WTMS Blog Today = What’s up in Mortgage Today (PM) – 04/06/2026

UWM CEO Mat Ishbia has been ordered to sit for a deposition as part of the ongoing “All-In” litigation, marking an escalation that has legal experts taking notice. Depositions at the CEO level are rare, typically reserved for cases where courts believe there’s direct involvement or unique knowledge at the top level. UWM’s immediate response was an emergency motion to block the deposition, arguing other executives could testify instead.

The “All-In” policy remains one of the most consequential wholesale channel moves in recent years, continuing to shape broker relationships and business flow patterns. This litigation keeps that policy—and its enforcement strategy—squarely in the spotlight as it potentially reaches the highest executive levels. FICO pricing pressure is hitting originators hard, with tri-merge credit costs now hovering around $540 per file according to Community Home Lenders of America criticism.

Credit pulls that were once routine line items are now cutting significantly into margins and forcing earlier, harder pipeline decisions. VantageScore is pushing back with studies showing that better pre-screening can reduce wasted files and improve pull-through rates, especially for first-time buyers. The real question for loan officers isn’t about scoring models—it’s whether lenders can move fast enough to implement cost-saving alternatives.

In today’s margin environment, anything that helps avoid dead-end files isn’t optional anymore. The mortgage AI boom is creating serious compliance gaps and liability risks that industry educators are flagging as immediate threats. Issues include inaccurate disclosures, data misuse, and bias concerns that could expose originators to regulatory action.

Meanwhile, Harvard research shows a neural network can predict 71% of mutual fund trading decisions, highlighting AI’s growing sophistication in financial markets. But Dalbar’s 2025 report found the average equity investor still earned 8.5% less than the S&P 500 due to human psychology factors like loss aversion and panic selling. The contrast between AI’s analytical precision and human emotional decision-making continues to widen across financial services.

Bond markets showed modest gains today despite low holiday-adjacent volume, with MBS up 6 ticks and the 10-year Treasury down 1 basis point to 4.334%. ISM services data came in mixed, with employment dropping to 45.2 versus 51.8 previously, but prices paid jumping to 70.7 from 63.0. Traders remain focused on Iran conflict developments, particularly after Trump’s ultimatum deadline approaches Tuesday night for reopening shipping channels.

The Strait of Hormuz situation continues to create volatility risks, though some ships have successfully made recent transits. Market participants are waiting to see if defensive momentum might shift once geopolitical tensions ease. Rocket Mortgage edged ahead of UWM in total loan count for 2025, originating 429,332 loans (6.33% market share) compared to UWM’s 422,120 loans (6.25% share).

However, UWM dominated in dollar volume with $164.32 billion versus Rocket’s $116.16 billion, reflecting UWM’s focus on purchase loans with higher balances. Rocket concentrated more heavily on cash-out refinances and second liens, which typically have lower loan amounts. The data may not fully reflect Rocket’s Mr.

Cooper acquisition impact, which closed October 1, 2025, due to HMDA reporting lags. Overall originations rose to 6.8 million from 6.25 million in 2024, with denial rates improving to 22.5% from 24.3%. Opendoor is acquiring Doma’s closing and escrow operations while partnering with Fannie Mae on the Title Acceptance Program, which eliminates lender’s title insurance requirements for about 80% of eligible refinance loans.

The program uses algorithmic risk assessments instead of manual title searches, resulting in faster closings and roughly $1,100 in savings per refinance transaction. Doma’s technology has powered Fannie’s program since 2024, with the new structure having Doma handle title risk decisions while Opendoor manages closing and escrow. This move directly targets the closing process, which Opendoor has identified as the most challenging part of simplifying home transactions.

Locking vs Floating

March’s rate spike has cooled in early April, but volatility risks persist as long as the Iran conflict continues. Current market conditions suggest waiting for potential shifts in defensive momentum that could coincide with the end of hostilities. While recent days have shown improvement, it’s still too early to make confident lock/float decisions based on this trend alone.

Today’s Events

ISM N-Mfg PMI (Mar): 54.0 vs 55 forecast, 56.1 previous

ISM Services Employment (Mar): 45.2 vs 51.8 previous

ISM Services New Orders (Mar): 60.6 vs 58.6 previous

ISM Services Prices (Mar): 70.7 vs 63.0 previous

Bond Pricing

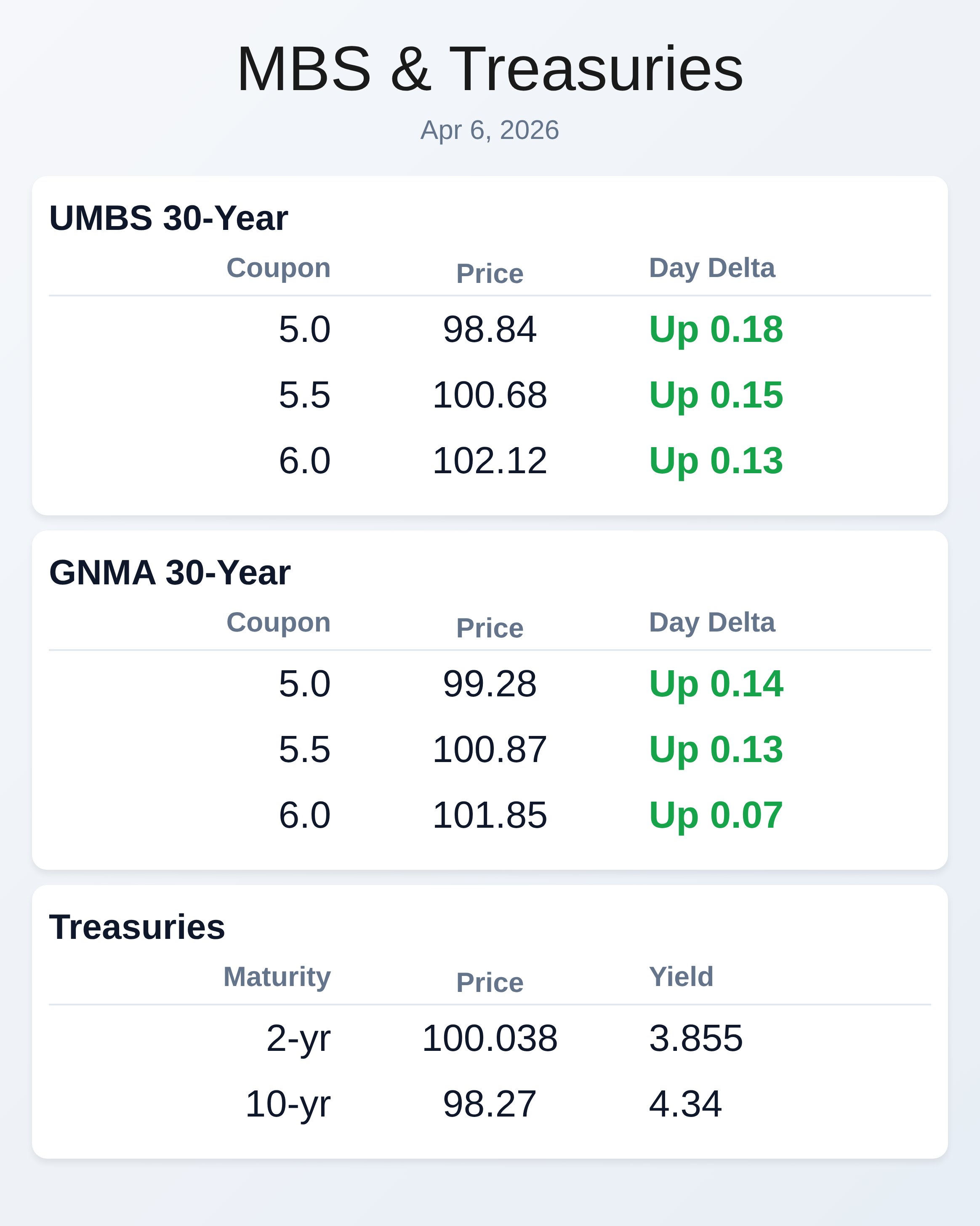

UMBS 30 yr

| Coupon | Price | Intra-Day Change |

| 5.0 | 98.84 | 0.18 |

| 5.5 | 100.68 | 0.15 |

| 6.0 | 102.12 | 0.13 |

GNMA 30 yr

| Coupon | Price | Intra-Day Change |

| 5.0 | 99.28 | 0.14 |

| 5.5 | 100.87 | 0.13 |

| 6.0 | 101.85 | 0.07 |

Treasuries

| Term | Yield | Price | Intra-Day Yield Change |

| 2 yr | 3.855 | 100.038 | 0.03 |

| 3 yr | 3.88 | 98.934 | 0.022 |

| 5 yr | 3.986 | 99.501 | 0.012 |

| 7 yr | 4.167 | 100.502 | -0.031 |

| 10 yr | 4.34 | 98.27 | 0.024 |

| 30 yr | 4.881 | 97.954 | -0.036 |