**WTMS Blog Today = What’s up in Mortgage Today (AM) – 06/10/2026**

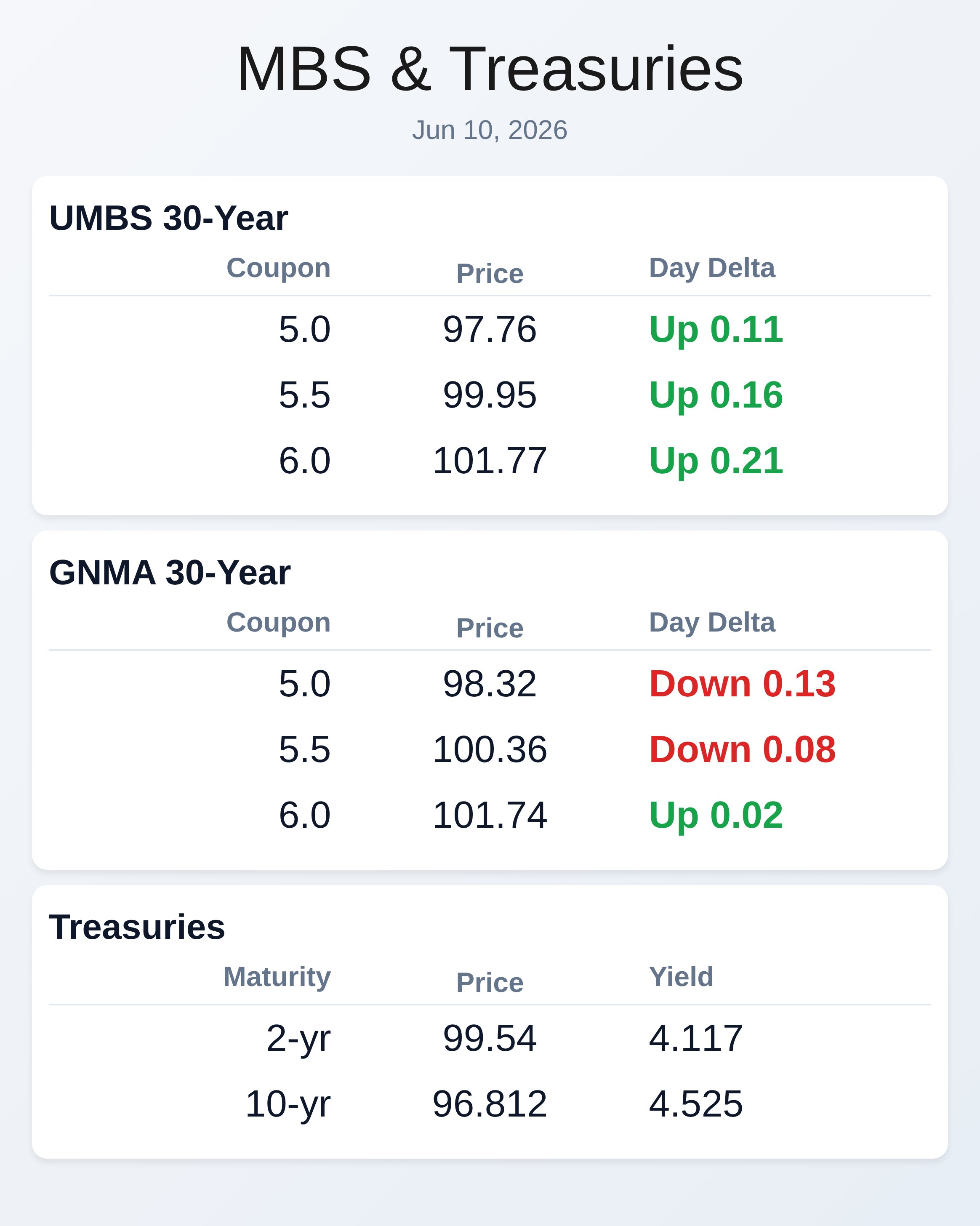

May’s core inflation came in softer than expected at 0.2% month-over-month versus a forecast of 0.3%, giving mortgage markets a modest boost after a volatile week dominated by geopolitical tensions between the U.S. and Iran. The better-than-expected print helped UMBS securities gain ground, with 5.5% coupons climbing to 99.95, while the 10-year Treasury yield pulled back slightly to 4.525% from pre-data levels near 4.538%.

Despite the relief, year-over-year core inflation remains sticky at 2.9%, signaling the Federal Reserve’s inflation challenge is far from solved and rate-cut timing remains uncertain. Mortgage application volume surged 10.8% last week as borrowers capitalized on rate volatility windows created by Middle East headlines, with refinance activity jumping 15% and purchase applications up 7% from the prior week. ARM demand also picked up noticeably, with 5-year ARMs averaging 5.96% and comprising 8.6% of total applications as rate-sensitive borrowers explored alternative structures.

The Mortgage Bankers Association noted that intraday rate swings during Iran ceasefire negotiations gave originators opportunities to lock clients at lower rates during favorable windows throughout the week. The lock-in effect continues reshaping the mortgage market as homeowners pulled a record $47 billion in home equity during Q1 2026, the highest first-quarter total since 2021. Second-lien originations and HELOC borrowing hit 20-year highs, with 248,000 borrowers accessing $25 billion through HELOCs and second liens while another 234,000 did cash-out refis for $22 billion.

Nearly two-thirds of all second-lien volume came from borrowers still holding mortgages from 2020-2022, unwilling to give up those historically low rates and instead tapping equity through junior liens. Mortgage credit availability edged higher in May, with the MBA’s index rising to 108.0, though the gains were modest and concentrated in jumbo ARM offerings as lenders targeted higher-income borrowers less sensitive to rate changes. Government loan programs and conforming credit remained flat, reflecting widespread lender caution amid 9-month rate highs and affordability headwinds that have squeezed purchase activity.

The muted movement signals lenders are holding firm on underwriting standards despite industry pressure, preferring to expand only selective ARM programs rather than loosening traditional credit boxes. Middle East escalation poses significant tail risk to the mortgage market as President Trump authorized new strikes on Iranian targets after tensions over a downed U.S. helicopter threatened peace negotiations.

Oil prices swung sharply on the news, with West Texas Intermediate crude rising 2% and Brent jumping 1.7% to $93 per barrel, raising concerns about energy-driven inflation that could complicate the Fed’s path back to its 2% target. Any sustained oil rally would likely push Treasury yields higher and pressure MBS valuations by increasing expectations for longer-duration rate hikes. Today’s Treasury auction of $39 billion in 10-year notes will test investor appetite in a market grappling with geopolitical uncertainty and sticky inflation readings that keep the Fed sidelined.

The broader economic backdrop remains surprisingly resilient with solid labor markets and consumer spending offsetting recession fears, but the combination of energy price risk and inflation persistence has pushed markets toward a higher-for-longer rate framework. Originators should monitor both the auction results and this afternoon’s Treasury budget data as signals for where rates may settle in the near term.

**Locking vs Floating**

Borrowers with risk tolerance should consider locking purchase rates now given that soft CPI data provided only modest relief and geopolitical risks remain elevated with additional Iranian tensions.

The 4.57% mark represents an overhead resistance level where risk-tolerant clients found previous opportunity, but conservative borrowers should wait for more substantial evidence of bond market support before adopting a neutral rate outlook. Intraday volatility from war headlines creates tactical opportunities but reinforces the case for prudent borrowers to lock today rather than bet on sustained rate improvement.

**Today’s Events**

May Core CPI released at 0.2% month-over-month versus forecast of 0.3%; 2.9% year-over-year versus forecast of 2.9%

May Headline CPI released at 0.5% month-over-month versus forecast of 0.5%; 4.2% year-over-year versus forecast of 4.2%

$39 billion 10-year Treasury note auction scheduled for today

May Treasury Budget statement expected later today

**Bond Pricing**

**UMBS 30 yr**

| Coupon | Price | Intra-Day Change |

**GNMA 30 yr**

| Coupon | Price | Intra-Day Change |

**Treasuries**

| Term | Yield | Price | Intra-Day Yield Change |