**WTMS Blog Today = What’s up in Mortgage Today (AM) – 05/21/2026**

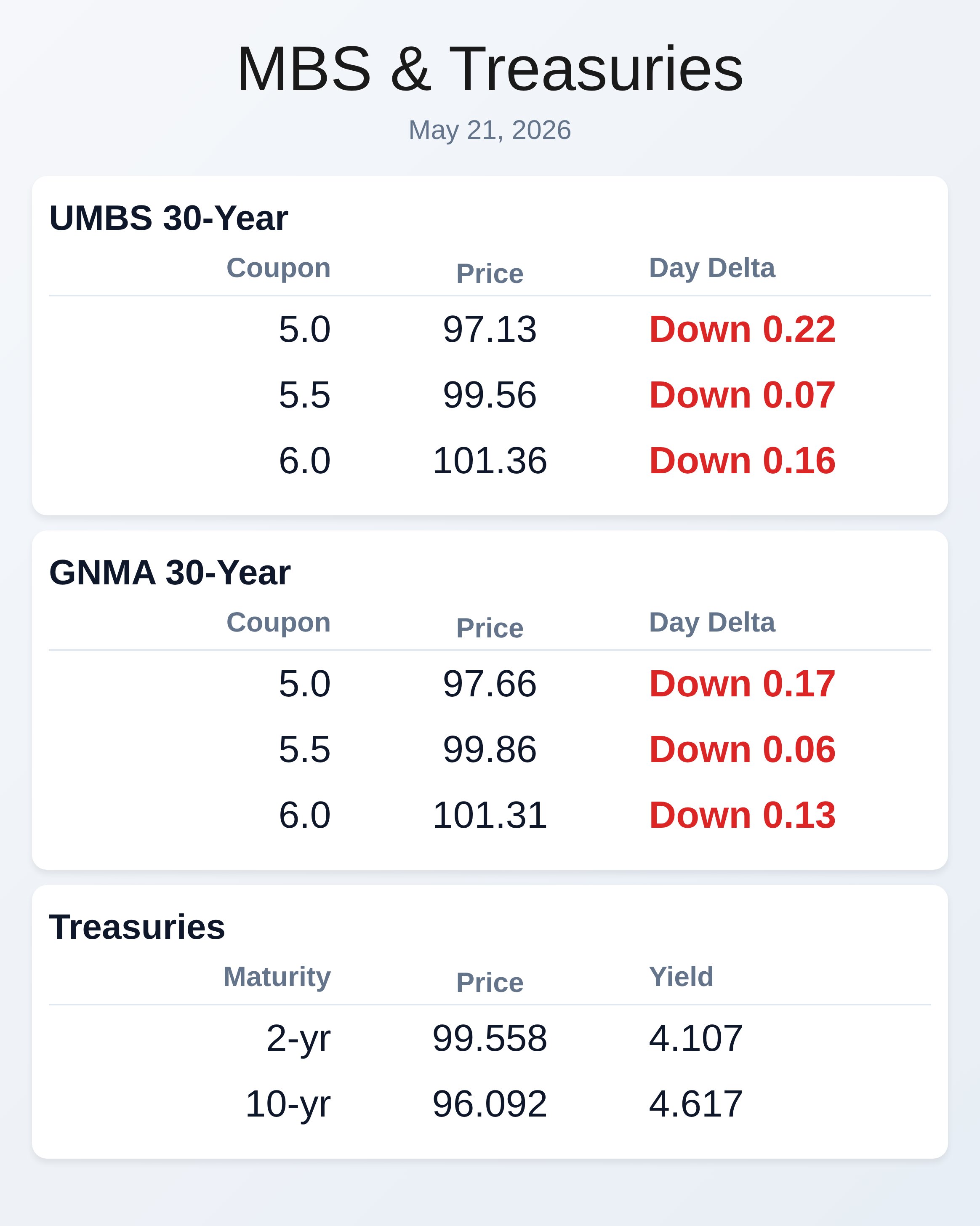

Bond markets reversed sharply today, with geopolitical headlines driving the war news cycle and creating significant intraday volatility. UMBS prices declined across all coupon points, with the 5.0 coupon dropping 0.22 points and the 6.0 coupon falling 0.16 points. GNMA securities tracked similar losses, confirming broad weakness across government-backed MBS products.

The 10-year Treasury yield climbed 3.2 basis points to 4.617%, signaling an uptick in longer-duration rate pressure. Mortgage originators should note that this reversal underscores the fragility of recent bond gains and highlights geopolitical risk as an active pricing factor. The spread between UMBS and GNMA remained relatively consistent, suggesting that agency MBS valuations held their relative positioning despite the broader price decline.

Most coupons traded within narrow ranges, with the 5.5 coupon showing the smallest intraday move on both UMBS and GNMA products. This compressed volatility on intermediate coupons typically signals consolidation ahead of larger directional moves. Lock-in activity may slow as originators wait for clarity on the geopolitical situation.

The reduced movement in mid-coupon securities offers a narrow window for portfolio rebalancing without major price slippage. Treasury yields moved across the entire curve today, with shorter maturities showing larger percentage swings than longer bonds. The 2-year yield gained 5 basis points while the 30-year added only 2.1 basis points, creating a flattening dynamic that reduces hedge efficiency for floating-rate portfolios.

This curve behavior is typical when risk-off sentiment drives near-term cash market pressure rather than long-term structural rate changes. Mortgage servicers tracking duration exposure should monitor this curve flattening closely. The disparity in yield moves suggests traders are pricing near-term uncertainty while remaining cautious on decade-long rate paths.

Peace deal confirmation would almost certainly spark a multi-point rally across MBS and Treasury markets based on current market sentiment and historical precedent. The bond market has priced significant risk premium into current yields due to ongoing geopolitical tension and headline uncertainty. Any reduction in conflict risks would remove that premium, creating immediate upside for both coupon-sensitive and non-coupon-sensitive MBS positions.

However, the path between now and such an outcome remains highly uncertain with multiple potential downside catalysts. Originators relying on rate stability for pipeline management should maintain elevated risk discipline until geopolitical clarity improves. 10-year Treasury ceiling and floor levels help originators track larger market momentum shifts independent of daily MBS price noise.

These benchmark support and resistance levels provide objective reference points when intraday volatility obscures true directional intent. As MBS markets correlate tightly to both Treasury yields and war headline cycles, watching the 10-year yield guides positioning for larger moves. Today’s break above previous intraday resistance suggests bears are gaining near-term control of market direction.

Using these key levels helps filter out noise and identify genuine trend reversals. Mortgage sellers facing margin compression from intraday losses should consider tightening execution discipline on new lock commitments through close. The volatility index remains elevated, and additional negative data or geopolitical headlines could extend losses before day’s end.

Hedging strategies should account for the possibility of another 3-5 basis point move on the 10-year before tomorrow’s opening. Maintaining adequate buffer on rate locks protects margin but reduces volume capture in a nervous market. The next 24 hours will likely determine whether today’s sell-off represents healthy consolidation or the start of a larger correction cycle.

**Locking vs Floating**

Bond market strength and geopolitical headlines remain tightly correlated, with any confirmed peace developments almost certainly creating additional rate rally opportunity. Floaters benefit from the heightened uncertainty—each positive headline removes risk premium and creates immediate downstream pricing gains. Lockers absorb intraday pressure but protect against further deterioration if conflict tensions escalate.

The high degree of uncertainty about future rate paths argues for balanced lock-float strategies that don’t overcommit to either direction. Monitor the 10-year Treasury ceiling and floor levels to track genuine momentum shifts beyond daily noise.

**Bond Pricing**

**UMBS 30 yr**

| Coupon | Price | Intra-Day Change |

**GNMA 30 yr**

| Coupon | Price | Intra-Day Change |

**Treasuries**

| Term | Yield | Price | Intra-Day Yield Change |