WTMS Blog Today = What’s up in Mortgage Today (AM) – 04/15/2026

Mortgage rates tumbled to their lowest point in a month as bond markets rallied on optimism that Middle East peace talks could end the Iran conflict, with the 30-year fixed dropping to 6.42%. Refinancing applications surged 5% for the week and sit 15% above year-ago levels, signaling that rate-sensitive borrowers are seizing the opportunity. However, purchase applications slipped 1% last week and remain 3% below last year’s levels, as economic uncertainty continues to sideline homebuyers.

The core inflation data delivered better-than-expected news, with March PPI showing just 0.1% monthly growth in core prices versus the 0.5% forecast. This pricing relief comes as the market now prices in contained inflation despite persistent geopolitical tensions and energy-driven volatility. Existing home sales hit their slowest pace since 2009, declining 3.6% month-over-month in March, according to the National Association of Realtors.

Sales fell across all four U.S. regions, with the median sale price reaching $408,800, down from earlier months. The year-over-year picture is mixed: the South and West showed gains while the Northeast and Midwest retreated further.

NAR Chief Economist Dr. Lawrence Yun attributed the weakness to lower consumer confidence and softer job growth that continues suppressing buyer activity. For mortgage originators, this translates to tighter purchase loan volume and increased pressure on refi-dependent business models.

Newrez is broadening access to its new Medical Professional Home Loan by opening the program to wholesale brokers, not just retail channels. The product features up to 100% financing with no PMI, qualifies physicians on projected income rather than current compensation, and treats student debt with flexible debt-to-income ratios. Loan amounts reach $2 million, targeting residents, fellows, and newly practicing physicians who possess strong long-term earning potential but fall outside standard agency or jumbo underwriting parameters.

This niche product expansion signals how lenders are carving out specialized lanes to capture origination volume in a competitive market. The Community Bankers Association is pushing the Federal Housing Finance Agency to fast-track VantageScore implementation in conventional mortgage underwriting, citing a staggering 1,567% increase in FICO-related costs over the past three and a half years. Equifax and TransUnion have already reduced VantageScore 4.0 pricing to approximately $1 per pull, but CHLA wants structural reform beyond pricing—specifically, directing Fannie and Freddie to develop in-house credit assessment capabilities.

This cost pressure reflects broader industry frustration that the multi-score transition isn’t advancing quickly enough while credit costs continue climbing, directly impacting lender margins and pricing competitiveness. March inflation data delivered modest relief across import and producer prices, with imports rising just 0.8% month-over-month against a forecast of 2.3%. The April Empire State Manufacturing Index surged to 11.0, well above expectations of negative 0.5, suggesting renewed economic optimism.

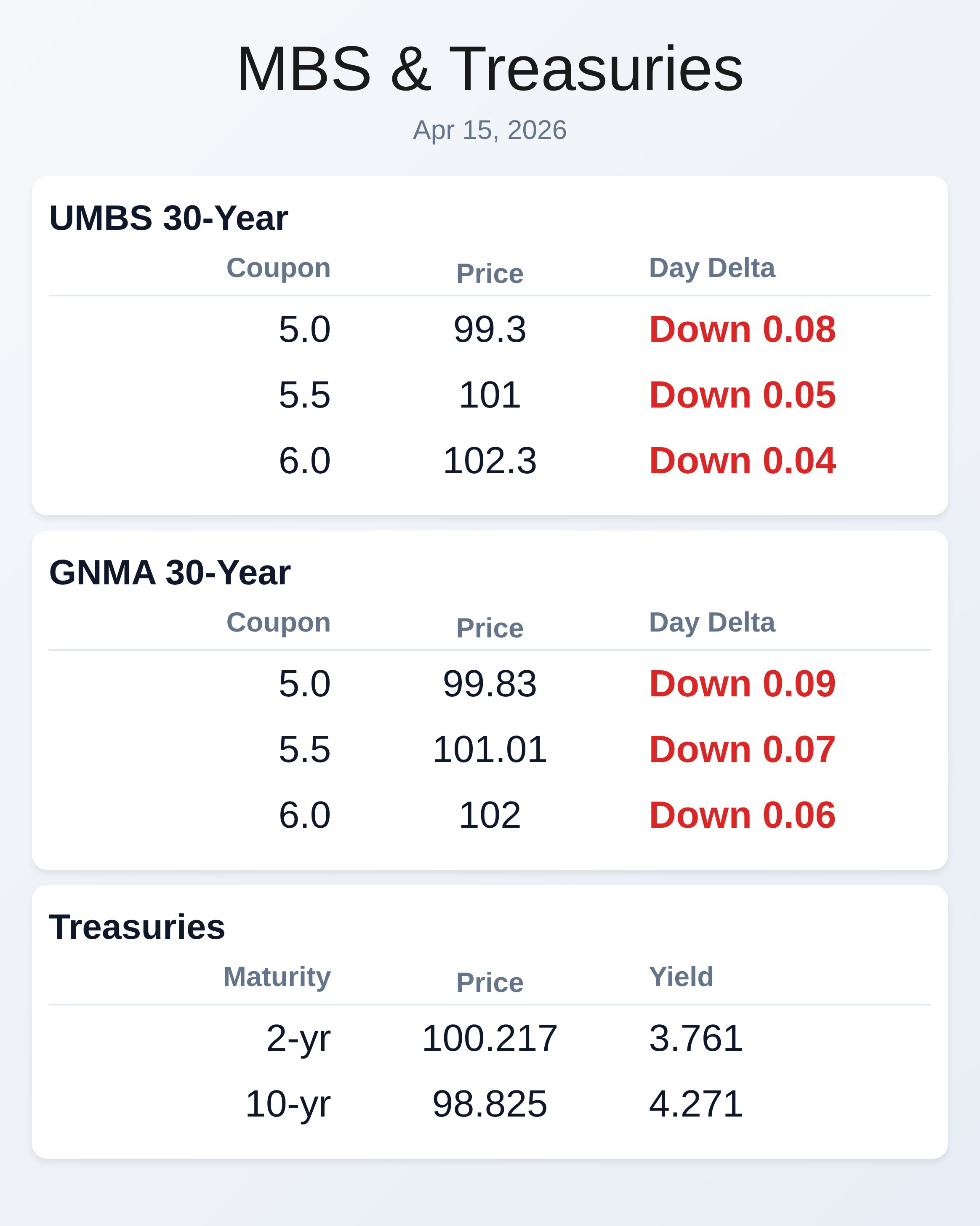

Bond prices responded positively, with 10-year Treasury yields rising modestly to 4.273% as markets reassess the inflation outlook in light of potential peace developments. UMBS 5.0 coupons trade at 99.27, down slightly from Tuesday’s close, while GNMA securities show similar modest weakness. Lock opportunities remain favorable as pricing has improved to four-week highs, though the market exhibits caution given the war’s uncertainty.

Two straight days of bond market gains represents the maximum winning streak seen since the conflict began, making this window potentially valuable for borrowers sitting on the fence between locking and floating. Today brings the NAHB Housing Market Index, the Federal Reserve’s Beige Book, Treasury auctions, and additional Fed commentary that could shift sentiment quickly. Origination teams should monitor oil prices closely, as they’ve become the primary near-term driver of bond volatility and rate direction.

Locking vs Floating

The bond market has notched two consecutive days of gains—the longest winning streak since the war started—offering a rare window for borrowers debating lock versus float. Current pricing represents the best levels in four weeks, suggesting this may be an opportune moment for rate-lock decisions. However, the market cautioned that two-day streaks have been the maximum seen recently, meaning extended gains cannot be assumed.

Those floating should remain alert to daily oil prices and geopolitical headlines, as sentiment can shift rapidly even with modest economic data surprises.

Today’s Events

Core PPI m/m (Mar): 0.1% vs 0.5% forecast

Core PPI y/y (Mar): 3.8% vs 4.1% forecast

PPI m/m (Mar): 0.5% vs 1.1% forecast

PPI y/y (Mar): 4.0% vs 4.6% forecast

Import prices m/m (Mar): 0.8% vs 2.0% forecast

NY Fed Manufacturing (Apr): 11.0 vs -0.5 forecast

NAHB Housing Market Index (Apr)

Federal Reserve Beige Book

Treasury auctions (short-duration)

Bond Pricing

UMBS 30 yr

| Coupon | Price | Intra-Day Change |

| 5.0 | 99.27 | -0.11 |

| 5.5 | 100.98 | -0.07 |

| 6.0 | 102.3 | -0.04 |

GNMA 30 yr

| Coupon | Price | Intra-Day Change |

| 5.0 | 99.87 | -0.04 |

| 5.5 | 101.0 | -0.07 |

| 6.0 | 101.97 | -0.09 |

Treasuries

| Term | Yield | Price | Intra-Day Yield Change |

| 2 yr | 3.764 | 100.213 | 0.021 |

| 3 yr | 3.78 | 99.214 | 0.015 |

| 5 yr | 3.89 | 99.931 | 0.022 |

| 7 yr | 4.072 | 101.078 | 0.026 |

| 10 yr | 4.273 | 98.805 | 0.023 |

| 30 yr | 4.881 | 97.954 | 0.023 |