**WTMS Blog Today = What’s up in Mortgage Today (PM) – 06/01/2026**

Warren Buffett’s decision to sink $6.8 billion into homebuilder Taylor Morrison signals that one of the world’s sharpest investors sees long-term housing demand recovery even as affordability pressures persist. This is Berkshire Hathaway’s first major acquisition under new CEO Greg Abel, who plans to eventually merge Taylor Morrison with Clayton Homes into a combined platform. Abel’s move breaks from Berkshire’s typical hands-off style, suggesting confidence in housing’s structural appeal beyond near-term headwinds.

With a record $397 billion cash position at quarter-end and homebuilder valuations depressed, timing matters for long-term equity positioning. For mortgage originators, the deal underscores that institutional capital still sees opportunity in housing even when monthly rate chatter dominates headlines. Scotiabank is expanding its U.S.

mortgage warehouse lending footprint by acquiring MapleMark Bank, a Dallas-based commercial bank that brings FDIC deposit insurance credentials. The deal, announced with no disclosed financial terms, builds directly on Scotiabank’s 2024 hire of seven JPMorgan mortgage executives in Texas to launch warehouse finance operations. Recent exits by Flagstar and Comerica from warehouse lending have created openings for new players willing to deploy capital into the segment.

FDIC deposit insurance is critical for attracting mortgage banker clients to warehouse platforms, making this acquisition strategically sound. For lenders shopping warehouse facilities, new competitive entrants may improve pricing and availability. Rocket Mortgage now pulls both FICO and VantageScore 4.0 on every application across Fannie Mae, Freddie Mac, and VA loans as part of an expanded pilot program.

The dual-scoring approach gives borrowers the broadest opportunity to qualify while Rocket evaluates which model—or both—should be retained long-term. This follows FHFA confirmation of roughly $10 million in VantageScore-based loans already delivered to Freddie Mac through early tests, with HUD signaling adoption of both VantageScore 4.0 and FICO 10T for FHA loans later in 2026. Multiple credit score models reduce approval friction and may expand the qualified borrower pool, though operational complexity increases during transition phases.

Originators should monitor which agencies ultimately standardize on scoring methodology. Property tax bills hit a median of $3,119 nationally in 2024, rising 5.1% from the prior year, with borrowers carrying mortgages paying $913 more annually than mortgage-free homeowners through escrow reserves. Every one of the 50 largest U.S.

metros registered increases, led by Tampa (7.7%), Denver (7.4%), and Miami (7.1%), while New York City tops absolute dollar amounts at more than $10,000 median bills. These rising tax obligations flow directly into debt-to-income calculations and monthly payment quotes, potentially pricing marginal borrowers out of qualification. Phoenix homeowners enjoy the lowest effective tax rate at 0.44%, while Buffalo carries the highest at 2%, creating regional variance in home affordability math.

Loan officers should expect property tax increases to compress borrowing power further in high-tax jurisdictions. Technology vendors continue sharpening tools to reduce friction in mortgage origination workflow. ICE launched a fraud detection platform integrated with Encompass to catch underwriting risks earlier, while Finastra deployed an analytics platform to help lenders identify where borrowers abandon applications and benchmark conversion rates against peers.

FICO named Eric Lapin as VP of strategy for its scores business, bringing 25 years of housing finance experience to the role as credit analytics remain central to lending decisions. These incremental process improvements target application fallout and manual review bottlenecks that drag loan timelines. Originators should evaluate whether new vendor tools justify implementation costs against current operational constraints.

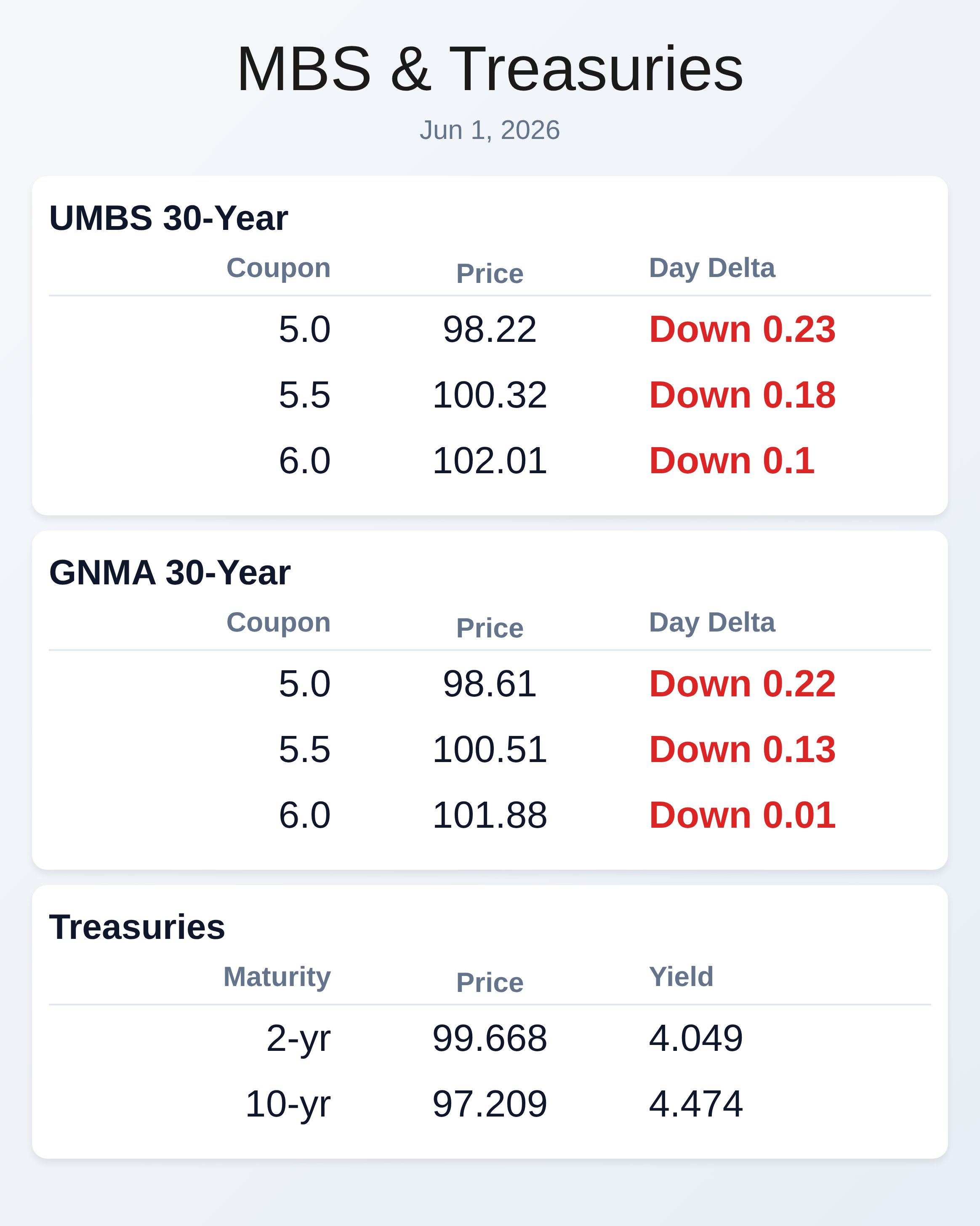

Mortgage rates improved modestly last week as inflation came in cooler than expected, but momentum faces headwinds as June opens with stocks near record highs and May jobs data still pending. Kevin Warsh’s inflation gauge is drawing renewed attention among rate strategists as markets hunt for clues on when the Federal Reserve might adjust its policy stance. Oil price declines supported the rate improvement, though commodity volatility remains a wild card for near-term direction.

Borrowers and lenders alike are watching whether cooling inflation persists or reverses, as that determination shapes both lock-and-float strategy and pipeline pricing. Friday’s employment report will be critical for confirming whether labor market strength can sustain without reigniting price pressures. Subscribe free to WTMS at WellThatMakesSense.com to get daily mortgage market insights in your inbox.