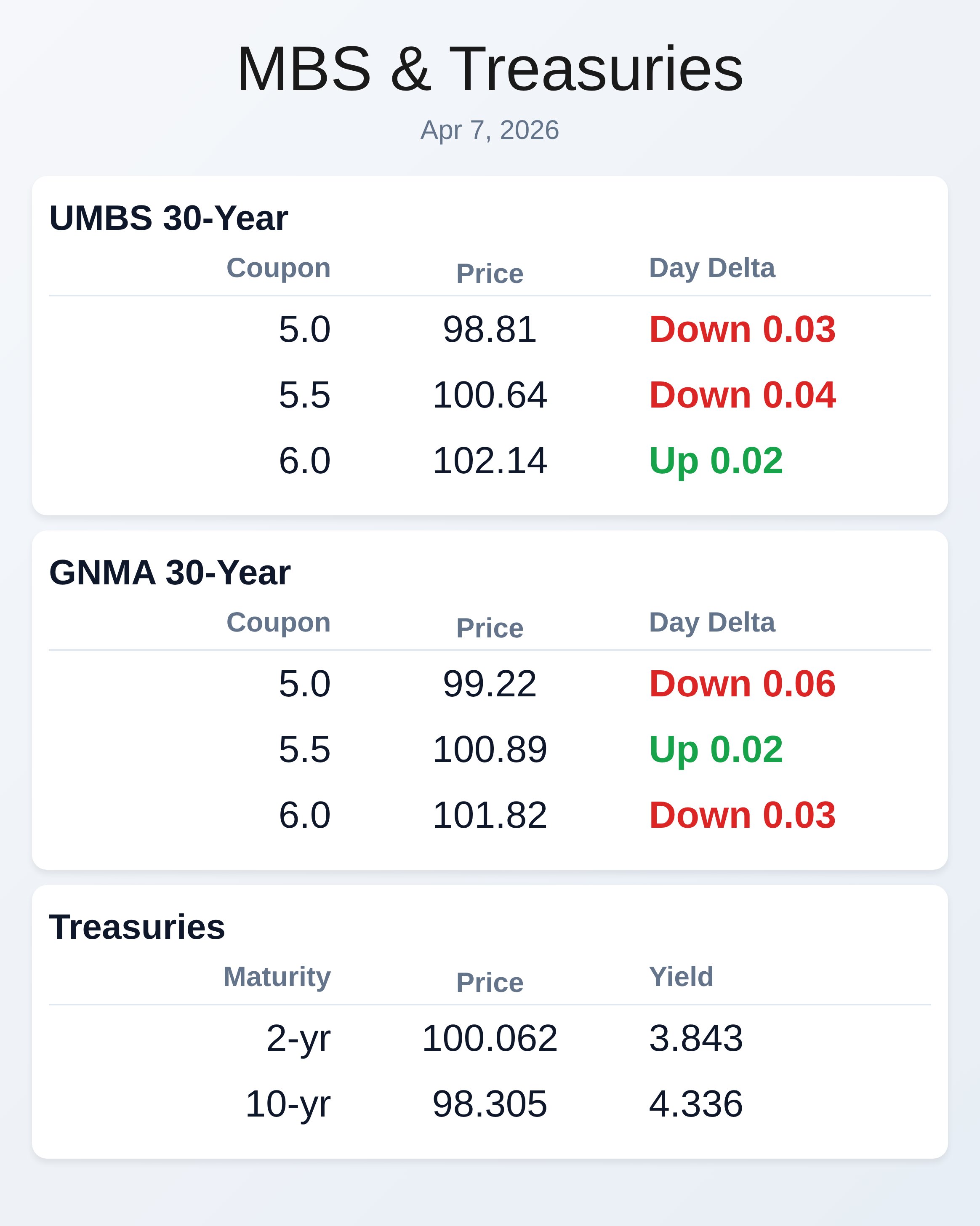

Employment within services contracted sharply to 45.2 from 51.8, adding another layer of complexity to the economic narrative. UMBS pricing remained relatively stable with the 5.0 coupon trading at 98.81, down just 0.03, while the 5.5 coupon held at 100.64 with a modest 0.04 decline. The 6.0 coupon showed slight strength, gaining 0.02 to reach 102.14, suggesting some selective buying interest in higher coupons.

This stability in mortgage securities reflects the current range-bound environment as originators navigate uncertain rate directions. The narrow price movements indicate that while there’s no significant selling pressure, buyers remain cautious about committing to larger positions. GNMA securities mirrored the mixed UMBS performance with similarly modest intraday changes across coupons.

The 5.0 GNMA coupon declined 0.06 to 99.22, showing slightly more weakness than its UMBS counterpart, while the 5.5 coupon gained 0.02 to reach 100.89. The 6.0 GNMA coupon pulled back 0.03 to 101.82, maintaining its typical discount to UMBS pricing. These government-backed securities continue to trade with their characteristic tight spreads to Treasuries, providing originators with reliable execution venues.

The stability in GNMA pricing supports continued securitization activity for conforming loan production. Treasury yields across the curve showed the market’s indecision with shorter maturities declining while longer dates edged higher. The 2-year note yield dropped 1.3 basis points to 3.843%, while the 5-year fell 0.7 basis points to 3.98%, suggesting some flight-to-quality buying in the front end.

Conversely, the 30-year bond yield climbed 1.3 basis points to 4.903%, reflecting concerns about long-term inflation expectations following the hot ISM prices data. This yield curve steepening indicates that while near-term Fed policy expectations remain anchored, longer-term inflation concerns persist. Mortgage originators face a challenging environment where rate lock decisions require careful timing given the elevated volatility risks stemming from geopolitical tensions.

The recent cooling of March’s rate spike provides some relief, but the potential for renewed defensive momentum shifts keeps the outlook uncertain. With ISM services prices surging well above forecasts, any signs of broader inflationary pressure could quickly reverse recent bond market gains. Current pricing levels suggest that while there’s no immediate pressure to rush lock decisions, the window for favorable conditions remains narrow and dependent on external factors beyond traditional economic data.

Locking vs Floating

Current market conditions favor a cautious approach to rate lock timing as volatility risks remain elevated due to ongoing geopolitical tensions in Iran. While March’s significant rate spike has cooled in early April, the potential for defensive momentum shifts keeps the outlook uncertain for bond markets. The 10-year Treasury yield ceiling and floor levels continue to help track broader bond market momentum, though current sideways action suggests waiting for clearer directional signals.

MBS pricing provides helpful intraday risk management, but originators should focus on the bigger picture Treasury movements for longer-term positioning decisions.

Today’s Events

ISM Non-Manufacturing PMI (March): 54.0 vs 55.0 forecast, 56.1 previous

ISM Services Employment (March): 45.2 vs no forecast, 51.8 previous

ISM Services New Orders (March): 60.6 vs no forecast, 58.6 previous

ISM Services Prices (March): 70.7 vs no forecast, 63.0 previous

Bond Pricing

UMBS 30 yr

| Coupon | Price | Intra-Day Change |

| 5.0 | 98.81 | -0.03 |

| 5.5 | 100.64 | -0.04 |

| 6.0 | 102.14 | 0.02 |

GNMA 30 yr

| Coupon | Price | Intra-Day Change |

| 5.0 | 99.22 | -0.06 |

| 5.5 | 100.89 | 0.02 |

| 6.0 | 101.82 | -0.03 |

Treasuries

| Term | Yield | Price | Intra-Day Yield Change |

| 2 yr | 3.843 | 100.062 | -0.013 |

| 3 yr | 3.869 | 98.963 | -0.011 |

| 5 yr | 3.98 | 99.53 | -0.007 |

| 7 yr | 4.158 | 100.553 | -0.009 |

| 10 yr | 4.336 | 98.305 | 0.001 |

| 30 yr | 4.903 | 97.603 | 0.013 |