WTMS Blog Today = What’s up in Mortgage Today (AM) – 05/05/2026

Bond markets are getting hammered on the heels of escalation headlines that have spooked investors globally. The 10-year Treasury jumped to 4.42%, exceeding the key technical ceiling of 4.37% that traders have been watching closely. Until a sweeping peace agreement materializes, mortgage professionals should adopt a defensive strategy and closely monitor intraday MBS price movements.

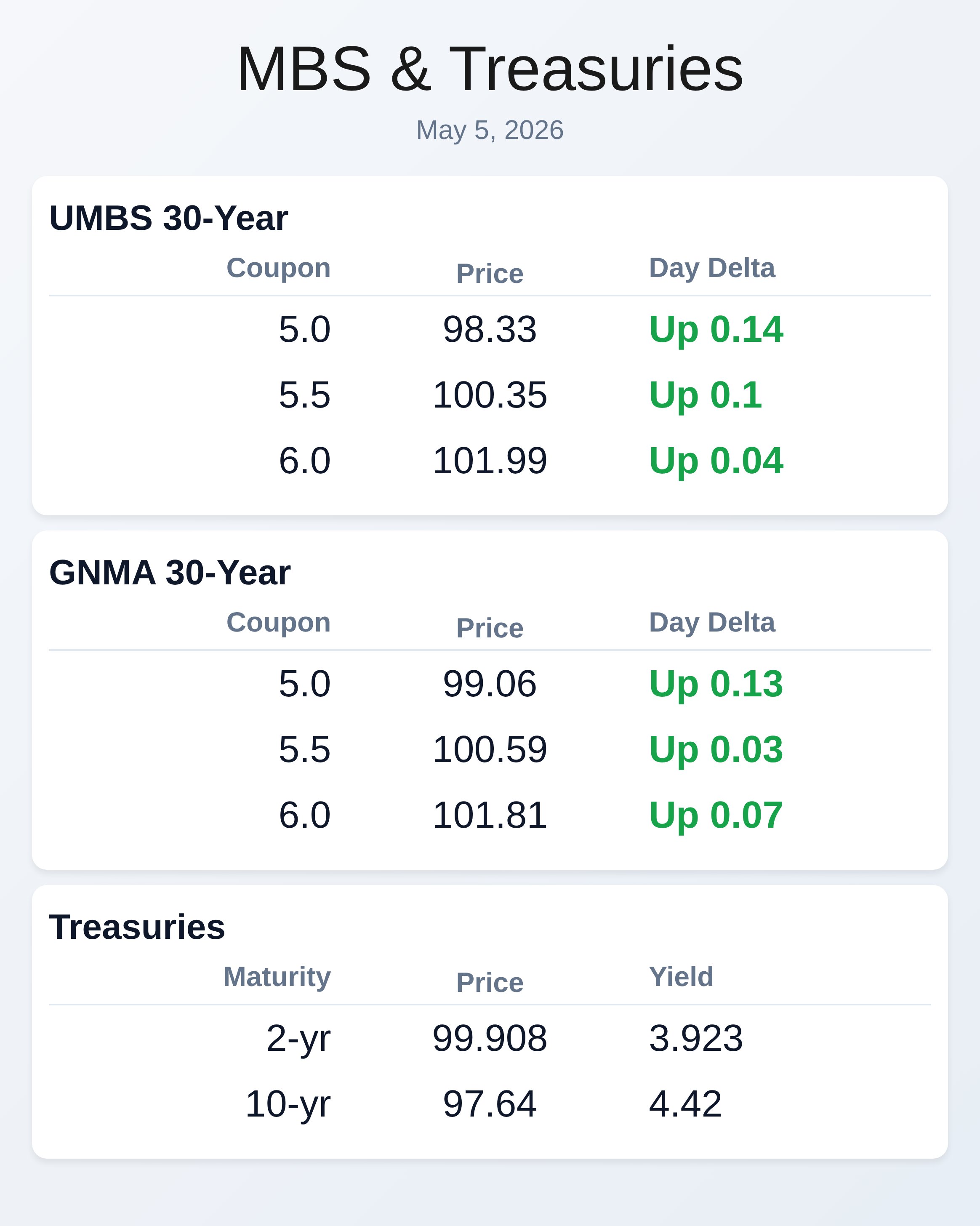

UMBS 5.0 coupons gained 14 basis points while GNMA 5.0s stayed relatively stable at plus 13 basis points. Across the curve, Treasury yields have risen sharply with 2-year yields moving to 3.923%. Manufacturing data delivered mixed signals for the economy this morning, with employment weaker than expected while pricing pressures accelerated significantly.

ISM Manufacturing Employment posted 46.4 against a forecast of 49.0, signaling softening job demand in the industrial sector. However, ISM Prices Paid surged to 84.6, well above the consensus forecast of 80.0, indicating mounting inflationary pressures. The ISM Manufacturing PMI came in at 52.7, matching the prior month and meeting consensus expectations.

This divergence between weak employment and strong pricing suggests stagflationary headwinds that could pressure mortgage prices further. MBS prices showed modest intraday gains despite the broader Treasury market weakness, with UMBS and GNMA coupons trading slightly higher. The 5.5 coupon across both UMBS and GNMA remained relatively flat to slightly positive on the session.

Longer coupons in the 6.0 range posted minimal gains, suggesting market participants are cautious ahead of potential additional geopolitical developments. Duration risk remains elevated, and basis risks between MBS and Treasury futures continue to widen. Mortgage originators should monitor these spreads carefully as they directly impact secondary marketing profitability.

The yield curve remains inverted at the front end, with 2-year Treasuries yielding 3.923% and the 10-year at 4.42%. This inversion reflects recession fears and flight-to-quality dynamics that tend to pressure mortgage origination volumes. The 30-year Treasury is trading at 5.007%, providing a ceiling for conventional conforming rates.

Hedging costs for pipeline management have become more volatile given the geopolitical uncertainty. Lenders should reassess their rate lock strategies and consider tightening product pricing.

**Locking vs Floating**

Manufacturing employment fell significantly short of expectations, providing some technical justification for a more defensive stance among originators.

However, surging prices paid data suggests the Federal Reserve will remain vigilant about inflation control, limiting the potential for significant rate declines. Given yields have breached above the 4.37% technical level to 4.42%, mortgage professionals should favor longer-duration locks over floating positions. Until geopolitical tensions subside and a peace framework emerges, the risk-reward profile favors protecting against further yield expansion.

Originators carrying short duration exposure face heightened mark-to-market losses if yields continue climbing.

**Today’s Events**

ISM Manufacturing Employment (Apr): 46.4 vs 49 forecast, 48.7 previous

ISM Manufacturing PMI (Apr): 52.7 vs 53 forecast, 52.7 previous

ISM Manufacturing Prices Paid (Apr): 84.6 vs 80 forecast, 78.3 previous

**Bond Pricing**

**UMBS 30 yr**

| Coupon | Price | Intra-Day Change |

| 5.0 | 98.33 | 0.14 |

| 5.5 | 100.35 | 0.10 |

| 6.0 | 101.99 | 0.04 |

**GNMA 30 yr**

| Coupon | Price | Intra-Day Change |

| 5.0 | 99.06 | 0.13 |

| 5.5 | 100.59 | 0.03 |

| 6.0 | 101.81 | 0.07 |

**Treasuries**

| Term | Yield | Price | Intra-Day Yield Change |

| 2 yr | 3.923 | 99.908 | -0.031 |

| 3 yr | 3.948 | 98.744 | -0.031 |

| 5 yr | 4.060 | 99.172 | -0.025 |

| 7 yr | 4.240 | 100.062 | -0.013 |

| 10 yr | 4.420 | 97.640 | -0.018 |

| 30 yr | 5.007 | 96.033 | -0.008 |