**WTMS Blog Today = What’s up in Mortgage Today (AM) – 05/13/2026**

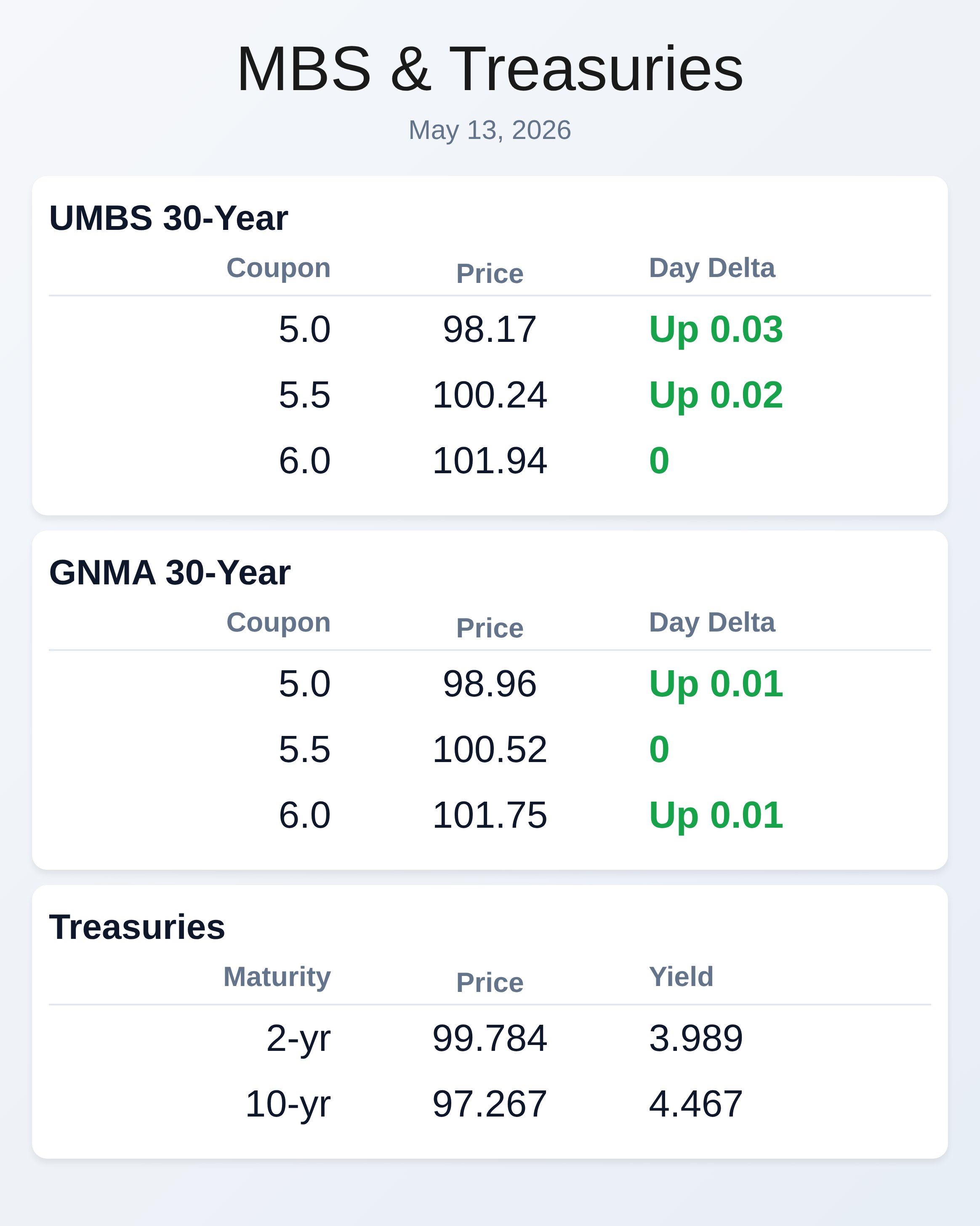

War headlines and auction concessions have pushed 10-year Treasury yields to their highest level in 10 months, signaling stronger headwinds for mortgage originators. The 10-year Treasury yield jumped 1.4 basis points to 4.467 percent, while UMBS 30-year coupons showed minimal intraday movement across all coupon levels. GNMA 30-year securities similarly held steady, with the 6.0 coupon unchanged and lower coupons barely budging.

Market volatility remains elevated due to geopolitical uncertainty, making it harder to establish reliable lock and float strategies in the near term. This selloff reflects broader bond market pressure rather than mortgage-specific weakness. Core inflation data beat expectations on the month, with headline CPI also running hotter than forecast, creating additional upward pressure on longer-dated yields.

Core CPI rose 0.4 percent versus 0.3 percent expected and 0.2 percent prior, while year-over-year core inflation accelerated to 2.8 percent from 2.6 percent. Headline inflation on a monthly basis matched the 0.6 percent forecast but year-over-year readings climbed to 3.8 percent from 3.3 percent. The broader inflation story remains sticky despite some moderation from prior year comparisons.

Originators should expect elevated rate volatility to persist through the upcoming week. The two-year Treasury dipped 1 basis point to 3.989 percent, suggesting some flattening across the shorter end of the curve despite the 10-year’s sharp move higher. Mid-curve yields like the five-year and seven-year also moved modestly lower, with the five-year down 1 basis point to 4.124 percent.

The 30-year Treasury remained flat at 5.026 percent, maintaining a wide spread versus the 10-year that reflects market uncertainty about long-term inflation and growth. Current pricing suggests bond traders are hedging against recession risks even as inflation data disappoint. The yield curve continues to signal mixed economic signals.

**Locking vs Floating**

Geopolitical tensions are creating unpredictable market swings that defy traditional rate forecast models. Short-term lock and float decisions should not be based on war headlines because volatility could move in either direction without warning or schedule. A peace agreement would likely provide some relief to rates compared to current levels, but timing such a resolution is impossible.

Originators may want to consider the longer-term probability of de-escalation rather than making tactical decisions on daily newsflow. Hedging current pipeline positions is more prudent than betting on near-term direction during this period of elevated uncertainty.

**Today’s Events**

Core CPI (April): 0.4% monthly vs.

0.3% forecast, 2.8% year-over-year vs. 2.7% forecast

Headline CPI (April): 0.6% monthly vs. 0.6% forecast, 3.8% year-over-year vs.

3.7% forecast

**Bond Pricing**

**UMBS 30 yr**

| Coupon | Price | Intra-Day Change |

| 5.0 | 98.17 | 0.03 |

| 5.5 | 100.24 | 0.02 |

| 6.0 | 101.94 | 0 |

**GNMA 30 yr**

| Coupon | Price | Intra-Day Change |

| 5.0 | 98.96 | 0.01 |

| 5.5 | 100.52 | 0 |

| 6.0 | 101.75 | 0.01 |

**Treasuries**

| Term | Yield | Price | Intra-Day Yield Change |

| 2 yr | 3.989 | 99.784 | -0.001 |

| 3 yr | 4.023 | 98.536 | -0.003 |

| 5 yr | 4.124 | 98.886 | -0.001 |

| 7 yr | 4.291 | 99.754 | -0.003 |

| 10 yr | 4.467 | 97.267 | 0.014 |

| 30 yr | 5.026 | 95.75 | 0 |