**WTMS Blog Today = What’s up in Mortgage Today (AM) – 06/08/2026**

Friday’s jobs report sent bond investors scrambling as markets priced in a potential Federal Reserve rate hike by December. The U.S. added 172,000 jobs in May—nearly double forecasts—with unemployment holding steady at 4.3%, signaling resilience that could force the Fed to tighten policy to combat sticky inflation.

Treasury yields jumped across the curve, with the 10-year climbing to 4.55% and traders now betting on a 20% chance of a second hike. This repricing caught many off guard after a week of geopolitical uncertainty and energy concerns. The labor market’s strength essentially closed the door on any near-term rate cuts, reshaping expectations heading into Fed Chair Kevin Warsh’s first policy meeting on June 16-17.

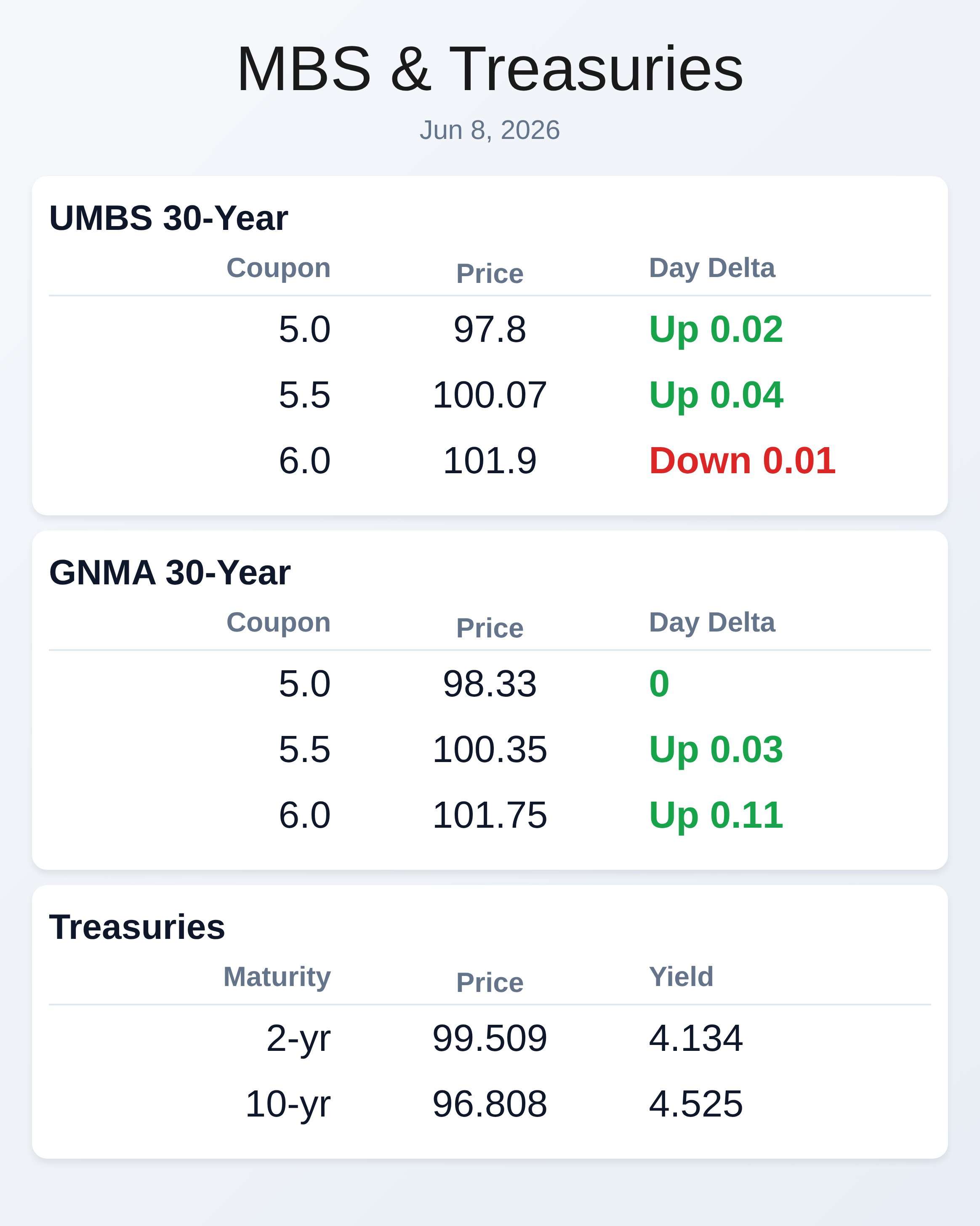

Agency MBS and GNMA securities held ground during the intraday volatility, with five-year and 10-year Treasuries underperforming as the curve flattened further. UMBS 5.5% coupons traded near par at 100.07, while GNMA 6.0% coupons climbed to 101.75, reflecting selective demand in higher-coupon pools. Mortgage originators face a narrowing window to lock borrowers into current rates before a potential summer tightening cycle unfolds.

The prospect of higher-for-longer rates is already pressuring refinance pipelines and will likely weigh on purchase applications as summer progresses. Dallas Fed President Lorie Logan added fuel to rate-hike expectations in comments made before Friday’s jobs release, warning that “higher interest rates could be necessary later this year” given inflation trending toward 4% and corporate earnings remaining robust. Her remarks echoed broader hawkish sentiment across the FOMC, with Goldman Sachs and BNP Paribas now forecasting at least one to three quarter-point hikes starting in December.

This consensus shift signals an abrupt end to the “higher-for-longer hold” narrative and suggests the Fed could surprise markets with tightening rather than cuts. Mortgage rates tied to 10-year Treasuries will likely track higher alongside these expectations, making the next few weeks critical for rate locks. Housing market weakness is amplifying rate concerns as new listings fell 0.8% from April and were down 4.1% year-over-year, according to Zillow data.

Existing-home sales declined 2.9% annually while price cuts became more common, with nearly one in four listings experiencing reductions in May. Homes are taking longer to sell and fewer are commanding premiums over asking price, signaling buyer demand is eroding under higher borrowing costs. This softening inventory and slowing sales activity underscore why mortgage brokers and lenders must act decisively to capture borrowers before rates move higher.

Middle East tensions and energy prices added a second source of rate volatility on Monday as Israel and Iran exchanged missile strikes despite ceasefire talks. Oil prices spiked above $94 per barrel, raising inflation concerns just days before the May Consumer Price Index report on Wednesday. Core CPI is expected to show inflation moderating toward 2.9% year-over-year, but headline inflation could spike to 4.2% due to energy costs, giving the Fed additional ammunition for a hawkish policy pivot.

Geopolitical uncertainty will likely remain a dominant driver of bond market volatility this week. A Florida jury verdict awarding $47.8 million in a buyer broker commission fraud case signals growing legal exposure for brokers and agents as NAR commission guidelines continue shifting post-settlement. The case illustrates how enforcement of buyer broker agreements is becoming increasingly aggressive in court, even when disputes involve relatively small commissions.

Mortgage professionals working with real estate teams should ensure buyer broker agreements are documented and enforceable in their jurisdictions. Industry consolidation also continues with Synergy One Lending merging into American Pacific Mortgage, reflecting ongoing M&A activity as smaller shops seek stability in a tightening rate environment.

**Locking vs Floating**

Job market resilience combined with rising inflation signals that rates have likely peaked for the moment—but remain on a tightening bias rather than a cutting bias.

Markets have fully repriced out near-term Fed cuts and are now booking at least one hike by year-end, making the “lock button” the safer tactical choice unless intraday momentum clearly reverses. Confirmed support on the 10-year around 4.50% would offer a brief window to reassess, but borrowers should expect rates to drift higher into summer.

**Bond Pricing**

**UMBS 30 yr**

| Coupon | Price | Intra-Day Change |

| 5.0 | 97.8 | 0.02 |

| 5.5 | 100.07 | 0.04 |

| 6.0 | 101.9 | -0.01 |

**GNMA 30 yr**

| Coupon | Price | Intra-Day Change |

| 5.0 | 98.33 | 0 |

| 5.5 | 100.35 | 0.03 |

| 6.0 | 101.75 | 0.11 |

**Treasuries**

| Term | Yield | Price | Intra-Day Yield Change |

| 2 yr | 4.134 | 99.509 | -0.012 |

| 3 yr | 4.186 | 98.085 | -0.014 |

| 5 yr | 4.259 | 98.289 | -0.011 |

| 7 yr | 4.386 | 99.186 | -0.009 |

| 10 yr | 4.525 | 96.808 | -0.006 |

| 30 yr | 5 | 96.139 | 0.001 |