WTMS Blog Today = What’s up in Mortgage Today (PM) – 04/07/2026

Markets turned volatile Tuesday as geopolitical tensions over Iran’s response deadline created wild swings throughout the trading session. MBS securities fell as much as a quarter point during mid-day weakness, with UMBS 5.0s dropping to session lows near 98.56 before recovering on late-day ceasefire optimism. The 10-year Treasury yield spiked to 4.364% at the weakest levels before settling back to 4.296% as Pakistan floated a potential two-week extension with ceasefire provisions.

Oil prices initially surged on escalation fears but reversed sharply lower when diplomatic options emerged. The mortgage origination landscape shifted dramatically with new HMDA data revealing a split leadership between Rocket Mortgage and United Wholesale Mortgage in 2025. Rocket originated 429,332 loans for a 6.33% market share, edging out UWM’s 422,120 loans and 6.25% share by volume count.

However, UWM dominated in dollar volume with $164.32 billion compared to Rocket’s $116.16 billion, highlighting divergent business strategies. Rocket’s strength in smaller-balance, rate-sensitive transactions contrasts sharply with UWM’s focus on higher-value purchase loans through the broker channel. Economic data painted a mixed picture of business investment and employment trends that could influence Federal Reserve policy decisions.

Core capital expenditures jumped 0.6% in February, beating the 0.4% forecast and suggesting companies are moving forward with investment plans despite geopolitical uncertainty. However, durable goods orders fell 1.4%, largely driven by declining aircraft bookings as Boeing reported fewer February orders. The ADP Employment report showed 26,000 new jobs versus the prior month’s 10,000, though no forecast was available for comparison.

Credit costs continue pressuring mortgage originators as FICO tri-merge reports now cost around $540 per file, forcing lenders to make harder pipeline decisions earlier in the process. VantageScore is positioning its alternative scoring model as a solution for better pre-screening and reduced wasted credit pulls, particularly for first-time homebuyers. Industry veterans question whether lenders can adapt quickly enough to benefit from these tools, especially given the current focus on survival over innovation.

The rising cost structure is forcing originators to choose between processing volume or protecting margins on each transaction. Finance of America faces legal challenges over an alleged March 20 ransomware attack, with a customer lawsuit filed in Texas federal court before any public breach disclosure. The Word Leaks group reportedly claimed responsibility for the cyberattack, potentially exposing Social Security numbers and personal data for thousands of customers.

This follows a broader industry pattern where data breach lawsuits are filed before companies fully understand incident scope, though these cases typically settle rather than reach trial. The company has not reported the incident to state attorney general databases or provided public comment. Iran war dynamics continue driving unusual oil market behavior, with West Texas Intermediate trading at a $5 premium to Brent crude as Gulf shipping constraints boost domestic demand.

This pricing inversion is expected to significantly impact Friday’s inflation data, with March CPI forecasted to jump from 2.4% to 3.4% annualized. Core CPI is projected to rise from 2.5% to 2.7%, potentially complicating Federal Reserve policy discussions around future rate cuts. The geopolitical situation remains fluid, with Wednesday expected to bring either meaningful escalation or de-escalation based on Iran’s response to diplomatic overtures.

Locking vs Floating

Markets remain highly volatile with geopolitical developments around Iran creating significant uncertainty for Wednesday trading. The deadline for Iran’s response to diplomatic terms has passed, with potential outcomes ranging from major escalation to a two-week ceasefire extension. Given the extreme nature of possible market reactions, originators should expect larger than normal moves in either direction and plan accordingly for potential repricing risks.

Today’s Events

ADP Employment Change Weekly: 26K vs — forecast, 10K previous

Core CapEx (February): 0.6% vs 0.4% forecast, 0% previous

Durable goods (February): -1.4% vs -0.5% forecast, 0% previous

Bond Pricing

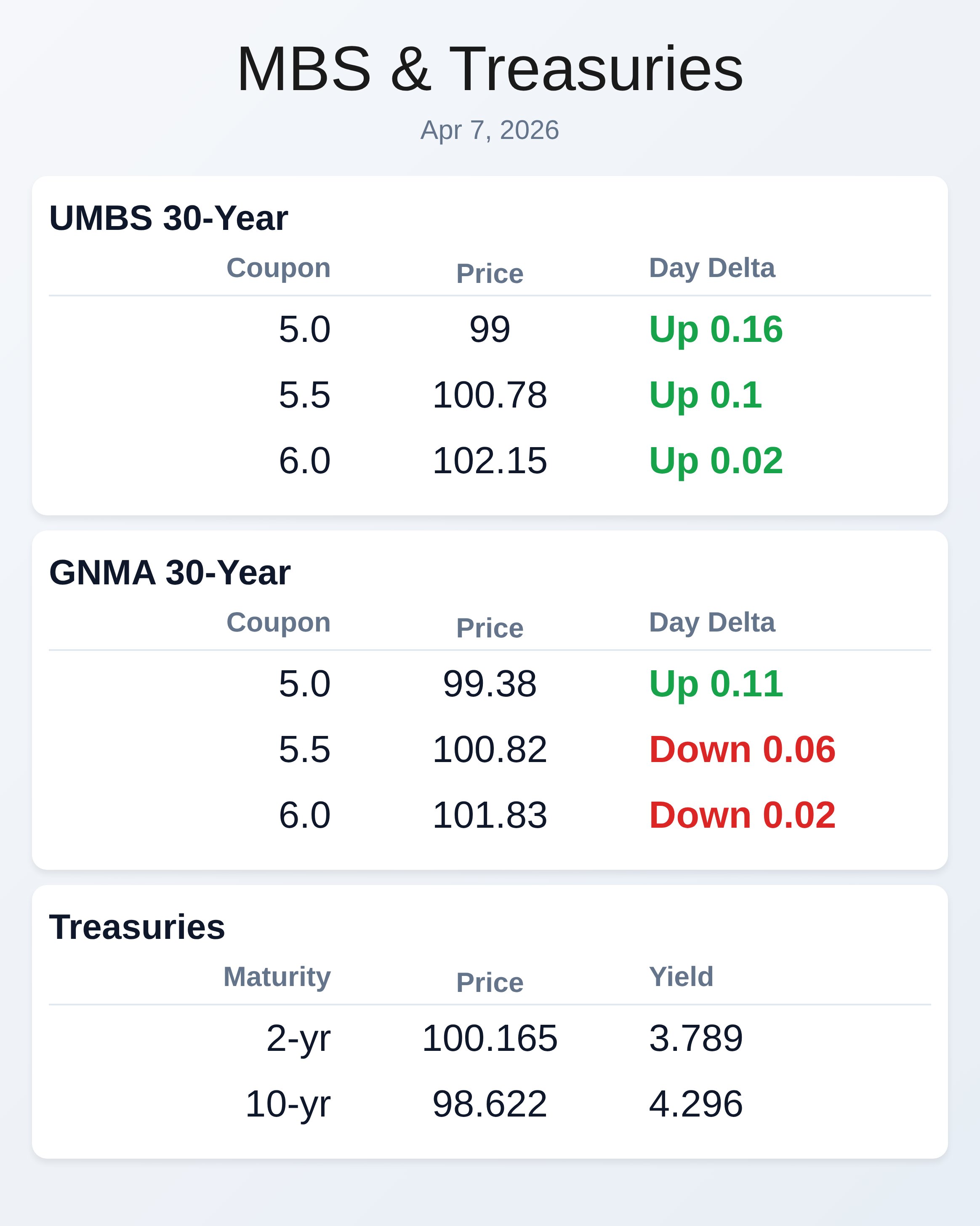

UMBS 30 yr

| Coupon | Price | Intra-Day Change |

| 5.0 | 99 | 0.16 |

| 5.5 | 100.78 | 0.1 |

| 6.0 | 102.15 | 0.02 |

GNMA 30 yr

| Coupon | Price | Intra-Day Change |

| 5.0 | 99.38 | 0.11 |

| 5.5 | 100.82 | -0.06 |

| 6.0 | 101.83 | -0.02 |

Treasuries

| Term | Yield | Price | Intra-Day Yield Change |

| 2 yr | 3.789 | 100.165 | -0.059 |

| 3 yr | 3.849 | 99.021 | -0.024 |

| 5 yr | 3.93 | 99.754 | -0.054 |

| 7 yr | 4.108 | 100.855 | -0.056 |

| 10 yr | 4.296 | 98.622 | -0.039 |

| 30 yr | 4.872 | 98.088 | -0.019 |