**WTMS Blog Today = What’s up in Mortgage Today (PM) – 05/12/2026**

War headlines pushed bond markets to their worst levels in 10 months as geopolitical tensions triggered aggressive selling across both MBS and Treasuries. The 10-year yield climbed 5.2 basis points to 4.461 percent by late afternoon, while UMBS 5.0 coupons fell a full quarter point to 98.14. This morning’s April CPI report showed core inflation at 0.4 percent month-over-month versus a 0.3 percent forecast, yet bonds initially shrugged off the data—the real damage came when war escalation comments hit the newswire.

For mortgage originators, this sharp repricing increases negative reprice risk on pipeline, making lock decisions more urgent as volatility shows no signs of subsiding before next week. Volatility makes lock-float strategy nearly impossible to execute in the short term because geopolitical events don’t follow a predictable schedule and could swing rates either direction. Longer-dated strategic thinking suggests that a peace deal—whenever it arrives—would likely push rates meaningfully lower from current levels, giving originators a window for future rate locks.

The real question for your pipeline is whether you have enough rate lock cushion to survive another 4–5 days of headline risk without eating through your margins. Most originators should assume rates stay elevated unless we get genuine peace news, making today’s repricing more of a ceiling than a temporary spike. Institutional Shareholder Services just recommended Two Harbors shareholders reject the CrossCountry Mortgage deal, adding pressure to a proxy fight that United Wholesale Mortgage is actively trying to win.

UWM’s latest offer of $12.50 per share in cash for elections now carries more weight because ISS raised questions about whether CrossCountry’s “certainty narrative” actually protects shareholder value. The industry backdrop matters here—stretched valuations, tightening margins, and aggressive pricing during a mortgage surge mirror pre-2008 conditions, making deal certainty less certain than Two Harbors’ board has argued. For loan officers, this drama highlights how quickly market fundamentals can shift and underscores the importance of locking rates while still available at known pricing levels.

Lower rates earlier this spring drove refi volume to a four-year high while home prices posted their strongest quarterly gain in nearly two years according to ICE data. This combination gave loan officers a more balanced pipeline mix between purchase and refi business, improving overall profitability per loan. Technology platforms like MeridianLink are reporting record mortgage platform adoption as lenders scramble to improve efficiency and reduce costs in a margin-compressed environment.

For originators, this trend means technology is becoming less of a competitive luxury and more of an operational necessity to stay profitable. Treasuries across the entire yield curve rose sharply, with the 2-year at 3.989 percent, the 5-year at 4.125 percent, and the 30-year climbing to 5.026 percent—all up 3–5 basis points during the session. GNMA 30-year coupons fell even harder than UMBS, reflecting both the war risk premium and aggressive short covering in high-coupon pools.

The technical ceiling at 4.66 percent in the 10-year remains critical; any close above that level signals a breakdown in near-term support and probable acceleration toward 4.75 percent. Monitor your client communication carefully today because hotter inflation, higher oil prices above $100, and unresolved war risk create a perfect storm for upward rate pressure into month-end.

**Locking vs Floating**

War headlines dominate the short-term risk picture, making any lock-float strategy based on near-term technicals unreliable due to unpredictable geopolitical catalysts.

In the long term, peace would likely deliver meaningful rate relief, but no one can forecast when that occurs. Most originators should assume current levels are sticky and lock any marginal pipelines to avoid negative repricing surprises over the next week.

**Today’s Events**

m/m CORE CPI (Apr): 0.4% vs 0.3% forecast, 0.2% prior

m/m Headline CPI (Apr): 0.6% vs 0.6% forecast, 0.9% prior

y/y CORE CPI (Apr): 2.8% vs 2.7% forecast, 2.6% prior

y/y Headline CPI (Apr): 3.8% vs 3.7% forecast, 3.3% prior

**Bond Pricing**

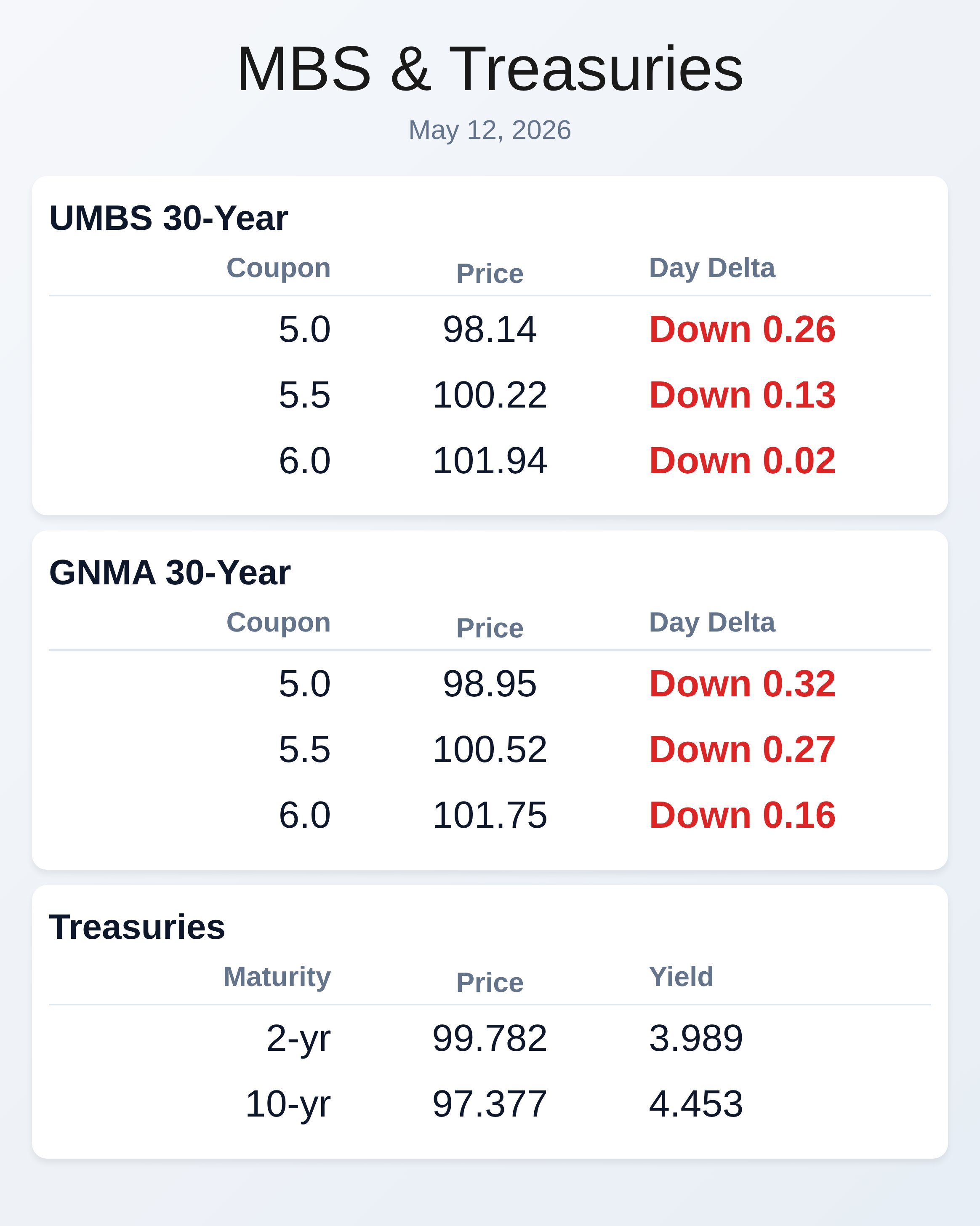

**UMBS 30 yr**

| Coupon | Price | Intra-Day Change |

| 5.0 | 98.14 | -0.26 |

| 5.5 | 100.22 | -0.13 |

| 6.0 | 101.94 | -0.02 |

**GNMA 30 yr**

| Coupon | Price | Intra-Day Change |

| 5.0 | 98.95 | -0.32 |

| 5.5 | 100.52 | -0.27 |

| 6.0 | 101.75 | -0.16 |

**Treasuries**

| Term | Yield | Price | Intra-Day Yield Change |

| 2 yr | 3.989 | 99.782 | 0.038 |

| 3 yr | 4.025 | 98.53 | 0.05 |

| 5 yr | 4.125 | 98.881 | 0.054 |

| 7 yr | 4.294 | 99.738 | 0.054 |

| 10 yr | 4.453 | 97.377 | 0.044 |

| 30 yr | 5.026 | 95.743 | 0.039 |