**WTMS Blog Today = What’s up in Mortgage Today (AM) – 05/14/2026**

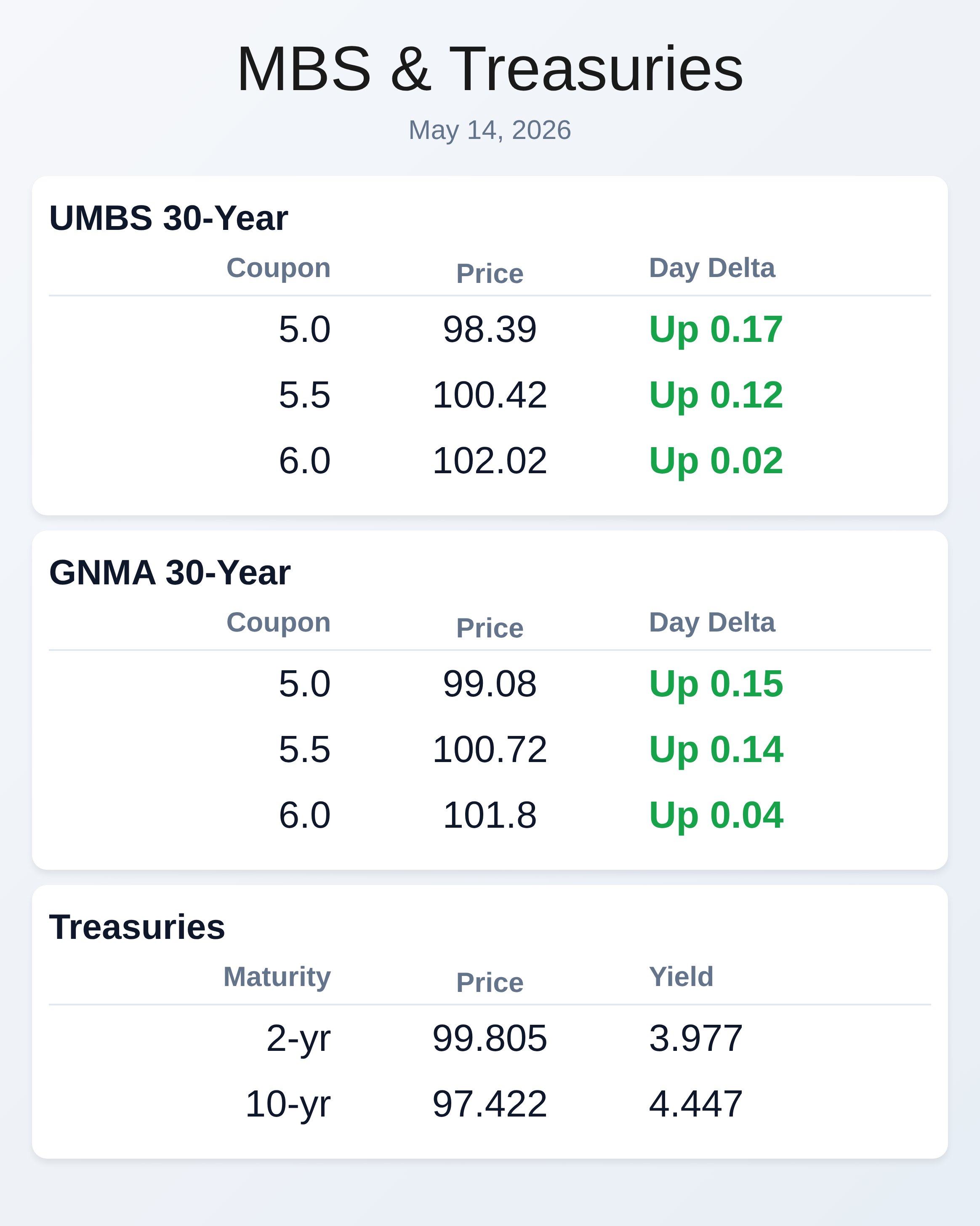

MBS rallied strongly overnight after initially selling off when producer prices crushed forecasts, with the 30-year UMBS 5.0 coupon gaining 22 basis points to 98.44 while the 10-year Treasury fell 30 basis points to 4.443%. Retail sales came in exactly on target at 0.5%, and jobless claims at 211K were only marginally higher than the 205K estimate, providing no fresh volatility. April import prices surged 1.9% month-over-month, nearly double the 1.0% forecast, with a 6.0% year-over-year producer price increase signaling broad-based inflation pressures tied to energy and industrial goods.

Oil’s recent pullback and growing optimism around the Trump-Xi meeting helped bonds stabilize after Tuesday’s PPI shock. GNMA securities mirrored the UMBS strength, with the 5.5 coupon at 100.72, up 14 basis points, though longer-dated spreads remain under pressure from geopolitical uncertainty. The mortgage origination industry is absorbing significant technology shifts as AI platforms now execute trades on live mortgage pipelines for the first time, marking a watershed moment in capital markets automation.

MCT’s Atlas delivered the industry’s first AI-powered trade execution on UMBS TBAs this week after recommending hedge trades at MBA Secondary 2025, demonstrating that artificial intelligence can operate within defined risk parameters to complete electronic auctions autonomously. Meanwhile, eNote adoption continues accelerating with over 90 investors now accepting digital notes through the MERS eRegistry, eliminating investor acceptance as a barrier to implementation. Lenders pursuing asset-based lending strategies are seeing record funding volumes, with one platform closing $103 million across 111 loans in April alone, a 91% year-over-year increase.

Bankruptcy servicing workflows remain a critical operational challenge as rising volume exposes gaps in coordination, proof-of-claim accuracy, and Rule 3002.1 compliance across servicers managing portfolios under federal stay protections. The 10-year Treasury yield moved lower despite inflation pressures, closing at 4.44% as investors rotated toward fixed income ahead of potential Fed policy shifts and a full rate hike already priced in for early 2027. Kevin Warsh’s Senate confirmation as Federal Reserve Chair by the narrowest margin in history (54-45) signals contentious rate-setting deliberations ahead, especially as market participants debate whether inflation will spike for only three to four months or persist through the end of the year.

The 30-year Treasury auction yesterday drew decent demand with a 2.30x bid-to-cover ratio, though non-dealer takedown at 88% and a “tail” of 0.5 basis points suggest investors still wanted higher yields to own long-duration government paper. Supply-and-demand dynamics for 30-year mortgages shifted meaningfully as institutional buyers found 5.0% yields attractive for the first time since 2007, pulling demand toward long-dated instruments. War headlines and Middle East escalation, including reports of vessel seizures near the Strait of Hormuz, continue to cloud the outlook and prevent any meaningful lock-float strategy based on short-term geopolitical developments.

Mortgage bankers should remain defensive and focus on capital preservation rather than aggressive risk-taking as volatility persists above the longer-term average despite recent stabilization. Current coupon spreads trade near the middle of recent ranges, indicating neither compelling value nor significant overhang in MBS valuation overall. Higher-coupon specified pools offer better relative value than current coupons, particularly for loans with strong FICO scores or investor properties that command tighter pay-ups in secondary market trading.

The 5.0% UMBS coupon’s resilience at 98.44 reflects investor appetite for discounted paper despite rate uncertainty, while GNMA securities continue to track UMBS with slight premium pricing reflecting investor preferences for government-backed securities. Traders should anticipate continued monitoring of oil prices and Middle East developments as leading indicators for bond market direction, since energy costs remain the primary driver of inflation expectations until geopolitical headlines stabilize.

**Locking vs Floating**

War-driven volatility in bonds makes tactical lock-float strategies unreliable on an intraday basis since geopolitical headlines do not follow predictable schedules and potential price swings are elevated.

Peace negotiations or a formal deal would likely benefit mortgage rates versus current levels over the longer term. Instead of reacting to daily war news, originators should track 10-year Treasury ceilings and floors to identify bigger-picture bond market momentum, which reveals whether the mortgage market is entering a new trading range.

**Today’s Events**

April Import Prices Month-over-Month: 1.9% vs 1.0% forecast

May Jobless Claims: 211,000 vs 205,000 forecast

April Retail Sales Month-over-Month: 0.5% vs 0.5% forecast (in-line)

April Retail Sales Control Group: 0.5% vs 0.4% forecast

**Bond Pricing**

**UMBS 30 yr**

| Coupon | Price | Intra-Day Change |

**GNMA 30 yr**

| Coupon | Price | Intra-Day Change |

**Treasuries**

| Term | Yield | Price | Intra-Day Yield Change |

| 2 yr | 3.965 | 99.805 | -0.006 |

| 3 yr | 4.012 | 98.565 | -0.006 |

| 5 yr | 4.096 | 98.969 | -0.011 |

| 7 yr | 4.269 | 99.887 | -0.021 |

| 10 yr | 4.443 | 97.422 | -0.018 |

| 30 yr | 5.003 | 96.091 | -0.033 |