WTMS Blog Today = What’s up in Mortgage Today (PM) – 03/03/2026

Mortgage bonds staged an impressive afternoon comeback after getting hammered overnight on Middle East tensions. UMBS prices recovered from morning losses of 28 basis points to finish down just 16 basis points by the close. The 10-year Treasury yield pulled back from its morning peak of 4.099% to settle at 4.062%, erasing most of the damage from the overnight session.

Energy markets dominated the morning narrative as Iran escalated attacks on Gulf infrastructure. Oil prices surged 7% while natural gas and gasoline futures jumped 5% after Iran threatened to attack ships passing through the Strait of Hormuz. This critical waterway handles about 20% of global oil supply, making any disruption a major market event.

The correlation between rising oil prices and higher bond yields initially suggested inflation fears were driving the selloff. However, market-based inflation expectations measured by TIPS showed almost no movement over the past two days. This disconnect suggests the real culprit is likely increased Treasury issuance related to military spending rather than pure inflation concerns.

Manufacturing data painted a picture of cautious expansion with growing uncertainty. The ISM Manufacturing Index showed activity still expanding but at a slower pace than January as new orders and production decelerated. Tariff concerns dominated manufacturer comments, though one bright spot emerged in the employment picture where companies reported success hiring skilled workers after years of labor shortages.

The employment shift reveals something important about labor market dynamics. Young workers are increasingly choosing skilled trades over college degrees with negative returns. One fabricated metals producer noted hiring experienced engineers and CNC operators in recent months after spending thousands with zero responses over the previous five years.

Treasury yields initially climbed despite geopolitical conflict, defying the typical flight-to-safety pattern. The 10-year yield had already fallen from 4.23% to current levels during the January military buildup, making yesterday’s action more of a “sell the fact” trade. President Trump indicated the conflict could continue for weeks, creating extended uncertainty around shipping routes and potential supply disruptions.

The duration of the conflict matters significantly for debt markets and Fed policy. Extended fighting increases the likelihood of higher Treasury issuance beyond the current $39 trillion debt level, which represents 115% of GDP. It also raises the probability of Fed easing measures including rate cuts or even quantitative easing, both of which fuel inflation concerns that bonds particularly dislike.

Federal Reserve officials continue showing no consensus on the appropriate policy path forward. Members focused on labor market health advocate for additional rate cuts while inflation hawks prefer waiting for more progress before easing. Fed Governor Waller’s recent remarks about maintaining adequate reserves add another layer to the ongoing balance sheet debate.

The afternoon recovery in bonds suggests traders are questioning the higher-for-longer narrative. While smaller traders may be connecting oil spikes directly to sustained inflation, larger institutional players see more nuanced dynamics at work. Gold absorbed much of the traditional safe-haven flows, acting as an inflation hedge while bonds struggled.

Locking vs Floating

Volatility remains dangerously elevated with geopolitical uncertainty and incoming economic data creating unpredictable swings. Tuesday’s afternoon recovery provided modest relief, but only the most aggressive risk-takers should view this as a signal to float. Most originators should wait for sustained evidence that the recent weakness has truly ended before exposing clients to float risk.

The technical recovery from morning lows shows some market resilience. MBS prices improved from down three-eighths to down just one-eighth by mid-afternoon before settling slightly worse at the close. This intraday pattern suggests some buyer interest exists at current levels, though conviction remains limited.

Today’s Events

No economic data releases scheduled.

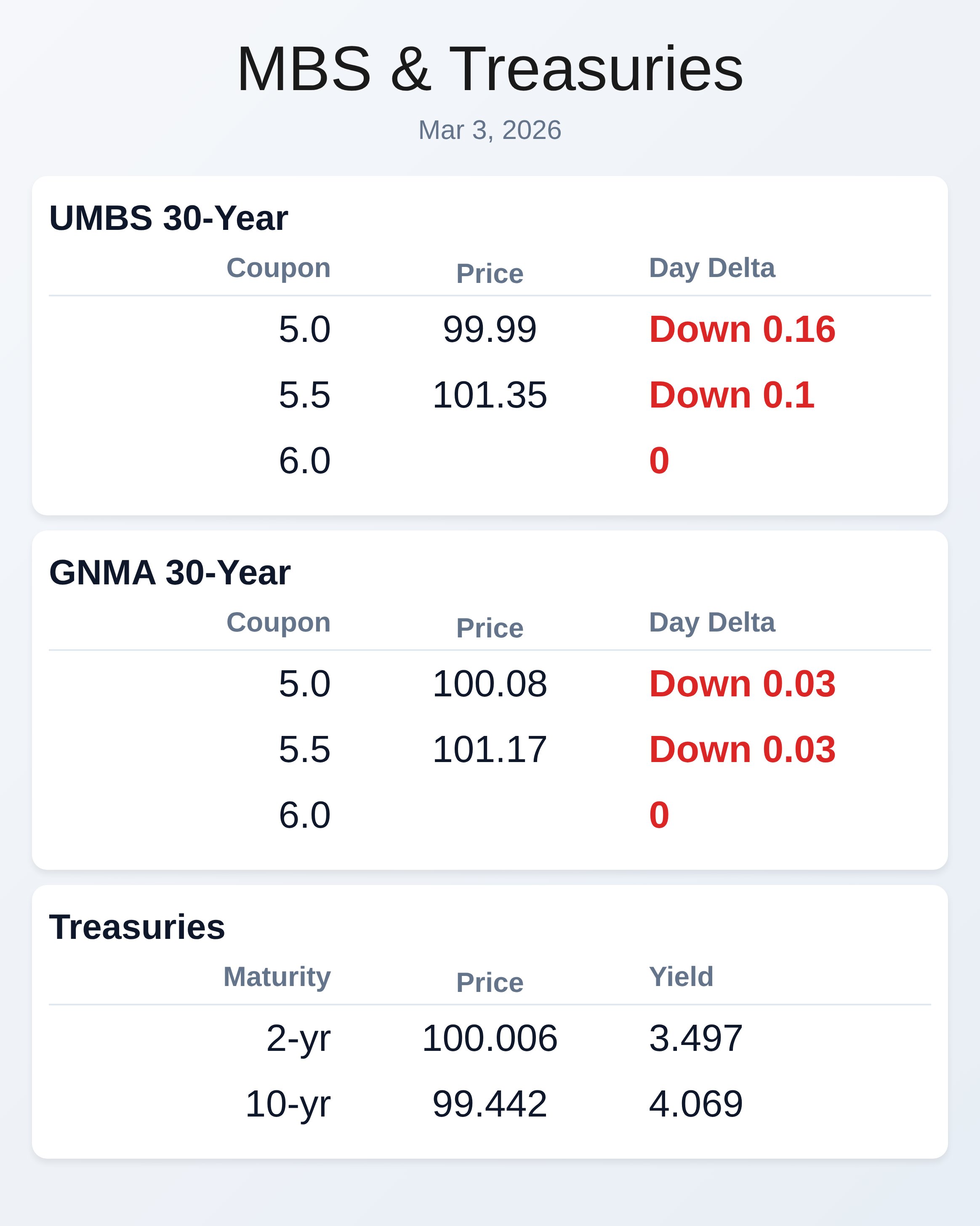

Bond Pricing

UMBS 30 yr

| Coupon | Price | Intra-Day Change |

| 5.0 | 99.99 | -0.16 |

| 5.5 | 101.35 | -0.1 |

| 5.0 | 100.08 | -0.03 |

GNMA 30 yr

| Coupon | Price | Intra-Day Change |

Treasuries

| Term | Yield | Price | Intra-Day Yield Change |

| 2 yr | 3.497 | 100.006 | 0.02 |

| 3 yr | 3.515 | 99.958 | 0.032 |

| 5 yr | 3.648 | 100.464 | 0.036 |

| 7 yr | 3.843 | 100.959 | 0.034 |

| 10 yr | 4.069 | 99.442 | 0.031 |

| 30 yr | 4.704 | 98.738 | 0.021 |