WTMS Blog Today = What’s up in Mortgage Today (PM) – 05/11/2026

Bonds ended Monday where they started, trapped in a range after geopolitical news priced in overnight and the market spent the rest of the day drifting sideways. UMBS 5.0 fell 0.37 points to 98.52 while the 10-year Treasury climbed 5.2 basis points to 4.410%, with the real story being the lack of domestic movement during regular trading hours. Existing home sales disappointed at 4.02 million versus a 4.05 million forecast, adding modest pressure to mortgage demand as higher rates continue weighing on buyer activity.

The market remains range-bound between 4.34% and 4.40% on 10-year yields, waiting for Fed Chair Powell’s final week and upcoming inflation data to break the stalemate. Originators face negative repricing risk into rate sheet locks as MBS underperformed despite strong oil market correlations. The weak existing home sales data underscores why lock-and-hold strategies matter more than ever in volatile, sideways-moving markets.

Two Harbors continued dominating industry headlines as UWM escalated its competing bid to $12.50 per share in cash consideration, topping CrossCountry Mortgage’s $12 all-cash offer ahead of the scheduled May 19 shareholder vote. The battle has evolved beyond simple merger competition into broader conversations around MSR valuations, servicing economics, and gain-on-sale pressure across the wholesale channel. Industry observers are questioning the sustainability of aggressive pricing competition when servicing economics remain under intense pressure from higher costs and tighter margins.

Both bidders continue pushing valuations higher, forcing mortgage executives to reassess capital allocation and deal fundamentals in real-time. This escalation signals tension between acquisition appetite and the underlying profitability challenges facing the origination-servicing complex. Pending home sales reached their highest level in nearly four years as buyers responded to easing mortgage rates and improving inventory conditions despite persistent affordability pressures.

Contract signings climbed even as mortgage rates remain elevated, suggesting renewed housing demand after several sluggish years in the purchase market. The data contradicts some bearish expectations about buyer paralysis, though affordability concerns and broader market uncertainty continue limiting market participation. Stronger pending sales activity could eventually flow into closing volumes and correspondent seller pipelines for mortgage originators over the next 30-to-45 days.

This positive signal matters for lenders betting on purchase-market stabilization heading into the summer months. Blackstone launched a new residential development finance platform aimed at helping homebuilders secure construction funding amid tighter bank lending and elevated borrowing costs. The expansion into builder finance reflects growing capital marketplace competition and signals that alternative lenders are aggressively filling gaps left by traditional bank capital constraints.

This move could intensify pricing pressure on correspondent and wholesale lenders competing for builder business and construction loan servicing rights. Originators should monitor how non-bank capital flows influence builder mix and market share within their production channels. Mortgage shops with strong builder relationships may see opportunities to cross-sell permanent take-out financing alongside temporary construction funding.

Affordability pressures deepened even as home price growth flattened, with high mortgage rates, insurance costs, and limited inventory squeezing buyer purchasing power near record lows across major markets. The affordability crisis persists despite slower home appreciation, meaning rate relief alone may not spark demand without meaningful inventory increases or income growth. Loan officers should prepare messaging around rate-lock strategies, ARM products, and debt restructuring conversations as clients wrestle with compressed affordability.

This environment underscores why origination focuses must balance acquisition urgency with realistic borrower capacity assessment. The combination of rate uncertainty and affordability constraints creates both compliance risk and revenue opportunity for shops managing client expectations carefully. Federal Reserve Chair Jerome Powell enters his final week in office while Kevin Warsh prepares for confirmation hearings on the Fed chair succession, adding policy uncertainty to an already volatile rates environment.

Treasury yields continue facing resistance around 4.40% on the 10-year, with the curve watching Powell’s final comments before Warsh takes over as chair. Market-moving economic data over the next few days includes consumer price index and producer price index reports that could shift rate expectations significantly. Originators should plan for potential volatility in both directions heading into the Fed leadership transition and inflation data releases.

Bond market positioning around these events will dictate repricing risk and lock-and-hold strategy recommendations to retail borrowers through week’s end.

**Locking vs Floating**

Bonds remain range-bound between 4.34% and 4.40% on 10-year yields with no clear directional catalyst emerging in the near term. Geopolitical headlines about Middle East peace negotiations offer no reliable basis for lock-and-float decisions because political outcomes are impossible to predict and their market impact is volatile.

Over slightly longer horizons, a peace deal resolution would likely provide some rate benefit relative to current levels, making near-term locks defensible while waiting for clarity. For now, borrowers without specific closing deadlines should maintain tactical floating postures, but those closing within 45 days face meaningful reprice risk and should consider locking on any 2-3 basis point rallies.

**Today’s Events**

Existing home sales (April): 4.02 million versus 4.05 million forecast and 3.98 million prior month.

**Bond Pricing**

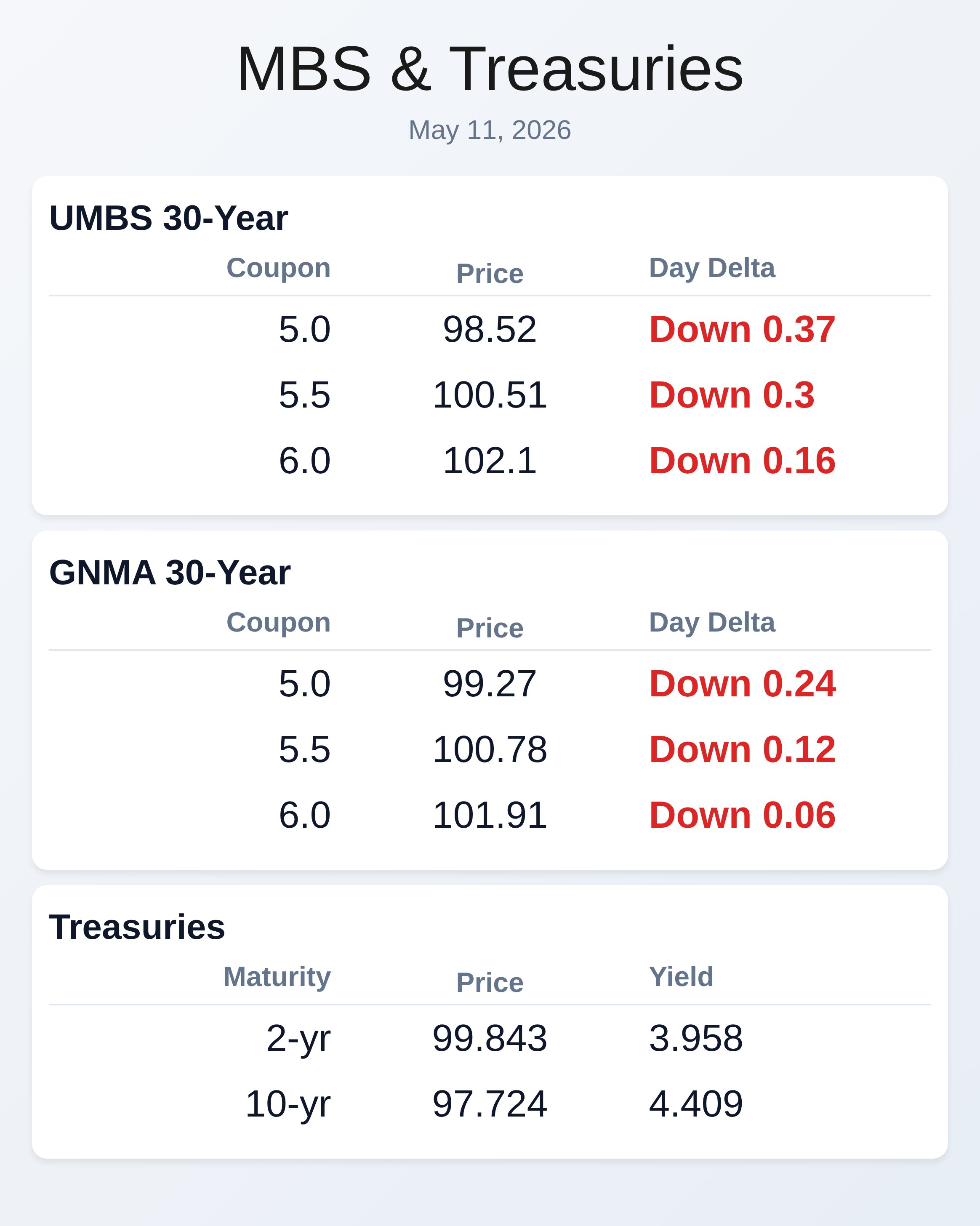

**UMBS 30 yr**

| Coupon | Price | Intra-Day Change |

| 5.0 | 98.52 | -0.37 |

| 5.5 | 100.51 | -0.30 |

| 6.0 | 102.10 | -0.16 |

**GNMA 30 yr**

| Coupon | Price | Intra-Day Change |

| 5.0 | 99.27 | -0.24 |

| 5.5 | 100.78 | -0.12 |

| 6.0 | 101.91 | -0.06 |

**Treasuries**

| Term | Yield | Price | Intra-Day Yield Change |