**WTMS Blog Today = What’s up in Mortgage Today (AM) – 05/18/2026**

The New York Federal Reserve manufacturing index exploded to 19.60 in May, crushing the 7.5 forecast and signaling unexpected economic strength that sent bond yields higher across the curve. Industrial production also beat expectations with a 0.7% gain in April versus the 0.3% forecast, reversing prior weakness and fueling fears that inflation pressures may intensify. These hotter-than-expected data points arrive amid elevated crude oil prices holding above $100 per barrel, driven by uncertainty surrounding the Iran conflict and the Strait of Hormuz.

The combination of stronger growth and energy-driven inflation concerns has markets pricing in a 60-40 probability of a Federal Reserve rate hike by January, forcing mortgage professionals to monitor geopolitical risk alongside domestic economics. Bond yields drifted weaker intraday despite the hawkish data, with Treasury curves showing modest volatility as investors digest the inflation implications. Mortgage originators face mounting cost pressures as per-loan origination costs climbed to $11,898 in Q1 2026 from $11,102 in Q4 2025, highlighting the competitive squeeze between pricing and production efficiency.

The CFPB remains a significant regulatory force despite prior Administration statements suggesting reductions, as the bureau requested funding exceeding $140 million for fiscal 2026 and continues advancing discrete rulemaking initiatives. Current CFPB priorities include addressing loan officer compensation structures, finalizing the servicing rule, refining ability-to-repay standards, and streamlining refinance documentation requirements. The MBA is collaborating with the agency on credit modernization discussions that question traditional tri-merge credit reporting and pilot programs under review by the FHFA.

Mortgage professionals should expect continued regulatory evolution around AI governance, vendor oversight, and consumer data usage, as demonstrated by scheduled industry panels at MBA Secondary addressing legal and compliance realities. Compliance teams must stay aligned with evolving agency expectations rather than assuming deregulatory momentum. Housing affordability remains a structural headwind as U.S.

Homeowners with mortgages now pay 37 percent more per month than renters, forcing prospective borrowers toward difficult choices including potential relocation for affordable property. LendingTree data highlights that rental markets outperform ownership costs in every major metropolitan area, even in the tightest housing markets, due to elevated mortgage rates and home prices. This affordability crisis creates opportunity in reverse mortgages and home equity tapping solutions, given that $14.5 trillion in senior home equity remains largely untapped by traditional refinance programs.

Mortgage professionals operating in origination-constrained environments should explore alternative products and client segments that address specific affordability barriers and liquidity needs. The shift toward equity extraction and non-traditional loan products reflects realistic adaptation to persistent rate and price headwinds. Capital markets remain dominated by geopolitical risk over domestic economic data, as oil prices and Iran conflict developments drive investor sentiment and bond yields far more than traditional inflation metrics or Fed policy signals.

Treasury yields hold elevated levels near year-to-date highs following last week’s selloff on hot consumer and producer price prints combined with climbing energy costs. Market participants are increasingly focused on April FOMC meeting minutes scheduled for release this week to assess committee debate on the path of policy prior to Fed Chairman Kevin Warsh’s recent swearing-in. The question of whether committee members view the next move as equally likely to be a rate cut versus a rate hike will carry amplified weight given recent inflation surprises.

Until geopolitical tensions ease or energy prices stabilize, rate volatility and mortgage rate uncertainty should be expected.

**Locking vs Floating**

Yield ceilings and floors have proved useful for tracking broader bond market momentum, particularly when sharp breakouts test levels unseen for a year. A peaceful resolution to the Iran conflict would likely push rates lower, but the timeline remains unknowable and dependent on developments outside traditional economic forecasting.

Borrowers should remain cautious about floating rate locks until clarity emerges on energy markets and geopolitical trajectories.

**Today’s Events**

NY Fed Manufacturing (May): 19.60 vs 7.5 forecast, 11.00 previous

Industrial Production (April): 0.7% vs 0.3% forecast, -0.5% previous

**Bond Pricing**

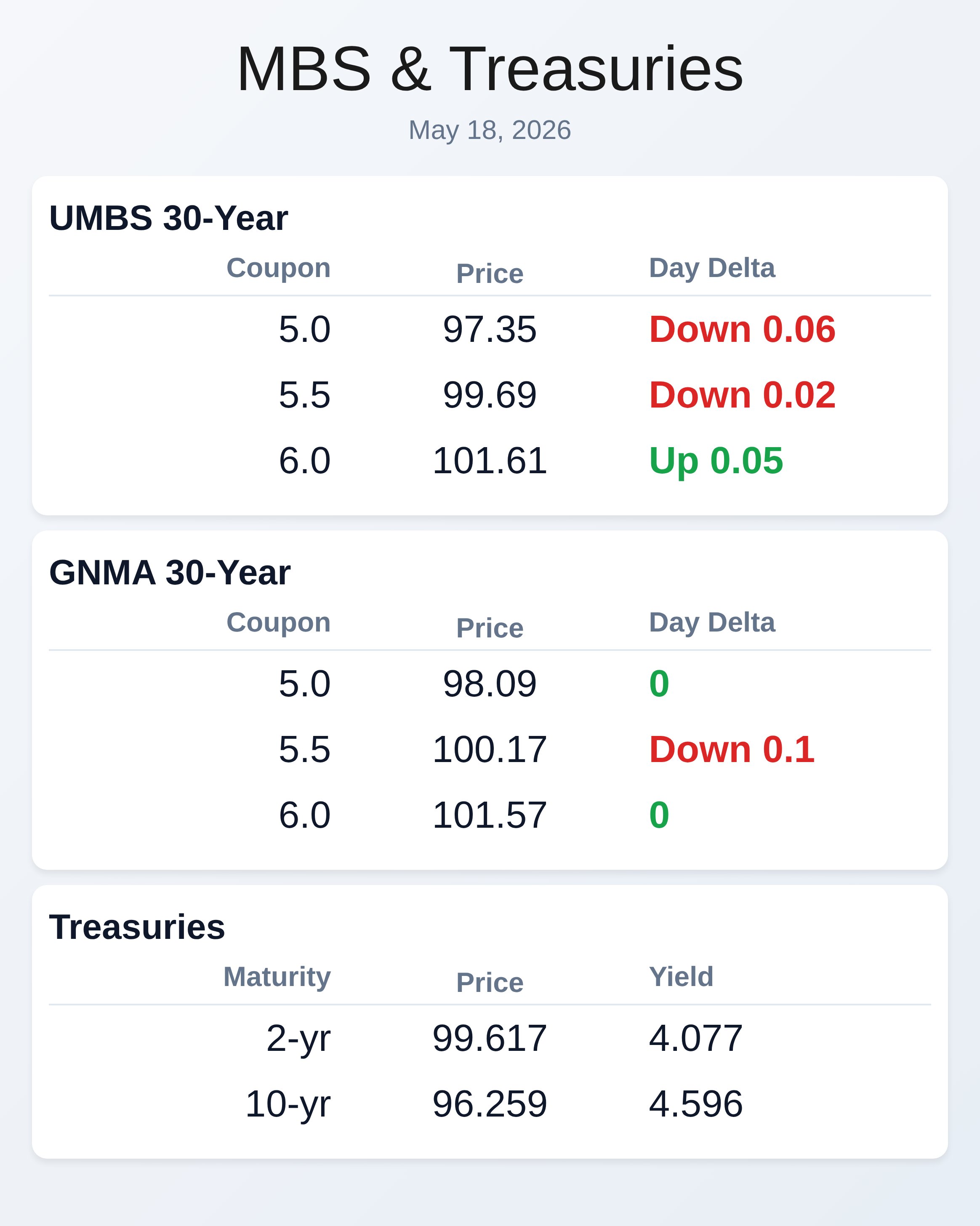

**UMBS 30 yr**

| Coupon | Price | Intra-Day Change |

| 5.0 | 97.35 | -0.06 |

| 5.5 | 99.69 | -0.02 |

| 6.0 | 101.61 | 0.05 |

**GNMA 30 yr**

| Coupon | Price | Intra-Day Change |

| 5.0 | 98.09 | 0 |

| 5.5 | 100.17 | -0.1 |

| 6.0 | 101.57 | 0 |

**Treasuries**

| Term | Yield | Price | Intra-Day Yield Change |

| 2 yr | 4.077 | 99.617 | -0.009 |

| 3 yr | 4.142 | 98.206 | -0.001 |

| 5 yr | 4.256 | 98.299 | 0.008 |

| 7 yr | 4.424 | 98.963 | 0.009 |

| 10 yr | 4.596 | 96.259 | 0.001 |

| 30 yr | 5.125 | 94.285 | 0.007 |