**WTMS Blog Today = What’s up in Mortgage Today (AM) – 06/02/2026**

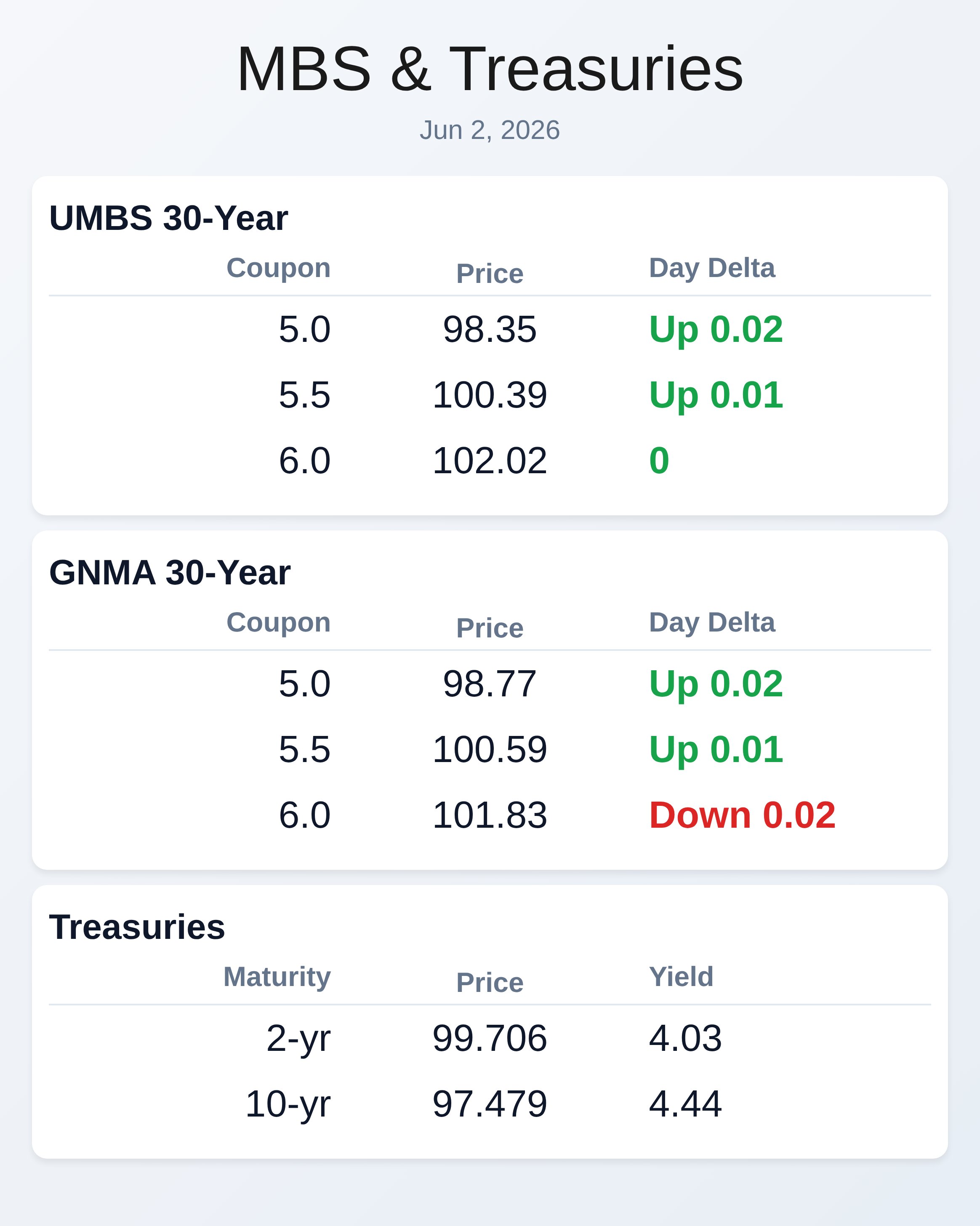

Bond markets found relief as the 10-year Treasury yield dropped to 4.43 percent after closing yesterday at 4.48 percent, even as oil prices stabilized amid cautious optimism about U.S.-Iran peace talks. Traders are treating geopolitical risk as temporary volatility rather than a lasting macro shock, which means rates could reverse sharply if negotiations collapse. Agency MBS prices opened better by 0.125 to 0.250 basis points, with UMBS 5.5 coupons stable at 100.39 and GNMA 5.5 coupons at 100.59.

The curve remains caught between fears of inflation persistence and hopes for eventual growth deterioration. Overall, positioning suggests calm but fragile market sentiment heading into today’s economic data. Economic strength continues to complicate the Federal Reserve’s inflation narrative, despite manufacturing employment showing contraction signals.

May’s ISM Manufacturing Index came in at 54.0 percent, beating forecasts of 53.0 and up from 52.7 in April, signaling manufacturing acceleration despite persistent pricing pressures. Construction spending grew 0.4 percent in April versus a 0.2 percent forecast, while prices-paid indices remain elevated—the ISM measure fell only slightly to 82.1 from 84.6, still well above historical norms. The Fed is increasingly abandoning easing bias after months of dovish forecasts, and Chair Warsh’s first FOMC meeting (June 16-17) is more likely to signal continuity than regime change.

Mortgage originators should prepare for a higher-for-longer rate environment as Fed officials shift focus toward inflation persistence over growth concerns. The front end of the Treasury curve now reflects expectations that policy will remain unchanged well into 2027, while the long end remains volatile due to oil prices and term premium swings. Markets are no longer debating imminent cuts versus hikes; they are instead wrestling with whether inflation or growth deterioration will break the Fed’s equilibrium.

Some Fed officials may begin penciling in higher rates, but there is insufficient evidence yet that inflation persistence clearly outweighs downside risks to growth. Any discussion of balance sheet reduction will face institutional resistance to departing from the ample-reserves framework. This uncertainty creates a challenging environment for lenders trying to price and hedge rate risk over multi-month periods.

Equity markets paused their AI-fueled rally as investors weighed Middle East peace prospects, with futures slipping 0.1 percent after an eight-day winning streak. Technology shares gave some support, including a 19 percent premarket surge in Marvell Technology after Nvidia CEO Jensen Huang signaled it could be the “next trillion-dollar company.” Traders are juggling unprecedented euphoria around AI infrastructure spending against a war that has disrupted oil markets historically. Bitcoin dropped below $70,000 for the first time in two months, suggesting some risk-off sentiment in traditional financial assets.

The uncertainty about crude prices means mortgage professionals should monitor energy-linked inflation metrics closely, as volatile oil could reignite rate pressures. Origination-focused vendors and companies continue aggressive product launches and consolidation activity across the mortgage ecosystem. Inside Real Estate (formerly BoomTown) has quietly rolled out a lead-generation product for lenders called BoldTrail, offering exclusive high-intent consumer opportunities in select markets with several metros already nearing capacity.

Today’s economic calendar includes non-market-moving Redbook same-store sales data, April JOLTS job openings at 10:00 AM ET, and a speech from Cleveland Fed President Hammack at 8:30 AM ET. The job openings report will likely show continued strength based on high-frequency data, adding to favorable labor-market releases for April and potentially reinforcing the Fed’s hawkish stance. Treasury supply includes a 6-week bill auction at 11:30 AM ET.

Market participants should monitor these releases for any signals about Fed policy persistence, particularly as Chair Warsh prepares for his first FOMC meeting later this month. Mortgage lenders should remain cautious on rate positioning given the conflicting signals between economic strength and geopolitical uncertainty.

**Locking vs Floating**

As warned last Friday, Iran negotiations remain fluid and overnight lock-float decisions remain coin flips.

The market has priced in a diplomatic outcome that has not yet materialized, creating the risk of significant reversal if talks break down. If energy infrastructure becomes a more direct target or negotiations stall, the 10-year yield could push back above 4.50 percent as investors reprice inflation risk rather than celebrate growth optimism. MBS prices help with intraday risk management, but tracking 10-year Treasury yield ceilings and floors provides the broader bond market momentum picture that matters most for rate decisions.

**Today’s Events**

Construction Spending (April): 0.4% vs 0.2% forecast, 0.6% previous

ISM Manufacturing Employment (May): 48.6 vs forecast not available, 46.4 previous

ISM Manufacturing PMI (May): 54.0 vs 53 forecast, 52.7 previous

ISM Manufacturing Prices Paid (May): 82.1 vs 85.5 forecast, 84.6 previous

**Bond Pricing**

**UMBS 30 yr**

| Coupon | Price | Intra-Day Change |

**GNMA 30 yr**

| Coupon | Price | Intra-Day Change |

**Treasuries**

| Term | Yield | Price | Intra-Day Yield Change |

| 2yr | 4.03 | 99.706 | -0.003 |

| 3yr | 4.075 | 98.393 | -0.008 |

| 5yr | 4.156 | 98.743 | -0.008 |

| 7yr | 4.29 | 99.758 | -0.012 |

| 10yr | 4.44 | 97.479 | -0.017 |

| 30yr | 4.953 | 96.846 | -0.018 |