WTMS Blog Today = What’s up in Mortgage Today (PM) – 04/14/2026

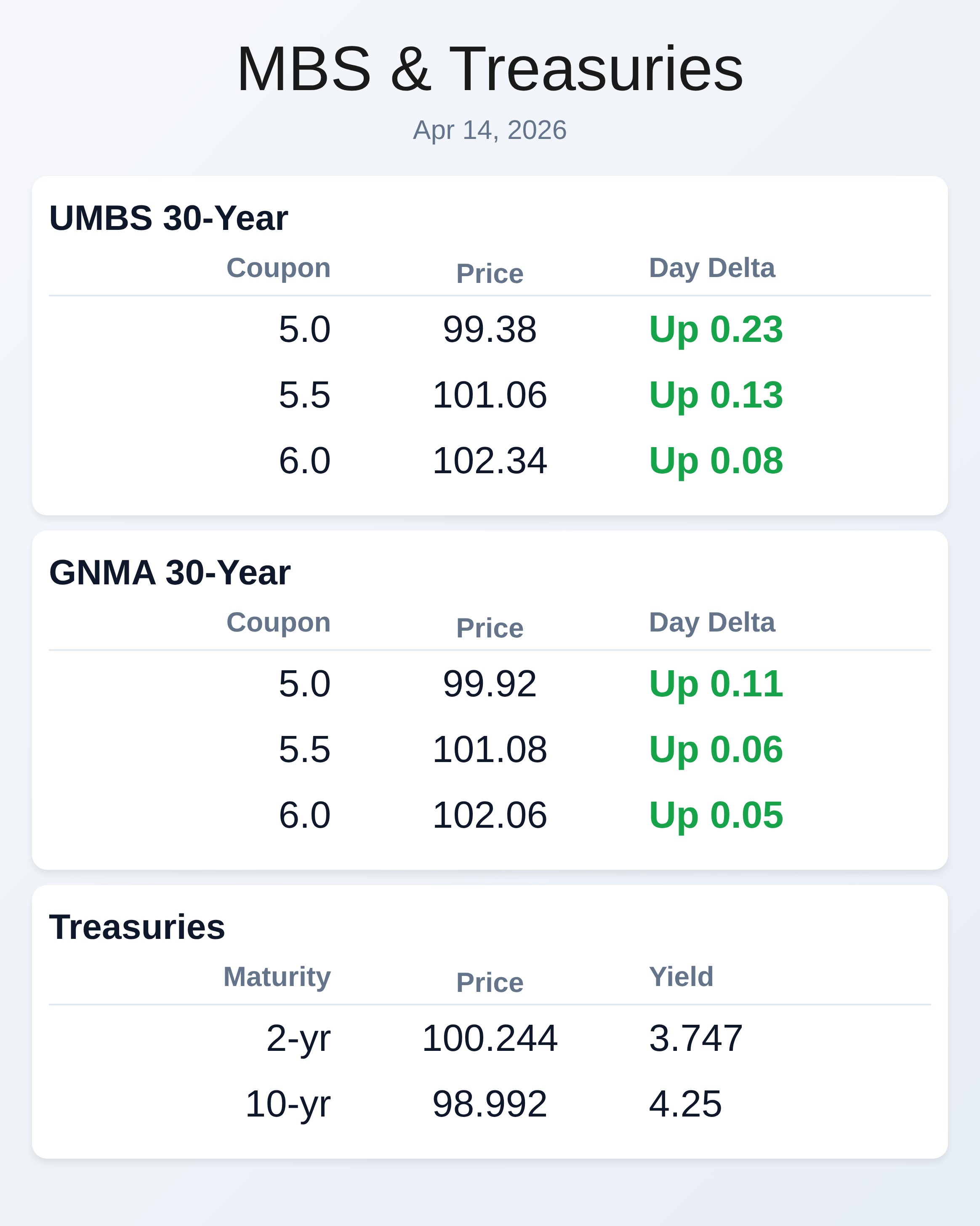

Bonds are staging their best day in four weeks on the back of war-related optimism and PPI inflation data that dramatically undershot expectations. UMBS 5.0 gained nearly a quarter point today, climbing to 99.39, while the 10-year Treasury yield dropped 4.1 basis points to settle at 4.247 percent. A Fox News report this morning quoting a Trump administration official saying “we have all the ingredients of a deal” with Iran sent oil prices lower and sparked both bond and equity rallies.

The market’s reaction was swift and decisive, with investors rotating into safer assets as geopolitical risk sentiment eased. This momentum marks only the second consecutive day of gains since the start of the war, making lock-worthy pricing available for the first time in roughly a month. March’s existing home sales data paints a mixed picture as the spring selling season limps into its opening month.

The National Association of Realtors reported a 3.6 percent decline in sales compared to February, though year-over-year comparisons improved from a 1 percent drop. Chief Economist Lawrence Yun attributed weakness to lower consumer confidence and softer job growth, signaling that demand pressures remain uneven across the nation. Median home prices hit a record for March at $408,800, continuing the ceiling effect on affordability despite gradually improving conditions.

Days on market compression—falling from 47 to 41 days—reveals a bifurcated market where COVID-era hot spots have cooled while Northeast and Midwest metros see renewed buyer interest. The good news for borrowers: wage growth is outpacing home price appreciation while mortgage rates hold steady, creating measurable improvement in affordability metrics that will matter for Q2 loan production. Originators should note that regional dispersion in housing demand remains pronounced, which means marketing and pipeline strategies need geographic precision.

Builders and real estate agents in declining metros may face margin pressure, but mortgage professionals in appreciating regions could see pipeline growth. The combination of better affordability and regional tailwinds in specific markets creates differentiated origination opportunities depending on your geographic footprint. Lock your best-qualified borrowers early; refinance volume remains depressed and purchase pipelines will vary by state.

Core PPI inflation came in far cooler than forecast, with the month-over-month reading at 0.1 percent versus a 0.5 percent expectation and a 3.8 percent year-over-year gain versus 4.1 percent expected. Headline PPI also underperformed forecasts significantly, with month-over-month at 0.5 percent (expected 1.1 percent) and year-over-year at 4.0 percent (expected 4.6 percent). Surprisingly, despite these massive inflation beats, bond markets did not react immediately at the 8:32 a.m.

data release, with UMBS unchanged and the 10-year up only a handful of basis points. The lack of initial response suggests market participants were already positioned for softer inflation and were focused on Iran developments instead. By late afternoon, however, bond strength had reached its peak as the geopolitical thaw fully priced in.

The 10-year Treasury now trades at critical technical levels that origination teams should monitor for lock-trigger planning. Current yield of 4.247 percent sits just below the 4.28 percent resistance level, with the next ceiling at 4.40 percent and a critical resistance zone at 4.59 percent. Conversely, the 4.05 percent floor provides downside support if geopolitical tensions resurface or economic data disappoints.

GNMA 5.0 coupons are at 99.94 with a 0.13 gain, slightly outperforming UMBS on the day and reflecting continued confidence in government-backed securities. For mortgage sellers managing fallout or repricing clients, today’s four-week price highs offer a window to lock quality borrowers before the geopolitical landscape shifts again. Mortgage teams should treat today’s bond strength as a tactical opportunity rather than a trend reversal given the fragility of the Iran ceasefire narrative.

Two-day winning streaks have been the maximum since the war began, meaning mean reversion is statistically likely within the week. Clients locked at Friday’s worse pricing now face painful repricing scenarios if today’s levels hold, but sellers should resist panic-selling at best-of-month levels. Watch for any negative headlines on Iran negotiations to trigger a quick snapback toward 4.40 percent yields; the buffer is thinner than it appears.

Subscribe to WellThatMakesSense.com for free daily mortgage market updates and lock/float guidance.

Locking vs Floating

The bond market has delivered the best pricing in four weeks after two consecutive days of moderate gains. However, this represents only the second consecutive winning day since the conflict began, suggesting reversal risk remains elevated.

Borrowers on a fence about locking versus floating should recognize this as a genuine opportunity to lock, especially at these levels, but should not assume this momentum extends beyond a few more days. The geopolitical situation remains fluid, and any setback in Iran negotiations could quickly erase these gains.

Today’s Events

Core PPI m/m (Mar): 0.1% vs 0.5% forecast, 0.5% previous

Core PPI y/y (Mar): 3.8% vs 4.1% forecast, 3.9% previous

PPI m/m (Mar): 0.5% vs 1.1% forecast, 0.7% previous

PPI y/y (Mar): 4.0% vs 4.6% forecast, 3.4% previous

Bond Pricing

UMBS 30 yr

| Coupon | Price | Intra-Day Change |

GNMA 30 yr

| Coupon | Price | Intra-Day Change |

Treasuries

| Term | Yield | Price | Intra-Day Yield Change |