WTMS Blog Today = What’s up in Mortgage Today (PM) – 03/17/2026

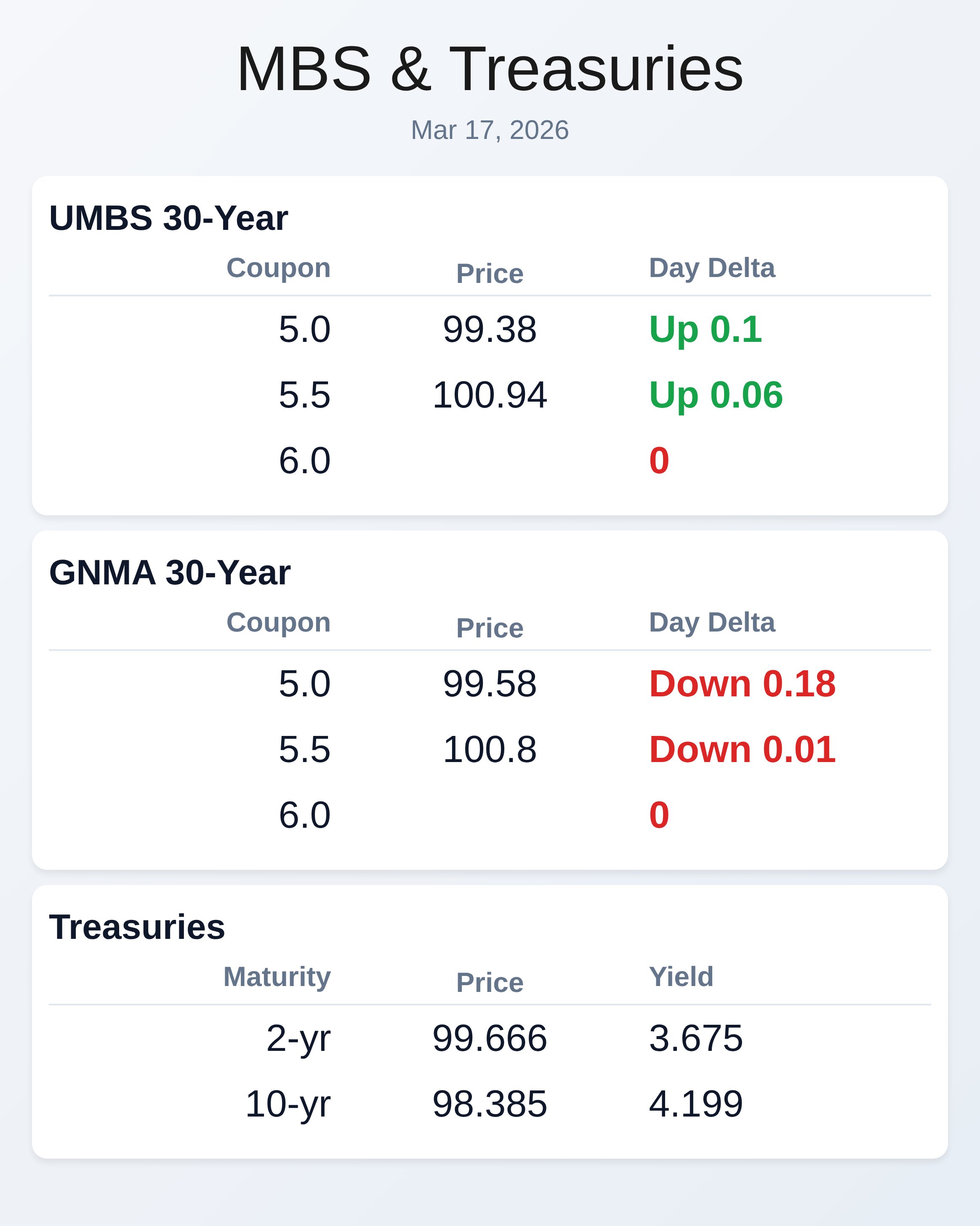

Mortgage pricing improved modestly Tuesday despite geopolitical turmoil continuing in the Middle East, offering a rare bright spot in what has been a difficult March for rates. The 10-year Treasury yield dropped back below the key 4.20% level to settle at 4.199%, while UMBS 5.0 coupons gained 10 basis points. This marks the second consecutive day of improvement, the first time bonds have closed stronger for two straight sessions since late February.

Oil prices climbed above $101 per barrel as Iran renewed attacks on UAE energy infrastructure, yet bonds rallied anyway, breaking the recent pattern where rates moved in lockstep with crude. Brent crude has surged more than 40% since the U.S.-Israeli conflict with Iran began three weeks ago, with the Strait of Hormuz remaining largely closed and disrupting roughly 20% of global oil flows. The disconnect between rising oil and falling yields today suggests markets may be pricing in either a swift resolution or accepting that central banks will look through this supply shock.

The Federal Reserve began its two-day policy meeting Tuesday with no rate change expected, but all eyes are on Wednesday’s updated economic projections and the so-called “dot plot” of future rate expectations. Markets currently price in just one 25-basis-point cut in 2026, down from expectations of two cuts before the Iran conflict erupted. Australia’s central bank kicked off a historic week of central bank meetings by raising rates 25 basis points to 4.1%, citing material inflation risks from the oil shock.

Housing data provided a mixed signal as pending home sales unexpectedly rose 1.8% in February, fueled by the brief dip in mortgage rates early in the year when rates touched 6.1%. However, that improvement is already fading as rates have climbed back above 6.2% amid the geopolitical crisis. The National Association of Realtors warned that further gains are likely limited if oil prices continue pushing mortgage rates higher.

A Reuters survey of housing analysts painted a sobering picture for the next two years, forecasting home prices will rise just 1.8% in 2026 and 2.5% in 2027 as the market remains constrained by high mortgage rates and housing shortages. The survey estimated the U.S. needs 2.5 million additional homes to meet current demand, with nearly 80% of respondents saying it would take more than five years to close that gap.

Lawrence Yun, NAR’s chief economist, warned that mortgage rates could hit 7.0% if the Iran conflict persists. On the servicing front, Freedom Mortgage announced a definitive agreement to acquire Seneca Mortgage Servicing and its mortgage servicing rights portfolio from EJF Capital. The transaction aims to enhance operational efficiency and create new opportunities for outside investors in mortgage loan assets.

Meanwhile, physician mortgages are gaining traction in the prime private-label RMBS market, according to a new KBRA report, creating opportunities for originators who understand how to work with medical professionals and their nontraditional income profiles. In regulatory news, a federal judge dismissed criminal subpoenas targeting Fed Chair Jerome Powell, ruling they were intended to pressure him to lower interest rates. The decision reinforces legal protections for Fed independence, though it underscores how central bank autonomy is increasingly being defended in courts rather than through longstanding political norms.

Two Harbors Investment Corp. adjourned its special shareholder meeting and delayed a key vote on its proposed acquisition by UWM Holdings as it seeks additional shareholder support. Economic data showed weakness as ADP’s weekly employment report revealed its biggest drop in months, with private payrolls increasing just 9,000 per week versus the 14,750 revised figure.

New York Fed manufacturing came in at -0.2 versus a 3.2 forecast and 7.1 prior reading. Treasury auctions continue this week with $13 billion in 20-year bonds Tuesday afternoon, followed by key data Wednesday including the FOMC decision, Powell’s press conference, and PPI figures.

Locking vs Floating

Volatility remains elevated due to geopolitical uncertainty and the ongoing Iran conflict making rate movements unpredictable.

March has been uniformly bearish for rates, and despite two consecutive days of modest improvement, it’s premature to call this a trend reversal. Exercise caution with floating strategies until the bearish streak has clearly leveled off, which will require more than just two positive sessions to confirm. Remember that false hope emerged on March 6th and 9th before rates resumed their climb higher.

Today’s Events

– NY Fed Manufacturing: -0.2 vs 3.2 forecast, 7.1 previous

– ADP Employment Change Weekly: 9k vs 15.5k expected

– Pending Home Sales: +1.8% vs -0.5% forecast

– 20-Year Treasury Auction: $13 billion

Bond Pricing

UMBS 30 yr

| Coupon | Price | Intra-Day Change |

| 5.0 | 99.38 | 0.1 |

| 5.5 | 100.94 | 0.06 |

| 5.0 | 99.58 | -0.18 |

GNMA 30 yr

| Coupon | Price | Intra-Day Change |

Treasuries

| Term | Yield | Price | Intra-Day Yield Change |

| 2 yr | 3.675 | 99.666 | -0.003 |

| 3 yr | 3.678 | 99.499 | -0.004 |

| 5 yr | 3.794 | 99.8 | -0.005 |

| 7 yr | 3.981 | 100.113 | -0.016 |

| 10 yr | 4.199 | 98.385 | -0.023 |

| 30 yr | 4.842 | 96.582 | -0.027 |