**WTMS Blog Today = What’s up in Mortgage Today (AM) – 06/04/2026**

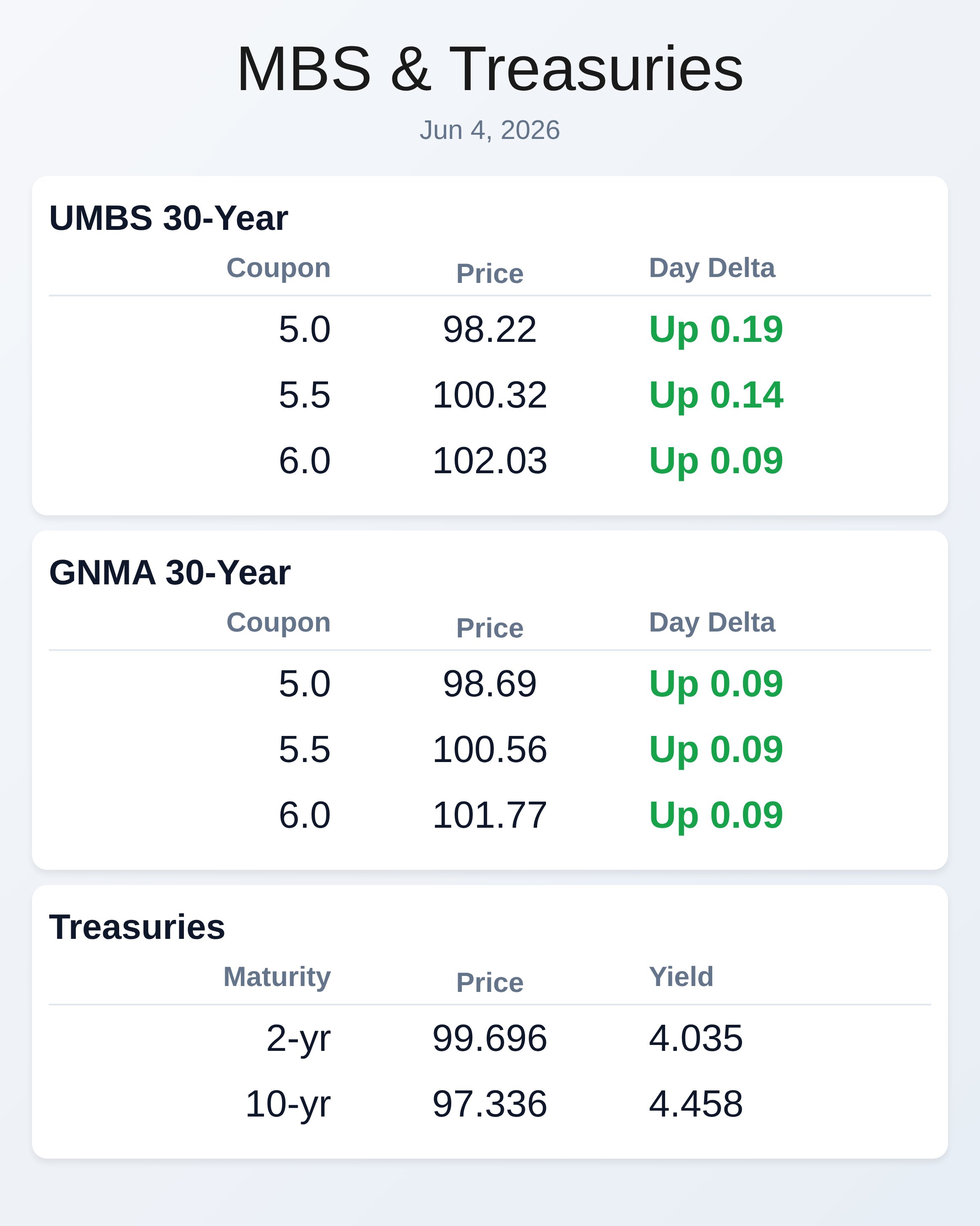

Peace negotiations headlines erased Wednesday’s losses and sent mortgage-backed securities higher by mid-morning. The Trump administration’s announcement of final talks to end the Iran war triggered a 4 basis point rally in the 10-year Treasury, which fell to 4.455% by 8:42 AM. MBS prices climbed 7 ticks across coupons, with UMBS 5.0 rising to 98.22 and UMBS 5.5 reaching 100.37.

Jobless claims data at 8:30 AM showed 225K initial claims versus a 213K forecast, having minimal market impact. Oil prices retreated 3.2% below $95 per barrel, supporting bond strength despite ongoing geopolitical tension. The mortgage market faces a growing convexity hedging challenge that threatens volatility ahead.

Bloomberg’s analysis reveals that mortgage investors are increasingly protecting against price declines by selling Treasury futures when MBS prices fall—a strategy that amplifies market moves in both directions. With over $2 trillion in mortgage securities now carrying 5%+ coupons, roughly four times the level from three years ago, bondholders must actively hedge interest-rate risk. About one-third of outstanding MBS now trade near par value where convexity sensitivity is greatest, forcing frequent rebalancing.

This “Beast” that vanished after the Fed’s 2022 rate hikes has awakened, with Goldman Sachs estimating the recent selloff roughly equivalent to $40 billion in 10-year Treasury selling. GNMA and UMBS securities showed mixed performance as investors digested competing signals. GNMA 5.0 gained 0.09 points to 98.69 while UMBS 5.0 climbed 0.19 to 98.22, reflecting modest upward momentum.

The narrower GNMA moves versus UMBS suggest government-guaranteed pools saw slightly less buying pressure. UMBS 6.0 advanced 0.09 to 102.03, though the curve steepness indicates traders remain cautious on longer coupons. These modest gains reflect the temporary relief from geopolitical headlines rather than fundamental shift in lending demand.

Treasury yields retreated across the curve as investors repriced Fed rate-cut expectations. The 2-year yield fell 4.7 basis points to 4.035%, while the 10-year dropped 3.8 basis points to 4.458%. The 30-year yield declined 2.5 basis points to 4.966%, showing steeper cuts in shorter maturities.

This inversion pattern suggests bond markets are pricing in economic caution or potential Fed easing later in 2026. Tomorrow’s jobs report will be the critical test of whether today’s calm persists or whether sticky labor data reignites inflation concerns. Mortgage originators should monitor the convexity hedging dynamic closely as it directly impacts secondary market execution.

When mortgage prices fall sharply, hedgers dump Treasury futures to protect positions, which pushes yields higher and further crushes MBS values—a feedback loop that narrows margins. The presence of $2 trillion in higher-coupon securities means this hedging activity will intensify on any significant rate spike. Loan officers locking borrowers now enjoy a 90-day window where origination risk is partially protected, but the Treasury pipeline remains vulnerable to sudden volatility.

Secondary teams should prepare for wider bid-ask spreads on any new economic data shock. Friday’s employment report will determine whether today’s peace-driven rally has staying power. With initial jobless claims already rising to 225K and only modest data remaining this week, the jobs number becomes the market’s sole focus.

If nonfarm payrolls disappoint, expect another 5-10 basis point drop in the 10-year as recession fears resurface. Conversely, strong employment could reignite inflation concerns and push yields back toward the 4.50% resistance level. Mortgage sellers should prepare lock/float strategies around the 4.43 to 4.51 range, which remains the operative trading band until Friday’s print reshapes expectations.

**Locking vs Floating**

War-related headlines continue to create overnight volatility, though market sensitivity to geopolitical shocks has diminished over the past two weeks. Floating positions remain a “coin flip” in this environment rather than a clear advantage. For those trading the narrow 10-year yield range between 4.43 and 4.51, today’s move back toward the higher end suggests short-term locking opportunities.

The convexity hedging dynamic means sudden rate spikes are possible, making overnight floats riskier than the typical pattern would suggest.

**Today’s Events**

Jobless Claims (May/30): 225K vs 213K forecast, 215K prior

Challenger Layoffs (May): 83.387K

Continued Claims (May/23): 1.777M vs 1.780M forecast

**Bond Pricing**

**UMBS 30 yr**

| Coupon | Price | Intra-Day Change |

| 5.0 | 98.22 | 0.19 |

| 5.5 | 100.37 | 0.19 |

| 6.0 | 102.03 | 0.09 |

**GNMA 30 yr**

| Coupon | Price | Intra-Day Change |

| 5.0 | 98.73 | 0.13 |

| 5.5 | 100.56 | 0.09 |

| 6.0 | 101.77 | 0.09 |

**Treasuries**

| Term | Yield | Price | Intra-Day Yield Change |

| 2 yr | 4.035 | 99.696 | -0.047 |

| 5 yr | 4.170 | 98.683 | -0.047 |

| 10 yr | 4.458 | 97.336 | -0.038 |

| 30 yr | 4.966 | 96.649 | -0.025 |