WTMS Blog Today = What’s up in Mortgage Today (PM) – 03/12/2026

Mortgage markets took another beating Thursday as geopolitical tensions continued to dominate trading. MBS dropped 3/8ths of a point while the 10-year Treasury yield climbed to 4.27%, its highest level since early February. The bond market is staging what can only be described as a war protest, with no end to the Iran conflict in sight.

Oil prices surged 9% after Iran’s new Supreme Leader Mojtaba Khamenei vowed to keep the Strait of Hormuz closed until U.S. and Israeli attacks cease. This critical shipping channel normally carries one-fifth of the world’s oil supply, and its closure is causing what the International Energy Agency calls the biggest oil supply disruption in history.

Two fuel tankers were set ablaze in Iraqi waters, and Iraq has completely suspended oil port operations following the attacks. The inflationary implications are keeping the Federal Reserve firmly on the sidelines. Fed funds futures now price in just 30 basis points of cuts by year-end, down from 50 basis points a few weeks ago, with most economists expecting the first cut in June at the earliest.

The 2-year Treasury yield hit 3.75%, its highest level since August, as traders pushed back expectations for monetary policy relief. Housing data delivered a mixed message for mortgage originators. January housing starts jumped 7.2% to 1.487 million units, crushing expectations of 1.35 million, but the details reveal a lopsided recovery.

Multi-unit developments surged 29.1% to their highest level in over a year, while single-family starts fell 2.8% and building permits dropped 5.4% month-over-month. The labor market continues to show resilience despite February’s surprise job losses. Initial jobless claims fell to 213,000, slightly below expectations, while continuing claims dropped to 1.85 million.

This stability gives the Fed room to stay patient on rate cuts even as gasoline prices have jumped 20% since the war began. Industry developments paint a challenging picture for lenders navigating this volatile environment. Radian Group announced it’s shutting down its mortgage conduit business entirely rather than selling it, choosing to refocus on its core mortgage insurance operations.

Meanwhile, loanDepot reported $8.04 billion in Q4 originations, its highest quarterly volume since 2022, showing that well-positioned lenders can still gain market share. Interestingly, homebuyers haven’t panicked yet despite the war and rising oil prices. An Ipsos poll commissioned by Redfin found that just one in four Americans has delayed big-ticket purchases like homes and cars due to the Iran conflict.

However, home price appreciation slipped into negative territory in February according to Clear Capital, suggesting affordability pressures are finally catching up to demand.

Locking vs Floating

Volatility risk remains elevated due to ongoing geopolitical uncertainty and oil market disruptions. March has been uniformly bearish for rates so far, with no signs of the trend reversing.

It makes sense to remain defensive and lock near-term closings until the bearish streak clearly levels off.

Today’s Events

– Building Permits (Jan): 1.376M vs 1.41M forecast, 1.455M previous

– Continued Claims (Feb 28): 1,850K vs 1,850K forecast, 1,868K previous

– Housing Starts (Jan): 1.487M vs 1.35M forecast, 1.404M previous

– Jobless Claims (Mar 7): 213K vs 215K forecast, 213K previous

– Trade Gap (Jan): -$54.50B vs -$66.6B forecast, -$70.3B previous

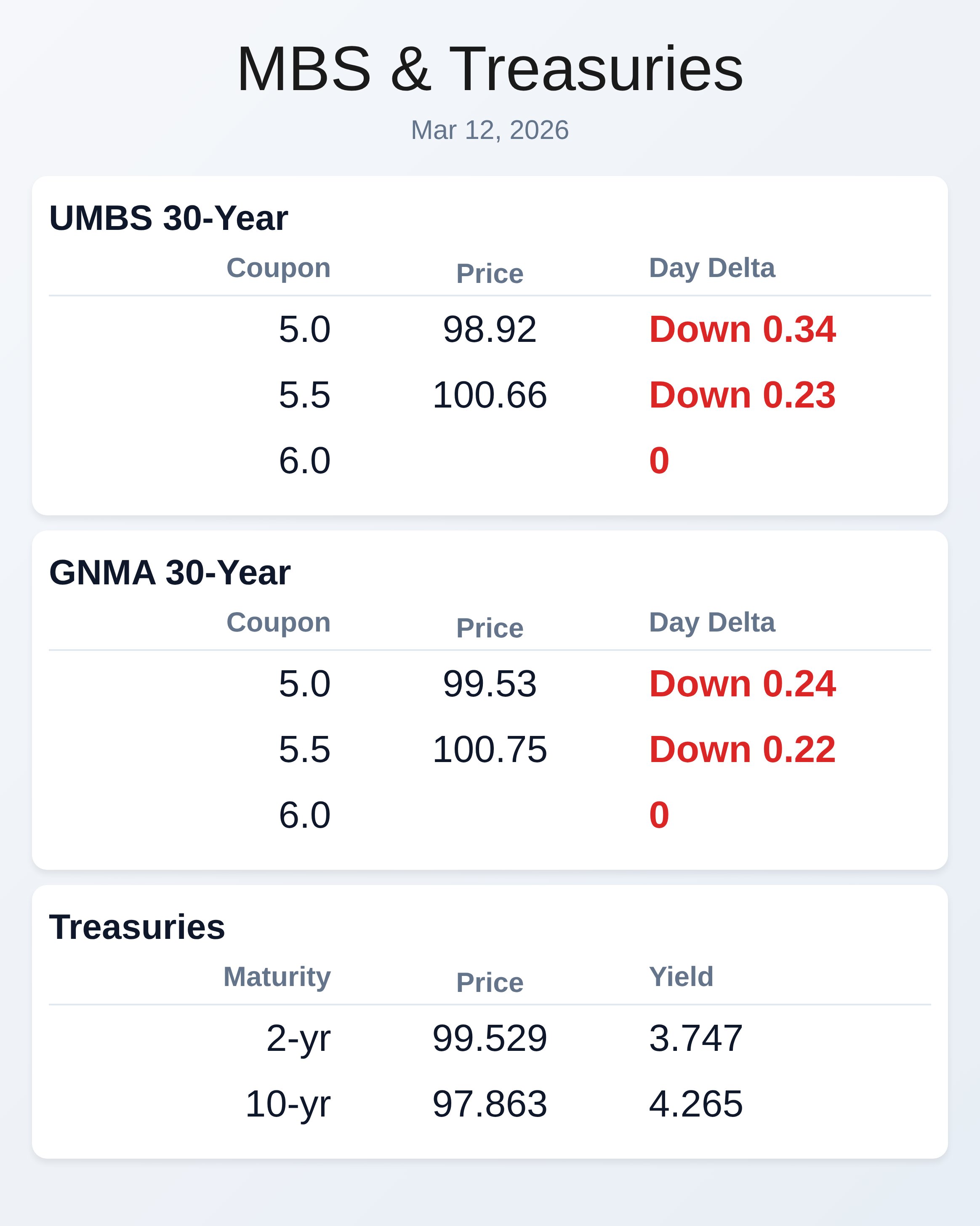

Bond Pricing

UMBS 30 yr

| Coupon | Price | Intra-Day Change |

| 5.0 | 98.92 | -0.34 |

| 5.5 | 100.66 | -0.23 |

| 5.0 | 99.53 | -0.24 |

GNMA 30 yr

| Coupon | Price | Intra-Day Change |

Treasuries

| Term | Yield | Price | Intra-Day Yield Change |

| 2 yr | 3.747 | 99.529 | 0.096 |

| 3 yr | 3.761 | 99.265 | 0.089 |

| 5 yr | 3.872 | 99.449 | 0.072 |

| 7 yr | 4.054 | 99.671 | 0.053 |

| 10 yr | 4.265 | 97.863 | 0.038 |

| 30 yr | 4.882 | 95.973 | 0.005 |