# WTMS Blog Today = What’s up in Mortgage Today (PM) – 03/18/2026

Oil spikes and inflation data shattered any optimism in the mortgage market Wednesday, sending rates back toward recent highs and crushing refinance demand. The 30-year fixed rate jumped to 6.30% last week, the highest level of 2026, driving a 19% week-over-week drop in refinance applications. The culprit was a double hit from the ongoing U.S.-Israel war with Iran and a hotter-than-expected Producer Price Index report showing wholesale inflation surged 0.7% in February, well above the 0.3% forecast.

Purchase applications managed a 1% gain and remain 12% above last year’s levels, offering a thin silver lining as the spring buying season approaches. But with oil prices now topping $108 per barrel after Israeli strikes on Iran’s South Pars gas field, the outlook for mortgage rates in the near term has darkened considerably. Fed Holds Steady, Signals No Relief Coming

The Federal Reserve held rates steady in the 3.50%-3.75% range Wednesday, projecting only one rate cut for all of 2026 despite mounting economic uncertainty from the Iran conflict.

The Fed’s updated economic projections showed inflation ending 2026 at 2.7%, higher than the 2.4% forecast in December, as policymakers acknowledged the oil shock could keep price pressures elevated. Chair Jerome Powell’s press conference proved more hawkish than markets anticipated, with Powell emphasizing disappointing progress on core goods and non-housing services inflation beyond the energy spike. Fed Governor Stephen Miran continued his dissent streak, voting for an immediate rate cut, but the broader committee stayed unified in its cautious stance.

Markets responded by pushing expectations for the next rate cut beyond a year out, a dramatic shift from earlier projections of multiple cuts in 2026. Oil Shock Drives Market Volatility

Crude oil prices exploded higher Wednesday after Iran’s Revolutionary Guards threatened retaliatory strikes on energy facilities across Saudi Arabia, the UAE, and Qatar following the Israeli attack on Iran’s Pars gas field. Brent crude surged past $108 per barrel while West Texas Intermediate climbed above $98, widening the discount to Brent to levels not seen since 2019.

The conflict has effectively shut down the Strait of Hormuz, which handles 20% of global oil and LNG supply, with total Middle East output cuts estimated at 7 to 10 million barrels per day. U.S. gasoline prices have now risen roughly 28% since the war began, hitting $3.84 per gallon and approaching levels that historically trigger consumer spending pullbacks.

The Trump administration announced a 60-day Jones Act waiver to allow foreign vessels to move fuel between U.S. ports, but supply relief remains limited with Iraqi production still at only one-third of pre-crisis levels. Bond Market Suffers Worst Day in Weeks

Treasury yields jumped to near recent highs as bonds sold off sharply following the PPI data and Powell’s hawkish commentary.

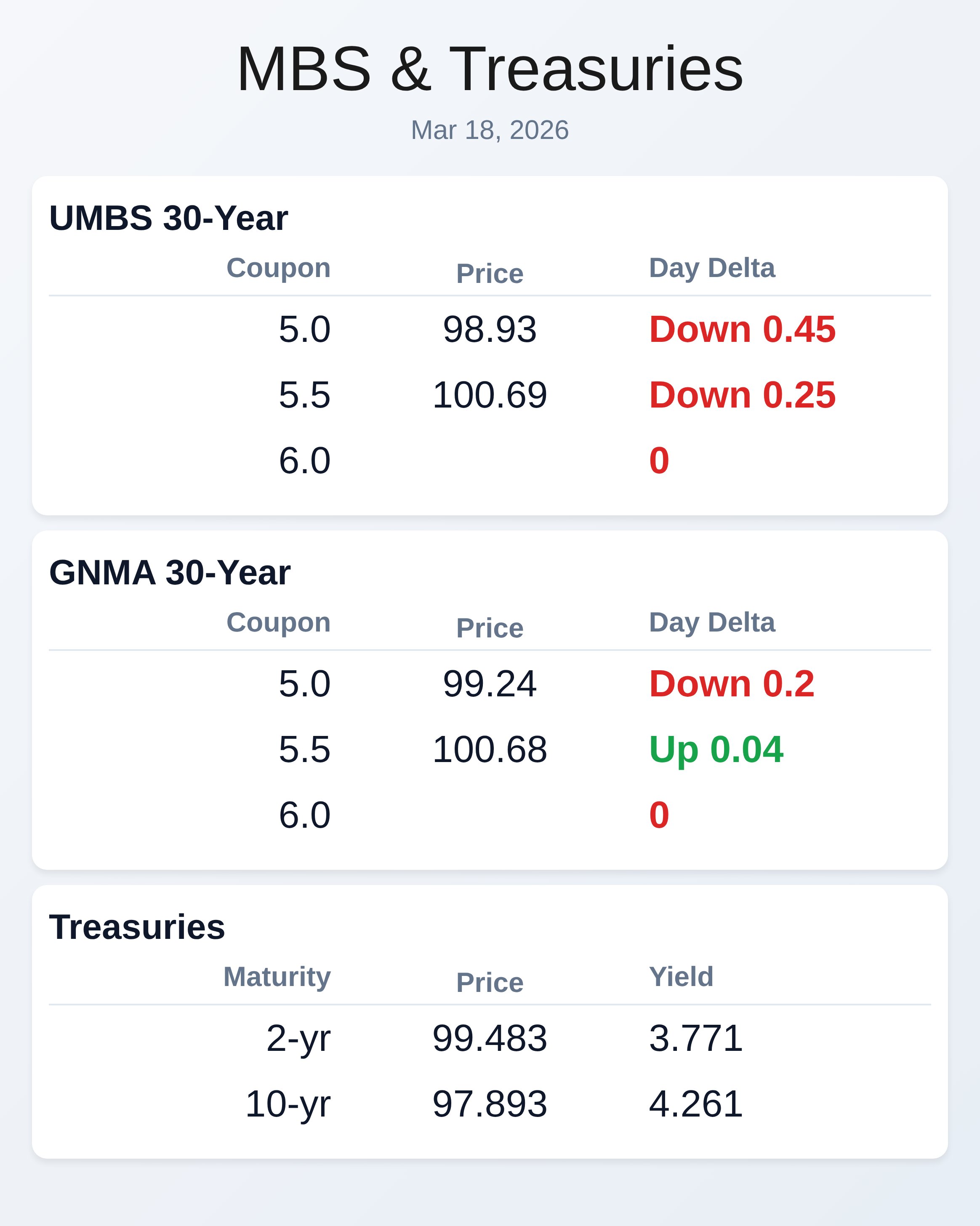

The 10-year Treasury yield rose 6.3 basis points to 4.261%, while the 2-year climbed 9.7 basis points to 3.771% as traders repriced rate cut expectations. UMBS prices fell nearly half a point, with the 5.0 coupon dropping 0.45 to 98.93, triggering negative reprice warnings from lenders in afternoon trading. The yield curve continued flattening for a third straight session, with the 2-year to 10-year spread narrowing to under 50 basis points, the flattest since late November.

Volume and volatility were surprisingly muted during the Fed announcement itself, but picked up dramatically during Powell’s press conference when he shifted focus away from energy prices to underlying inflation concerns. CFPB Wins Funding Fight in Federal Court

A federal judge ruled Wednesday that the Consumer Financial Protection Bureau must continue drawing its funding from the Federal Reserve, rejecting acting director Russell Vought’s legal argument that the agency couldn’t access funds unless the Fed was profitable. Vought, who publicly stated he was working to “close down the agency,” had stopped requesting Fed funds and instead sought congressional appropriations, which the judge called “arbitrary, capricious and in violation of law.” The ruling came after three nonprofits that rely on CFPB lending data sued, arguing the funding cutoff would effectively shut down the agency and eliminate access to fair lending data.

The decision ensures the CFPB can continue operations for now, though the broader political battle over the agency’s future remains unresolved. The mortgage industry has watched the CFPB funding fight closely, as the agency’s regulations touch nearly every aspect of residential lending. Housing Market Shows Mixed Signals

Pending home sales rose 1.8% in February, beating expectations and offering a rare bright spot in an otherwise gloomy housing picture.

But the data reflects contracts signed before the Iran war began and mortgage rates jumped, raising questions about whether the momentum can continue. Homebuilder sentiment ticked up one point to 38 in March but remains below the 50 break-even mark for the 23rd straight month, with nearly two-thirds of builders offering sales incentives and 37% cutting prices. Foreclosure filings are rising while affordability pressures intensify as tariffs squeeze material costs, immigration enforcement thins the construction labor pool, and now energy prices threaten to push overall inflation higher.

The mortgage market faces a challenging spring season with rates moving in the wrong direction just as inventory typically increases.

Locking vs Floating

The Fed’s hawkish stance and renewed volatility from geopolitical uncertainty make floating risky in the near term. Rates have generally moved one direction throughout March with only brief corrective moments, and the addition of Fed commentary emphasizing persistent inflation concerns beyond oil adds to upward pressure.

With energy prices still climbing and the market now pricing no rate cuts until late 2027, waiting for a definitive market turn before taking floating risks appears prudent. The Fed’s reaction added more volatility than expected to an already volatile environment dominated by the ongoing Iran conflict.

Today’s Events

– Core PPI m/m (Feb): 0.5% vs 0.3% forecast, 0.8% prior

– Core PPI y/y (Feb): 3.9% vs 3.7% forecast, 3.6% prior

– PPI m/m (Feb): 0.7% vs 0.3% forecast, 0.5% prior

– PPI y/y (Feb): 3.4% vs 2.9% forecast, 2.9% prior

– FOMC Economic Projections

– Fed Interest Rate Decision: 3.75% (unchanged)

– Fed Press Conference

Bond Pricing

UMBS 30 yr

| Coupon | Price | Intra-Day Change |

| 5.0 | 98.93 | -0.45 |

| 5.5 | 100.69 | -0.25 |

| 5.0 | 99.24 | -0.2 |

GNMA 30 yr

| Coupon | Price | Intra-Day Change |

Treasuries

| Term | Yield | Price | Intra-Day Yield Change |

| 2 yr | 3.771 | 99.483 | 0.097 |

| 3 yr | 3.777 | 99.222 | 0.099 |

| 5 yr | 3.877 | 99.429 | 0.09 |

| 7 yr | 4.058 | 99.648 | 0.079 |

| 10 yr | 4.261 | 97.893 | 0.063 |

| 30 yr | 4.884 | 95.95 | 0.041 |