**WTMS Blog Today = What’s up in Mortgage Today (PM) – 06/10/2026**

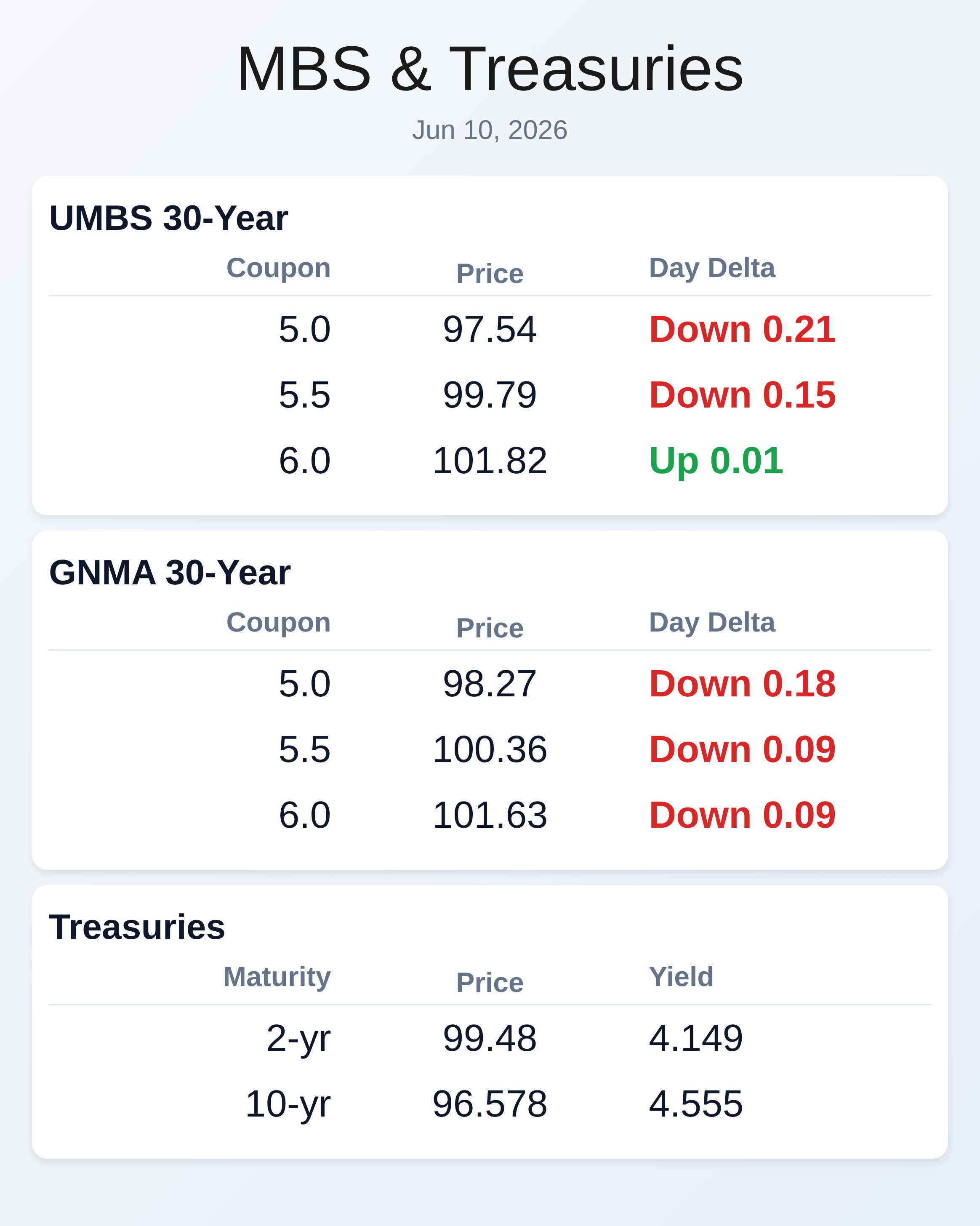

War headlines triggered a volatile reversal in mortgage bonds Wednesday as geopolitical concerns overwhelmed an inflation report that came in softer than feared. MBS fell roughly an eighth of a point from morning highs, with UMBS 5.0 dropping 15 basis points to 97.60, while the 10-year Treasury climbed to 4.554 percent following Trump’s comments about escalating attacks in Iran. Negative reprices became increasingly likely among the most reactive lenders as bond markets sold off on supply-demand imbalances following a Treasury auction.

The core Consumer Price Index came in at 0.2 percent month-over-month—below the 0.3 percent forecast—offering brief relief before geopolitical fears drove yields higher. Oil prices moved alongside rate weakness, signaling genuine risk-off sentiment in capital markets. The afternoon deterioration erased early morning strength despite benign inflation data that should have supported bonds.

Prices bounced sharply from the weakest intraday levels around 2:55 PM, recovering about three basis points from peaks near 4.559 percent on the 10-year. Risk-tolerant loan officers who maintained lock triggers at 4.57 percent remained positioned for upside, while conservative originators still lacked sufficient technical support for more neutral rate strategies. The market’s reaction underscores how quickly geopolitical headlines can override economic fundamentals in the bond space.

MBS pricing remains fragile with traders increasingly defensive about supply dynamics. Originators should brace for potential reprices if markets open weaker Thursday, particularly among lenders who printed rate sheets during this morning’s peaks. The technical ceiling established at 4.80 percent on the 10-year remains far away, but resistance levels at 4.59 and 4.66 percent suggest room for additional weakness.

Most of the afternoon selling was bond-specific rather than driven by new economic catalysts, meaning the catalyst for stabilization remains unclear. Client conversations should emphasize that inflation continues running above Federal Reserve targets, making near-term rate improvement unlikely. Lock activity should remain elevated given the uncertain rate trajectory and geopolitical noise dominating headlines.

The broader question facing the market is whether elevated yields reflect a new equilibrium or prove temporary ahead of next week’s batch of economic data. Tuesday’s core PCE reading and Thursday’s consumer confidence number could reset market expectations depending on whether inflation shows continued progress. Headline CPI at 4.2 percent still exceeds the Fed’s 2 percent objective, justifying mortgage rates in the 6.4 to 6.5 percent range for borrowers.

Supply-demand imbalances in Treasuries may have contributed as much to afternoon weakness as geopolitical concerns, suggesting some volatility could dissipate by Friday. MBS price action through mid-week should clarify whether bonds are building fresh support or heading toward session lows.

**Locking vs Floating**

Risk-tolerant borrowers should maintain lock triggers at 4.57 percent on the 10-year, while risk-averse clients still lack sufficient technical support to justify neutral positioning.

Wednesday’s volatility reinforces that bonds are leveling off after last week’s selling, but the path forward remains uncertain given geopolitical and technical headwinds.

**Today’s Events**

Core CPI (May): 0.2% versus 0.3% forecast, 0.4% prior

Headline CPI (May): 0.5% versus 0.5% forecast, 0.6% prior

Core CPI year-over-year (May): 2.9% versus 2.9% forecast, 2.8% prior

Headline CPI year-over-year (May): 4.2% versus 4.2% forecast, 3.8% prior

**Bond Pricing**

**UMBS 30 yr**

| Coupon | Price | Intra-Day Change |

| 5.0 | 97.60 | -0.15 |

| 5.5 | 99.84 | -0.10 |

| 5.0 | 98.22 | -0.24 |

**GNMA 30 yr**

| Coupon | Price | Intra-Day Change |

**Treasuries**

| Term | Yield | Price | Intra-Day Yield Change |