WTMS Blog Today = What’s up in Mortgage Today (PM) – 03/02/2026

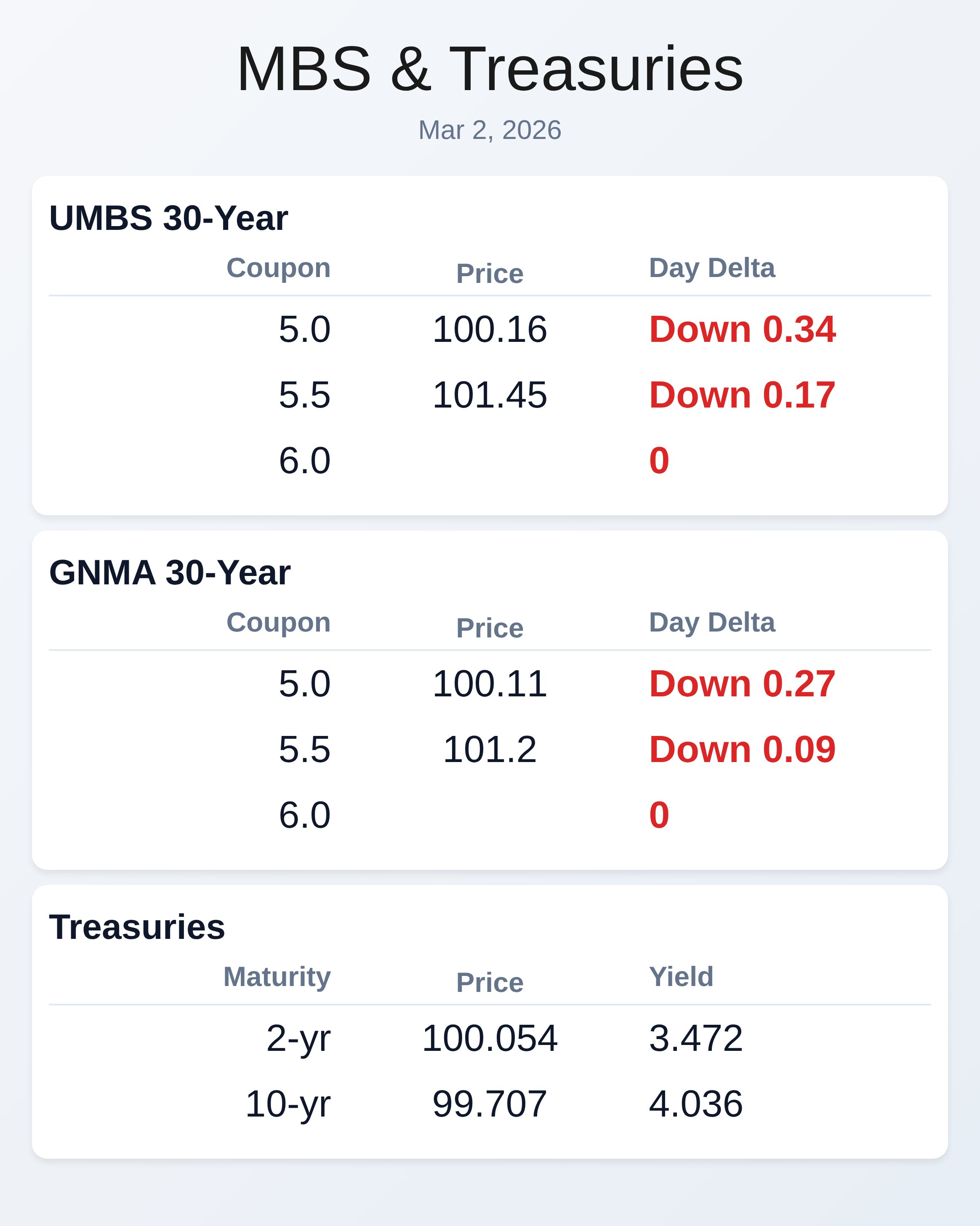

Middle East strikes delivered a one-two punch to mortgage markets today as geopolitical chaos collided with inflation concerns. UMBS 4.5 coupons plummeted 55 basis points while the 10-year Treasury yield surged to 4.036%, marking one of the worst days for bonds in recent memory. Oil prices jumped 7% and gold rocketed past $5,400 per ounce as investors scrambled to assess the fallout from weekend attacks on Iran that killed Ayatollah Khamenei and other senior leaders.

The selloff accelerated throughout the day as traders digested multiple threats to the inflation outlook. Brent crude surged 8% above $79 per barrel after the Strait of Hormuz effectively shut down, cutting off roughly one-fifth of global oil flows. Qatar’s decision to halt production at the world’s largest LNG export facility sent European natural gas prices soaring 52%.

These energy shocks could push gasoline and heating costs higher for American consumers, forcing the Federal Reserve to maintain its current rate stance longer than markets anticipated. Bond markets showed unusual behavior considering the geopolitical turmoil. Despite the classic risk-off environment with stocks down 1% and the dollar rallying, Treasury prices barely budged in what should have been a flight-to-quality trade.

Instead, inflation fears dominated as traders scaled back expectations for rate cuts across the US, UK, and eurozone. The disconnect between soaring gold prices and stagnant Treasury demand signals deep concern about oil-driven inflation overwhelming growth worries. February’s ISM Manufacturing data complicated the picture further with mixed signals on the economy’s health.

The headline PMI came in at 52.4, slightly above the 51.8 forecast but below January’s 52.6 reading, suggesting moderate expansion continues. However, the Prices Paid component exploded to 70.5, crushing the 59.5 forecast and representing the largest upside surprise in months. Manufacturing employment remained in contraction territory at 48.8, barely improving from last month’s 48.1 reading.

GNMA securities held up marginally better than UMBS today, though both took severe losses. The GNMA 4.5 coupon dropped 48 basis points compared to UMBS 4.5’s 55-basis-point decline, while higher coupons showed more resilience across both security types. GNMA 5.5 fell only 9 basis points versus UMBS 5.5’s 17-basis-point drop.

This pattern reflects investor preference for higher-yielding paper during selloffs when prepayment risk diminishes. Housing industry trade groups chose an interesting moment to push regulators for easier mortgage capital rules. A coalition including the Mortgage Bankers Association and American Bankers Association urged the Federal Reserve and FDIC to reduce Basel III requirements they claim have driven banks out of mortgage lending.

Bank servicing share collapsed from 88% in 2013 to just 39% in 2024 under current capital standards. The groups propose recognizing private mortgage insurance, lowering risk weights, and reducing warehouse lending charges to bring banks back into the market. Meanwhile, demographic shifts suggest modest improvements in housing affordability may be taking hold.

Redfin reported the median age of first-time homebuyers dropped to 35 years old in 2025 from 36 the previous year, reversing a long-term trend that peaked at 38 in 2018. The report credits slight easing in home-price growth and modestly lower mortgage rates for enabling younger buyers to enter the market. Repeat buyers also skewed younger, with median age falling to 47 from last year’s quarter-century high of 52.

Locking vs Floating

Last Friday’s warning about potential month-end technical selling proved prescient as today’s action exceeded even pessimistic expectations. Geopolitical volatility creates an unpredictable backdrop, but incoming economic data will ultimately determine the market’s direction over coming weeks. The explosive Prices Paid reading from ISM Manufacturing confirms inflation pressures remain stubborn and widespread across the manufacturing sector.

With MBS prices down more than half a point today and yields jumping nearly 10 basis points, borrowers floating rate locks face significant deterioration. Deals closing within the next three to four weeks should lock immediately to protect against further damage. The combination of geopolitical uncertainty, oil-driven inflation fears, and strong economic data creates too many downside risks for floating to make tactical sense.

Today’s Events

ISM Manufacturing Employment (Feb): 48.8 vs no forecast, 48.1 previous

ISM Manufacturing PMI (Feb): 52.4 vs 51.8 forecast, 52.6 previous

ISM Mfg Prices Paid (Feb): 70.5 vs 59.5 forecast, 59.0 previous

Bond Pricing

UMBS 30 yr

| Coupon | Price | Intra-Day Change |

| 5.0 | 100.16 | -0.34 |

| 5.5 | 101.45 | -0.17 |

| 5.0 | 100.11 | -0.27 |

GNMA 30 yr

| Coupon | Price | Intra-Day Change |

Treasuries

| Term | Yield | Price | Intra-Day Yield Change |

| 2 yr | 3.472 | 100.054 | 0.09 |

| 3 yr | 3.479 | 100.061 | 0.095 |

| 5 yr | 3.609 | 100.642 | 0.101 |

| 7 yr | 3.806 | 101.184 | 0.098 |

| 10 yr | 4.036 | 99.707 | 0.088 |

| 30 yr | 4.675 | 99.201 | 0.055 |