WTMS Blog Today = What’s up in Mortgage Today (AM) – 04/14/2026

Bonds ignore a massive beat in inflation data, as diplomatic hopes in Iran negotiations keep risk sentiment alive and energy costs anchored. The 10-year Treasury is holding around 4.29%, barely moved despite PPI coming in significantly cooler than economists expected. March producer prices rose just 0.5% month-over-month versus forecasts of 1.1%, while core PPI advanced only 0.1% versus the expected 0.4%, signaling that underlying wholesale inflation is cooling despite war-related oil volatility.

Markets are effectively in a holding pattern, with futures pricing in no change to Fed policy through year-end. This muted reaction tells you everything: traders are more focused on geopolitics and oil than hard data. The lack of volatility has been a gift to mortgage investors, as embedded optionality outperforms when rates stay range-bound.

Agency MBS have added another 6 basis points of excess return in recent weeks and fully erased losses from the onset of Middle East tensions, a remarkable recovery aided by declining rate volatility and steady Treasury demand. Current coupon spreads remain compressed but within familiar ranges, leaving investors focused on carry and liquidity rather than directional bets. Higher coupon, lower pay-up specified pools continue to offer relative value compared to investment-grade corporates.

For mortgage originators, this stability means lock-in opportunities without sharp repricing risk. Existing home sales fell 3.6% month-over-month in March to 3.98 million units, pressured by elevated mortgage rates, higher prices, limited inventory, and softer job growth at the start of spring buying season. The NFIB optimism index dropped to 95.8 in March, marking its lowest reading in a year and well below expectations.

These demand headwinds align with the broader constraint on origination volume, though diplomacy signals from Iran talks are helping equity markets rally and reduce fear of further rate spikes. The combination of cooler inflation, slowing sales, and recession concerns creates a three-way tug on long-term rates that keeps Treasury yields anchored. Energy prices remain the wildcard—if oil stabilizes near current levels, inflation stays manageable.

Policy dynamics continue to reshape mortgage spreads more than benchmark rates, according to capital markets analysis. Policy signals around MBS interventions, institutional ownership debates, and credit regulation are exerting subtle but powerful effects on execution and hedging strategies across the industry. The $1.8 trillion annual budget deficit remains a background headwind for rates, though its immediate impact is overshadowed by geopolitical headlines.

Understanding these policy nuances helps originators distinguish between noise and signal, avoiding costly overreactions to headlines without structural market consequences. Treasury valuations remain fairly attractive relative to corporates, with short-duration exposure in high demand as investors prioritize capital preservation. The 15-year MBS sector is now screening as the cheapest on an OAS basis, presenting an opportunity for investors hunting relative value.

Lower-coupon pools benefit from carry, while higher-coupon paper offers some relief from further curve steepening. Agency MBS continue to look fairly valued, not stretched, which supports a steady-handed approach rather than aggressive positioning in an uncertain environment. Investors should watch for any narrowing in spreads as oil prices moderate further.

Risk management frameworks favor disciplined positioning until macro clarity emerges on growth, inflation, and Fed policy post-Powell transition. Markets are pricing no Fed rate changes through year-end, despite inflation surprises cutting both ways—cooler core readings suggest no urgency to hike, yet elevated energy and geopolitical risks keep terminal rate expectations elevated. For originators, this means the 4.25%–4.35% zone in 10-year yields remains a logical reference range until diplomatic developments firm up or dissipate entirely.

Lock triggers at 4.34% or 4.40% work for risk-takers, while conservative shops should maintain defenses until yields decisively break below 4.30%.

Locking vs Floating

Market momentum in the 10-year remains flat compared to March, creating more room for different lock and float strategies. Risk-takers have a reasonable case for setting lock triggers at 4.34% to 4.40% in yield terms, capturing any upside surprise if geopolitics escalate further.

The risk-averse camp sees no compelling reason to lower defenses until Treasury yields convincingly break below 4.30% and hold there. The key insight: yield ceilings and floors matter more than intraday MBS moves when tracking bigger-picture bond market direction.

Today’s Events

Core PPI m/m (Mar): 0.1% vs 0.5% forecast, 0.5% previous

Core PPI y/y (Mar): 3.8% vs 4.1% forecast, 3.9% previous

PPI m/m (Mar): 0.5% vs 1.1% forecast, 0.7% previous

PPI y/y (Mar): 4.0% vs 4.6% forecast, 3.4% previous

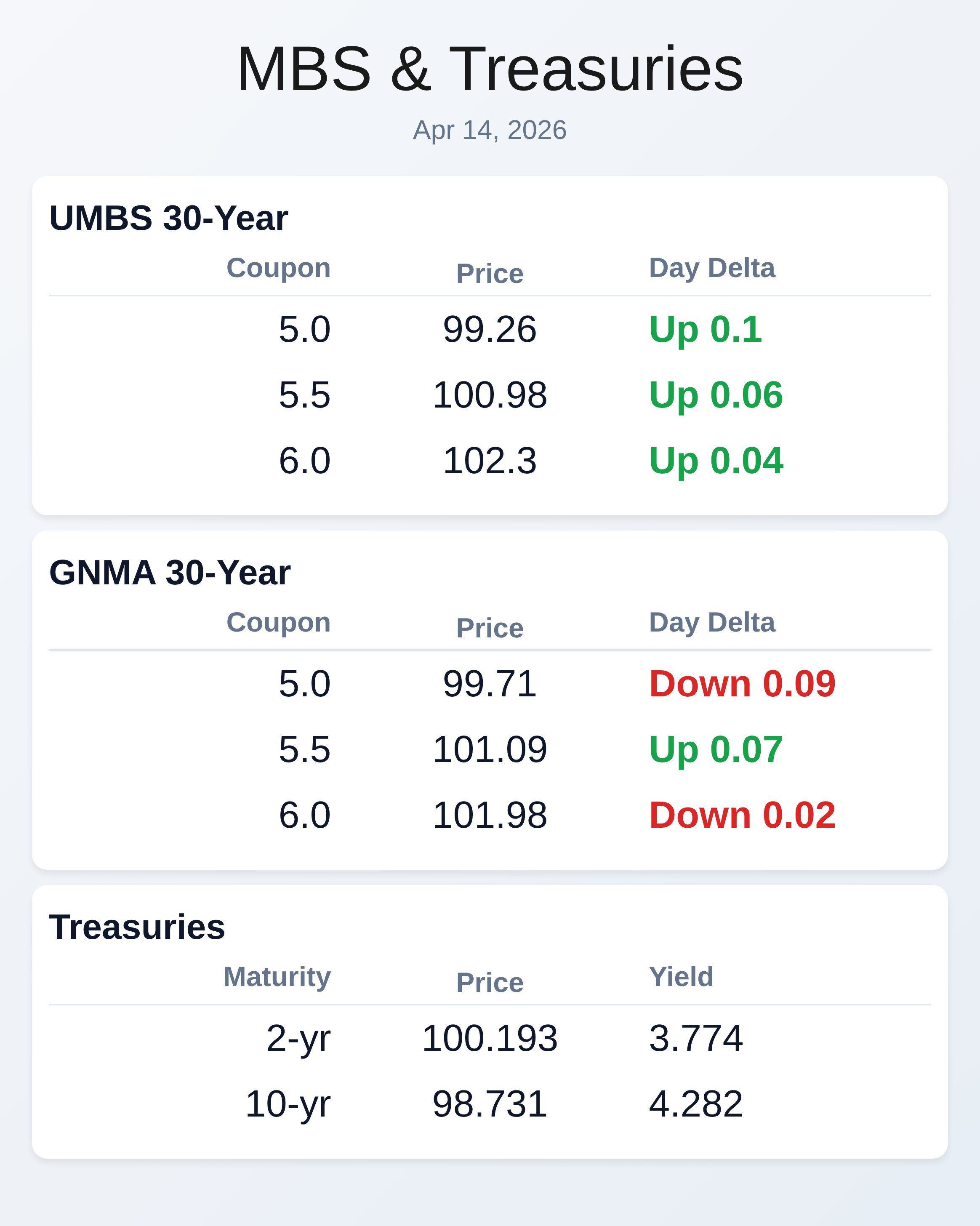

Bond Pricing

UMBS 30 yr

| Coupon | Price | Intra-Day Change |

|5.0|99.26|0.10|

|5.5|100.98|0.06|

|6.0|102.30|0.04|

GNMA 30 yr

| Coupon | Price | Intra-Day Change |

|5.0|99.71|-0.09|

|5.5|101.09|0.07|

|6.0|101.98|-0.02|

Treasuries

| Term | Yield | Price | Intra-Day Yield Change |

|2 yr|3.774|100.193|0.000|

|3 yr|3.789|99.188|-0.003|

|5 yr|3.902|99.878|-0.011|

|7 yr|4.084|101.003|-0.010|

|10 yr|4.282|98.731|-0.006|

|30 yr|4.887|97.852|-0.009|