WTMS Blog Today = What’s up in Mortgage Today (AM) – 04/08/2026

Treasury yields are dropping hard this morning as markets brace for Iran’s response deadline tonight, with the 10-year yield falling to 4.236%, down 6.4 basis points from yesterday’s close. The geopolitical uncertainty has sparked a flight to safety, pushing bond prices higher and creating favorable conditions for mortgage rates. UMBS securities are following suit with solid gains across all coupons, while GNMA bonds are posting similar strength.

The market’s calm demeanor in early April has given way to heightened volatility as traders position for either escalation or de-escalation from the Middle East tensions. This morning’s pre-market action suggests Wednesday could deliver dramatically different trading conditions than we’ve seen recently. Economic data released this morning painted a mixed picture for the mortgage market, with February’s Core Capital Expenditures jumping 0.6% versus the 0.4% forecast, signaling stronger business investment than expected.

However, Durable Goods orders disappointed with a -1.4% decline against expectations for only a -0.5% drop, suggesting some softness in manufacturing demand. The ADP Employment Change Weekly came in at 26,000 new jobs, up from the prior week’s 10,000 reading, though no forecast was available for comparison. These data points are creating cross-currents in the bond market, with the stronger CapEx data potentially weighing against the geopolitical rally.

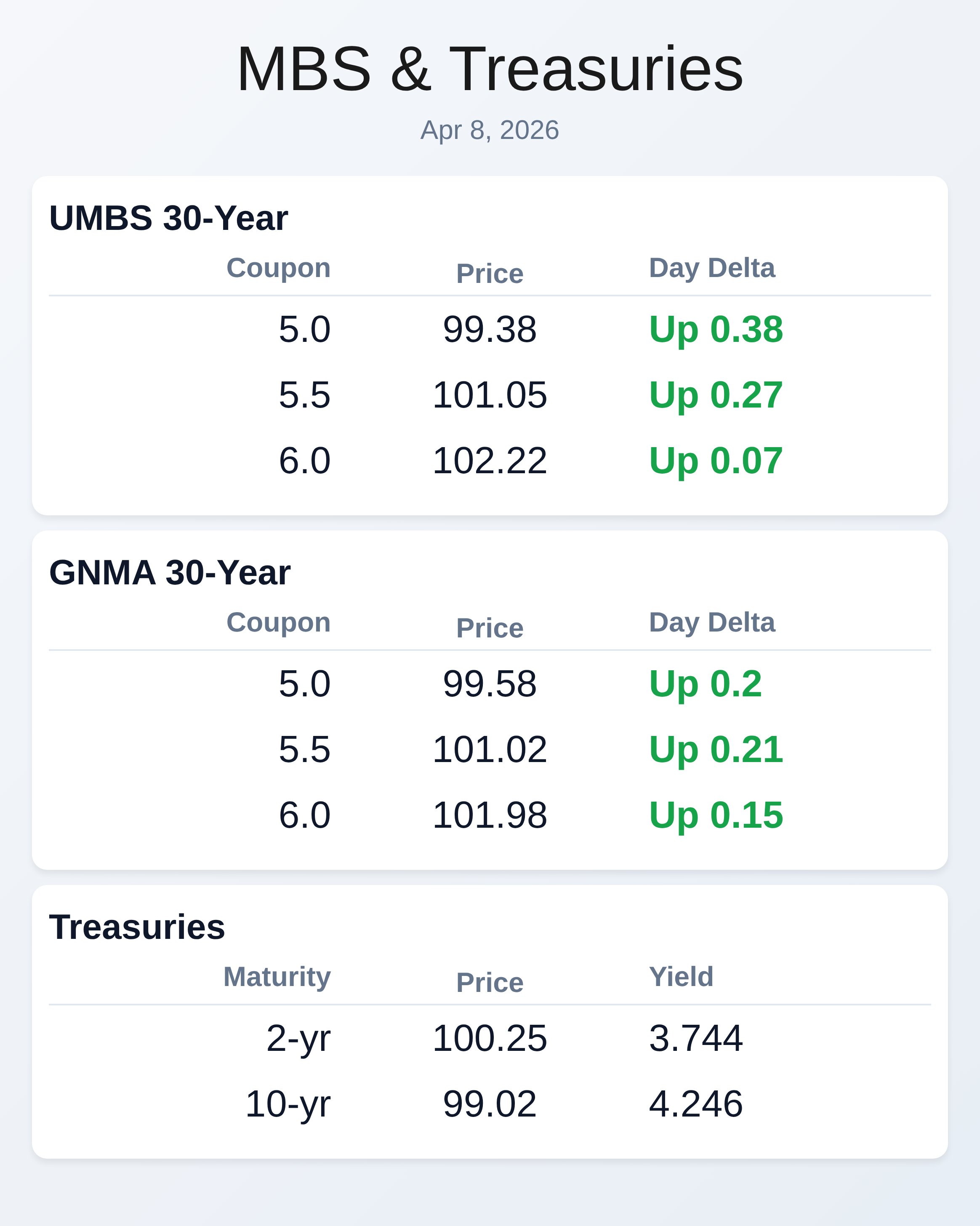

The net effect appears to favor lower yields as investors prioritize safety over economic strength signals. Mortgage bond pricing is showing significant strength across the board, with UMBS 5.0% coupons up 38 basis points to 99.38, while 5.5% coupons gained 27 basis points to 101.05. The 6.0% coupon UMBS securities posted more modest gains of 7 basis points, reaching 102.22.

GNMA securities are tracking closely with UMBS, showing 20 basis points of improvement in 5.0% coupons and 21 basis points in 5.5% coupons. This broad-based rally in mortgage securities is creating opportunities for originators to offer more competitive rates to borrowers. The strength in both UMBS and GNMA markets suggests institutional investors are actively seeking yield in the mortgage-backed securities space.

Fed balance sheet dynamics are taking center stage as current Fed nominee Warsh signals intentions to reduce the central bank’s $6.7 trillion portfolio of Treasuries and MBS. The challenge lies in understanding the liabilities these assets offset, including $3 trillion in commercial bank deposits, $2.4 trillion in currency, and $1 trillion in the Treasury’s checking account. Only bank deposits can realistically be reduced, which means carefully managing bank liquidity without disrupting financial markets.

This potential policy shift could have significant implications for MBS demand and pricing in the months ahead. Mortgage originators should monitor how these discussions evolve, as any actual balance sheet reduction could affect funding costs and secondary market conditions. Treasury yield movements are providing crucial directional signals for mortgage pricing, with the entire yield curve showing strength from the 2-year note down to 3.744% to the 30-year bond at 4.848%.

The 10-year Treasury’s 5 basis point decline to 4.246% is particularly important for mortgage rate direction, as it often serves as a benchmark for longer-term lending rates. The yield curve flattening we’re seeing today suggests investors are pricing in potential economic slowdown risks or extended geopolitical uncertainty. This environment typically favors mortgage origination volumes as borrowing costs become more attractive.

The key question is whether this rally can sustain itself beyond the immediate geopolitical concerns. Market volatility is expected to intensify as we approach tonight’s deadline for Iran’s response, with options on the table for either a two-week extension or a ceasefire that could dramatically alter tomorrow’s trading landscape. Bond traders are already positioning for significant moves in either direction, creating opportunities for both gains and losses in mortgage securities.

The relatively calm trading we’ve experienced in early April appears to be ending, with Wednesday likely to bring much more active price discovery. Originators should prepare for potential rate volatility and consider their risk management strategies accordingly. The current rally in bonds provides a window of opportunity that may not persist if geopolitical tensions ease.

Locking vs Floating

The current environment favors a cautious approach to floating, given the heightened geopolitical uncertainty surrounding Iran’s response deadline. While bonds are rallying today on safe-haven demand, the potential for dramatic reversals on Wednesday creates significant risk for borrowers waiting for further rate improvements. The mixed economic data provides some fundamental support for lower rates, but geopolitical events can override economic fundamentals quickly.

Originators should consider the timing of their pipeline and the risk tolerance of their borrowers when making lock-versus-float recommendations.

Today’s Events

ADP Employment Change Weekly: 26K vs no forecast, 10K previous

Core CapEx (February): 0.6% vs 0.4% forecast, 0% previous

Durable Goods (February): -1.4% vs -0.5% forecast, 0% previous

Bond Pricing

UMBS 30 yr

| Coupon | Price | Intra-Day Change |

| 5.0 | 99.38 | 0.38 |

| 5.5 | 101.05 | 0.27 |

| 6.0 | 102.22 | 0.07 |

GNMA 30 yr

| Coupon | Price | Intra-Day Change |

| 5.0 | 99.58 | 0.2 |

| 5.5 | 101.02 | 0.21 |

| 6.0 | 101.98 | 0.15 |

Treasuries

| Term | Yield | Price | Intra-Day Yield Change |

| 2 yr | 3.744 | 100.25 | -0.045 |

| 3 yr | 3.763 | 99.26 | -0.086 |

| 5 yr | 3.875 | 100.001 | -0.055 |

| 7 yr | 4.055 | 101.176 | -0.053 |

| 10 yr | 4.246 | 99.02 | -0.05 |

| 30 yr | 4.848 | 98.456 | -0.024 |