WTMS Blog Today = What’s up in Mortgage Today (PM) – 05/05/2026

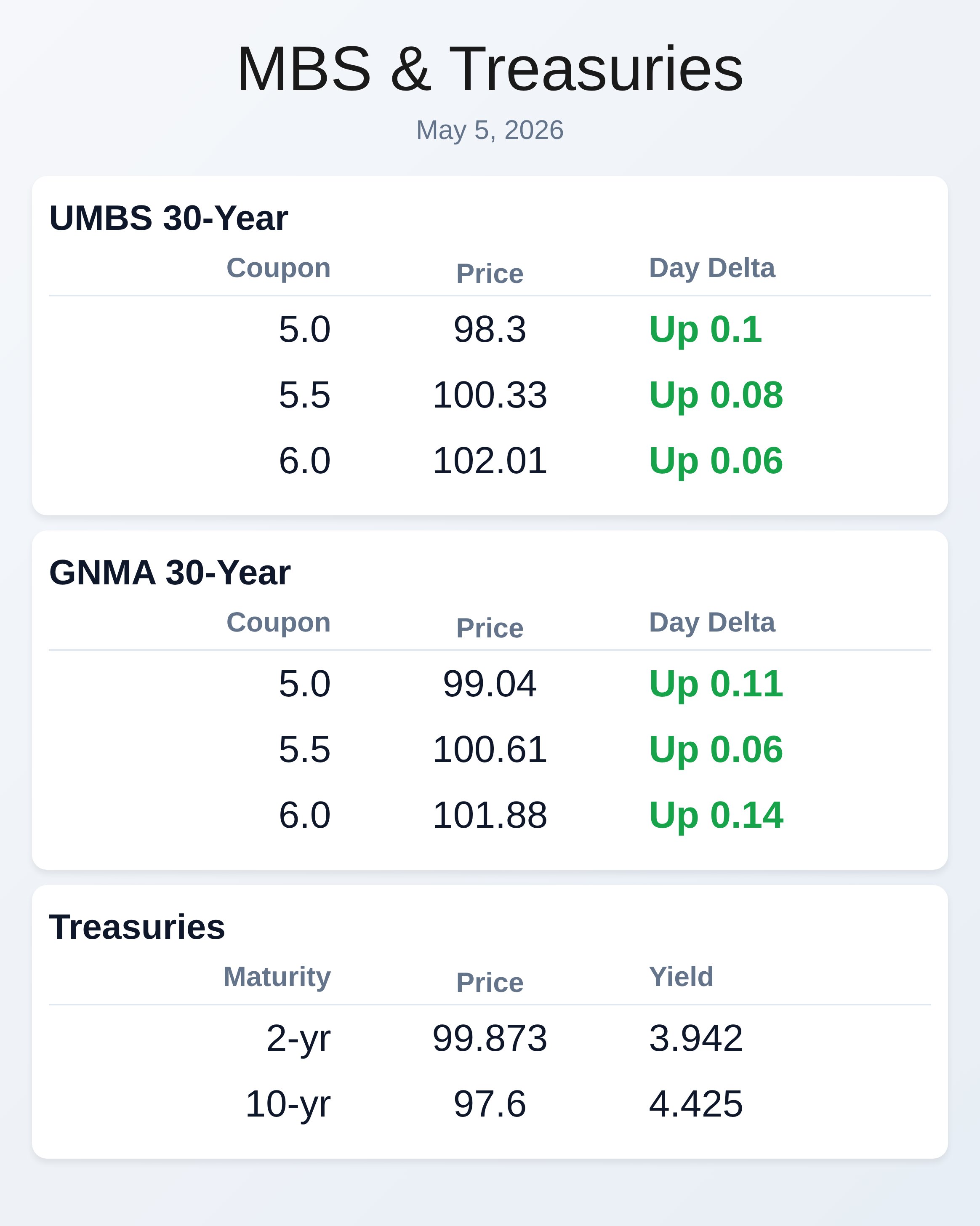

Bonds staged a modest recovery today as oil prices stabilized and economic data came in near expectations, but mortgage-backed securities gained less than one-third of yesterday’s losses, signaling caution among traders. UMBS 5.0 coupons climbed just 0.14 points, while the 10-year Treasury yield fell only 1.9 basis points to 4.419%, leaving rates vulnerable to renewed selling pressure. The market’s tepid response despite favorable data suggests investors are braced for continued volatility, especially with Middle East tensions keeping commodity markets elevated.

New home sales surprised to the upside at 682,000 units versus a 650,000 forecast, the strongest signal from today’s economic print that housing demand remains intact even at current rate levels. ISM services employment jumped to 48.0 from 45.2, and business activity held steady at 55.9, both reflecting a labor market that shows life despite recent Fed warnings about rate hikes. The trade deficit narrowed to -60.30 billion versus expectations of -60.9 billion, a small win for the administration’s trade policy narrative.

These benign prints should have helped bonds more, but they didn’t, underscoring the reality that rates are now driven more by inflation fears and Fed policy than traditional economic calendars. The bigger story is what’s brewing at the Federal Reserve: Neel Kashkari’s recent commentary on potential rate hikes has sent Fed Funds futures markets scrambling, with December contract pricing now showing a nearly 30% chance of tightening and only a 6% chance of a cut this year. That shift from accommodative expectations to hawkish repricing happened fast and explains why bond traders are gun-shy despite solid economic momentum.

For mortgage originators, this signals that rate locks should be treated as a precious commodity because the window to offer certainty to borrowers is narrowing. The UWM-Two Harbors deal fight continues to escalate in public, with both companies now making their case directly to shareholders as the May 19 vote approaches. UWM is defending its $12 bid by attacking the board’s math and process, positioning its offer as offering more value and flexibility, while Two Harbors leans on execution certainty.

This fight moving into public shareholder warfare means the outcome is increasingly unpredictable, and industry consolidation—which affects secondary market pricing—now hinges on voter sentiment rather than boardroom negotiation.

**Locking vs Floating**

Bonds recovered modestly but trails yesterday’s selloff by a wide margin, creating asymmetric risk in favor of locking rates. For borrowers with rate certainty in hand, this is a stabilization window to move loans to underwriting before the next leg of volatility hits.

Those still shopping should lock now given the Fed’s emerging hawkish tilt—improvement is possible but far from guaranteed, and the tail risks are clearly pointed higher.

**Today’s Events**

Trade Gap (Mar): -60.30B vs -60.9B forecast, -57.3B previous

S&P Global Services PMI (Apr): 51.0 vs 51.3 forecast, 49.8 previous

ISM Business Activity (Apr): 55.9 vs forecast unavailable, 53.9 previous

ISM Non-Manufacturing PMI (Apr): 53.6 vs 53.7 forecast, 54.0 previous

ISM Services Employment (Apr): 48.0 vs forecast unavailable, 45.2 previous

ISM Services New Orders (Apr): 53.5 vs forecast unavailable, 60.6 previous

ISM Services Prices (Apr): 70.7 vs 70.7 forecast, 70.7 previous

New Home Sales (Mar): 682K vs 650K forecast, 587K previous

USA JOLTS Job Openings (Mar): 6.866M vs 6.84M forecast, 6.882M previous

**Bond Pricing**

**UMBS 30 yr**

| Coupon | Price | Intra-Day Change |

**GNMA 30 yr**

| Coupon | Price | Intra-Day Change |

**Treasuries**

| Term | Yield | Price | Intra-Day Yield Change |

| 2yr | 3.942 | 99.873 | -0.004 |

| 3yr | 3.97 | 98.683 | -0.001 |

| 5yr | 4.078 | 99.09 | -0.001 |

| 7yr | 4.25 | 99.999 | -0.003 |

| 10yr | 4.425 | 97.6 | -0.008 |

| 30yr | 4.987 | 96.332 | -0.028 |