WTMS Blog Today = What’s up in Mortgage Today (PM) – 03/05/2026

The mortgage trigger lead industry ended today as the Homebuyers Privacy Protection Act took effect. Credit reporting agencies can no longer sell trigger leads unless the lender already originated or services that borrower’s loan, or the consumer explicitly opted in. For originators who don’t retain servicing, this eliminates a major lead source overnight and forces an immediate pivot to referral-based marketing strategies.

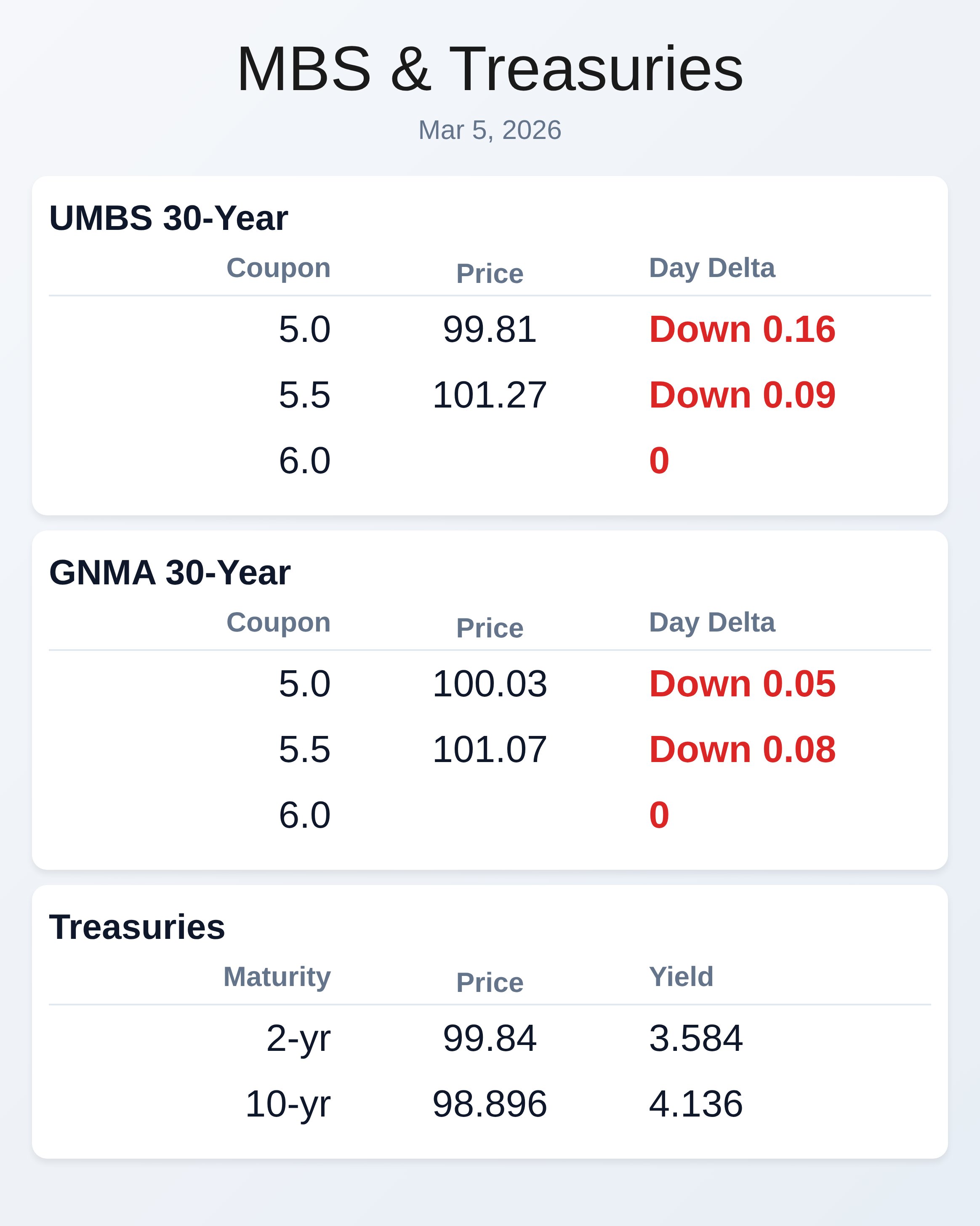

Geopolitical chaos dominated bond markets as the Iran conflict pushed oil prices toward $83 per barrel. The 10-year Treasury yield broke through 4.10% and climbed to 4.14%, up 4.3 basis points on the day. UMBS 5.0 coupons dropped 19 basis points to 99.78, the worst single-day performance in two weeks.

Energy price spikes are creating an unusual market dynamic. Markets are pricing in less Fed easing, with expectations dropping from 60 basis points of cuts last week to just 41 basis points by year-end. The 2-year Treasury jumped 23 basis points as traders bet inflation concerns will keep the Fed sidelined longer than previously expected.

Nearly one million people were impacted by a phishing attack on Figure Technology Solutions, highlighting cybersecurity vulnerabilities across mortgage banking. The incident serves as a critical reminder that post-breach response matters more than the breach itself. Figure detected and contained the attack within one day, immediately notified regulators, and offered credit monitoring to affected consumers—actions that substantially reduce enforcement risk compared to slower responses.

Historical data from recent mortgage industry breaches shows dramatic cost differences based on response speed. Bayview Asset Management and Flagstar Bank faced $46 million and $35 million in combined penalties respectively after slow detection and poor regulatory cooperation. By contrast, Mr.

Cooper and LoanDepot detected breaches within 24 hours and faced significantly lower per-customer costs despite affecting 14.7 million and 16.9 million customers. Home relistings hit a record high in January with nearly 45,000 homes returning to market after being previously delisted in 2025. This represents 3.6% of all active listings and signals sellers are preparing for spring activity.

The relisting surge suggests homeowners are testing pricing strategies as they navigate elevated mortgage rates that remain stubbornly high despite earlier optimism. The U.S. Navy torpedoed an Iranian warship near Sri Lanka in the first submarine attack on an enemy vessel since World War II.

The IRIS Dena, nicknamed “Soleimani” after the Iranian general killed in 2020, had more than 170 people aboard. Sri Lankan authorities rescued 32 survivors while roughly 140 remain missing, intensifying concerns about prolonged disruption to the Strait of Hormuz oil shipping lanes. Treasury yields rose through higher real rates rather than inflation expectations, creating a puzzling market reaction.

The 10-year inflation expectation stalled near 230 basis points even as front-end yields sold off sharply. This suggests markets view energy price spikes as a consumer tax that drags economic growth rather than fuel for sustained inflation, yet the Fed is priced for fewer cuts anyway. Challenger job cuts data showed U.S.

employers announced 48,307 layoffs in February, down 55% from January’s 108,435 cuts. Through February, employers announced 156,742 job cuts—the lowest January-to-February total since 2022. Morgan Stanley announced layoffs of 3% of its workforce as financial sector consolidation continues amid margin pressure.

The yield curve continued its flattening trend for the 13th time in the last 15 sessions. This persistent flattening typically signals recession concerns, yet unemployment remains near historic lows. The disconnect between curve positioning and labor market strength creates uncertainty about whether mortgage rates will finally decline or remain elevated through 2026.

Locking vs Floating

Volatility risk remains much higher than normal amid geopolitical uncertainty and Friday’s jobs report. Only the most risk-tolerant clients should consider floating based on Tuesday’s brief support. Everyone else is waiting for firmer evidence that the bleeding has stopped before making rate commitments.

Today’s Events

Challenger layoffs (Feb): 48,307K vs 108,435K prev

Continued Claims (Feb 21): 1,868K vs 1,850K forecast, 1,833K prev

Import prices (Jan): 0.2% vs 0.2% forecast, 0.1% prev

Jobless Claims (Feb 28): 213K vs 215K forecast, 212K prev

Bond Pricing

UMBS 30 yr

| Coupon | Price | Intra-Day Change |

| 5.0 | 99.78 | -0.19 |

| 5.5 | 101.28 | -0.09 |

| 5.0 | 99.97 | -0.11 |

GNMA 30 yr

| Coupon | Price | Intra-Day Change |

Treasuries

| Term | Yield | Price | Intra-Day Yield Change |

| 2 yr | 3.596 | 99.816 | 0.049 |

| 3 yr | 3.612 | 99.686 | 0.054 |

| 5 yr | 3.738 | 100.056 | 0.045 |

| 7 yr | 3.929 | 100.43 | 0.057 |

| 10 yr | 4.141 | 98.853 | 0.041 |

| 30 yr | 4.75 | 98.015 | 0.018 |