**WTMS Blog Today = What’s up in Mortgage Today (PM) – 05/15/2026**

Mortgage-backed securities plunged 0.75 points Friday as global uncertainty over Iran tensions and persistent inflation fears sent Treasury yields soaring to one-year highs. The 10-year Treasury hit 4.6%, a psychological ceiling that forced bond investors to reassess rate expectations well into 2027, meaning mortgage rates are pricing in extended duration of elevated borrowing costs. NY Fed Manufacturing came in at a scorching 19.60 versus forecast of 7.5, while Industrial Production beat at 0.7% versus 0.3% expected, painting a picture of a surprisingly resilient economy despite recession warnings.

These hot economic reads collided head-on with geopolitical anxiety, creating a whipsaw environment where rates moved sharply higher throughout the session with MBS and 10-year yields unable to find any ground. For mortgage originators, Friday’s volatility underscores the challenge of rate sheet management when economic strength clashes with inflation persistence and no clear path to Fed rate cuts. Kevin Warsh’s Senate confirmation as the next Federal Reserve Chair offered brief market optimism, but the rally quickly faded when reality sank in: sticky inflation dynamics and Iran conflict uncertainty mean rate-cutting expectations are being pushed further into the future.

Markets had anticipated Warsh’s first FOMC meeting in June might signal dovish policy shifts, yet energy price spikes and broad-based inflation data have complicated that timeline considerably. The 30-year fixed mortgage rate sat at 6.66% on Thursday and appears destined to push higher given Friday’s yield trajectory, squeezing both purchase and refinance volume. Treasury auctions this week showed weak demand for long-duration bonds, with pension funds and insurance companies demanding higher yields to absorb new supply.

For lenders, this signals that rate stability remains elusive and client conversations must shift from rate relief hopes to longer-term financing strategies. The Rocket/UWM servicing lawsuit escalates an already contentious competitive environment in mortgage origination, with Rocket claiming UWM violated non-solicit agreements by targeting 182,000 Mr. Cooper borrowers through aggressive rate cuts and AI-powered marketing systems.

UWM’s “Refi Shield 100” program and its KEEP AI system allegedly breached the 2024 MSR sale agreement, costing Rocket nearly $100 million in lost servicing revenue since the Mr. Cooper acquisition. UWM fired back calling the lawsuit “baseless and opportunistic,” pointing to the suspicious timing of the filing after Rocket closed the Mr.

Cooper deal and after former UWM wholesale executive Mike Fawaz announced a UWM partnership. The legal battle reveals deeper tensions around competitive poaching and the enforceability of non-solicit covenants in an AI-enabled origination landscape. Originators watching this case should understand that aggressive borrower acquisition strategies now carry measurable legal and financial risk, particularly when targeting seasoned loan portfolios.

The Two Harbors/CrossCountry/UWM merger battle intensifies as shareholders prepare for the May 19 vote, with UWM accusing Two Harbors of “smoke and mirrors” over dividend announcements and valuation messaging. CrossCountry matched UWM’s $12-per-share offer earlier this week, pivoting the contest to governance, servicing economics, and how deal value is being communicated to shareholders rather than pure dollar amounts. The rhetoric has grown sharper as both sides trade pointed statements, suggesting underlying strategic concerns about servicing rights, MSR valuations, and post-merger integration risk.

For mortgage servicing professionals, the outcome will reshape competitive positioning in the servicing sector and may signal how much acquirers are willing to pay for mortgage-backed loan portfolio rights going forward. This high-stakes proxy battle is essentially a referendum on servicing viability at current interest rate environments and borrower prepayment assumptions. Ginnie Mae prepayment speeds slowed meaningfully in April as refinancing activity dried up, with VA loans continuing to prepay materially faster than FHA loans thanks to VA streamline efficiency.

Servicer dispersion remained wide, with firms like Rocket generating faster prepayments while regional banks and depositories produced stickier collateral reflecting differing customer bases and servicing strategies. This bifurcation means extension risk is real for investors holding slower-paying pools while seasoning and borrower composition become critical valuation drivers. Mortgage-backed security investors are increasingly focused on collateral selection and specified pool characteristics to manage convexity, knowing that broad refinancing waves are off the table for the foreseeable future.

For lenders holding long-duration MSR portfolios, these dynamics underscore the importance of strategic servicer partnerships and granular borrower-level analytics. Real wages have turned negative after inflation adjustment, a troubling signal for consumer spending resilience even as retail sales and unemployment figures suggest near-term economic stability. Small business confidence remains subdued while existing home sales continue lagging long-term norms, hinting that housing affordability strain is beginning to filter through buyer behavior despite headline economic strength.

The disconnect between positive labor market data and weakening real wage growth suggests consumers are becoming increasingly price-sensitive on groceries, gasoline, and housing costs. Fed policymakers now face a complex scenario: persistent inflation paired with potential growth slowdown leaves little room to cut rates without risking renewed price acceleration. Mortgage originators should prepare messaging that emphasizes long-term commitment to borrowers facing affordability headwinds, positioning purchase and rate-and-term refinance strategies around life planning rather than purely rate-dependent decisions.

**Locking vs Floating**

Range breakouts at one-year highs change the calculus entirely for lock-versus-float decision-making. While a peaceful Iran resolution would theoretically support lower rates, the timeline is unknowable and yields are now testing resistance at 4.66 with floors at 4.05 and 4.12. When volatility hits this magnitude, traditional float strategies lose credibility because borrowers cannot predict when market normalization occurs.

The best guidance is to counsel clients on worst-case scenarios rather than base-case recovery, effectively recommending locks for committed timelines.

**Today’s Events**

NY Fed Manufacturing (May): 19.60 vs. 7.5 forecast, 11.00 previous

Industrial Production (April): 0.7% vs.

0.3% forecast, -0.5% previous

**Bond Pricing**

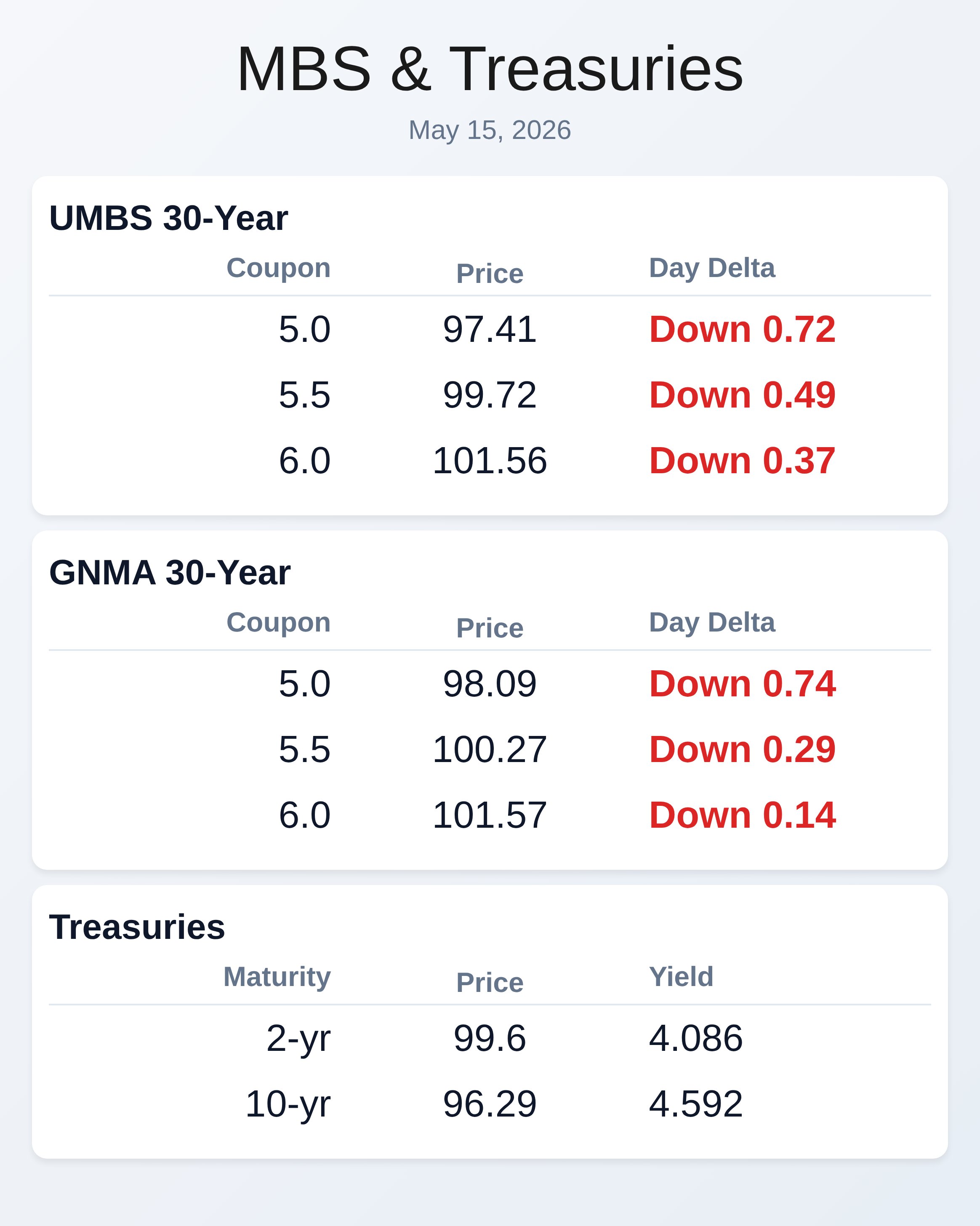

**UMBS 30 yr**

| Coupon | Price | Intra-Day Change |

|5.0|97.41|-0.72|

|5.5|99.72|-0.49|

|6.0|101.56|-0.37|

**GNMA 30 yr**

| Coupon | Price | Intra-Day Change |

|5.0|98.09|-0.74|

|5.5|100.27|-0.29|

|6.0|101.57|-0.14|

**Treasuries**

| Term | Yield | Price | Intra-Day Yield Change |