WTMS Blog Today = What’s up in Mortgage Today (AM) – 11/20/2025

The September jobs report delivered a split decision that kept bond traders on their toes this morning. Nonfarm payrolls came in at 119k versus the 50k expectation, but the unemployment rate ticked up to 4.4% from 4.3%. This mixed data explains why 30-year UMBS 5.0 coupons are holding gains of 21 ticks despite the stronger-than-expected job creation.

Labor force participation also rose to 62.4%, suggesting more Americans are actively seeking work. Fed rate cut odds for December dropped to around 25 percent following yesterday’s FOMC minutes, which showed most officials favoring a pause. The delayed employment data release schedule complicates Fed decision-making, with the November jobs report now pushed back to December 16.

This places the critical employment data after the Fed’s final 2025 meeting, giving policymakers less information to work with. Markets are interpreting this as reducing the likelihood of another rate reduction before year-end. The government shutdown continues to disrupt economic data collection and Treasury auction demand.

Yesterday’s 20-year Treasury bond sale drew weak investor interest, but markets barely reacted to the poor demand. Today brings a $19 billion reopened 10-year TIPS auction and Treasury buybacks of 20- to 30-year bonds due to liquidity concerns. Class D 48-hour MBS notifications are also in effect today.

Corporate layoffs accelerated in October with 153,074 job cuts announced, marking the worst October in 22 years according to Kobeissi’s Letter. For the first 10 months of 2025, U.S. employers announced 1.1 million job cuts, the second-highest total since 2009.

While AI automation accounts for only 4% of these cuts, unfavorable market conditions drove 21% of the layoffs, highlighting the broader economic pressures facing businesses.

Locking vs Floating

Today’s employment data created elevated risk and reward scenarios for rate locks. While the 119k job gain versus 50k forecast normally would pressure bonds, the unemployment rate increase to 4.4% is providing some offset.

MBS prices gained 2 ticks and 10-year yields dropped 1.7 basis points by mid-morning trading. Bonds were under pressure Wednesday, so Thursday morning rate sheets may reflect that earlier weakness if overnight conditions remain unchanged. Risk management favors caution given the mixed employment signals and ongoing data delays from the government shutdown.

The November employment report delay until December 16 creates uncertainty about Fed policy direction. Lenders should consider current intraday MBS gains as potentially temporary, especially with five Fed speakers scheduled to make remarks today.

Today’s Events

– September Nonfarm Payrolls: 119K vs 50K forecast

– September Unemployment Rate: 4.4% vs 4.3% forecast

– September Labor Force Participation Rate: 62.4% vs 62.3% previous

– November Philadelphia Fed Business Index: -1.7 vs -3.1 forecast

– November Philadelphia Fed Prices Paid: 56.10 vs 49.20 previous

– Weekly Jobless Claims: 220K initial, 1.974 million continuing

– October Existing Home Sales

– November Kansas City Fed Manufacturing Index

– $19 billion 10-year TIPS auction reopening

– Treasury buyback operation: $2 billion in 20-30 year coupons

– Freddie Mac Primary Mortgage Market Survey

– Five Federal Reserve officials speaking

Bond Pricing

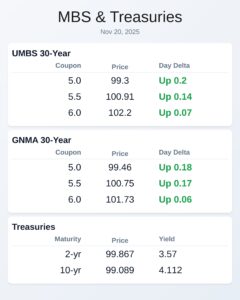

UMBS 30 yr

| Coupon | Price | Intra-Day Change |

| 5.0 | 99.3 | 0.2 |

| 5.5 | 100.91 | 0.14 |

| 6.0 | 102.2 | 0.07 |

GNMA 30 yr

| Coupon | Price | Intra-Day Change |

| 5.0 | 99.46 | 0.18 |

| 5.5 | 100.75 | 0.17 |

| 6.0 | 101.73 | 0.06 |

Treasuries

| Term | Yield | Price | Intra-Day Yield Change |

| 2 yr | 3.57 | 99.867 | -0.026 |

| 3 yr | 3.563 | 99.822 | -0.025 |

| 5 yr | 3.683 | 99.739 | -0.028 |

| 7 yr | 3.874 | 99.247 | -0.028 |

| 10 yr | 4.112 | 99.089 | -0.027 |

| 30 yr | 4.735 | 98.243 | -0.02 |