**WTMS Blog Today = What’s up in Mortgage Today (PM) – 06/03/2026**

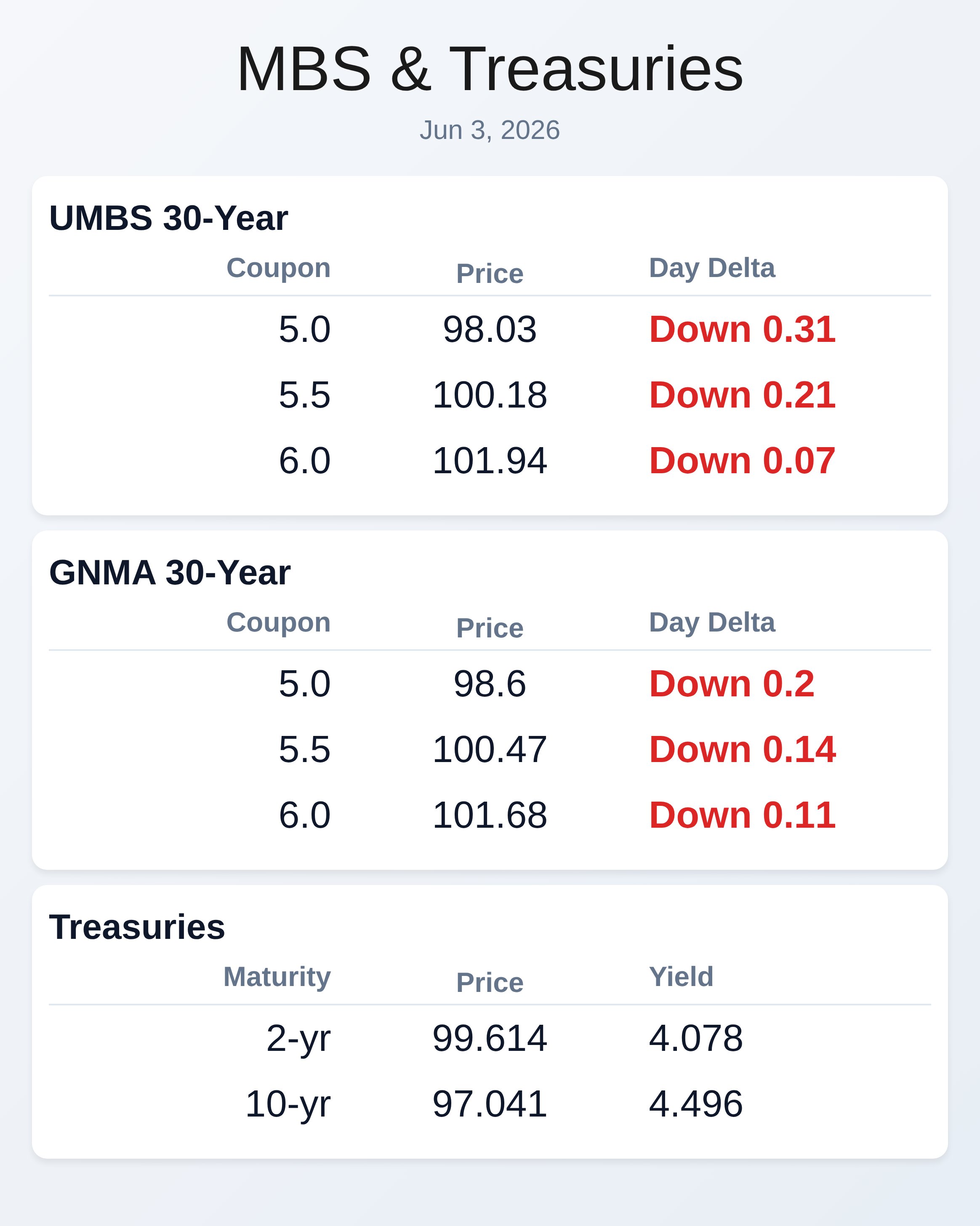

War headlines reignited overnight as Iran launched strikes against U.S. and allied sites, pushing Treasury yields higher and keeping the 10-year locked in a narrow 4.43 to 4.51 trading range. UMBS 5.0 fell 32 basis points to 98.02 while the 10-year yield climbed to 4.498%, marking the highest levels of the session by mid-afternoon.

MBS prices weakened nearly a full eighth of a point from this morning’s best levels, suggesting lenders may face negative repricing risk if they hit those brief windows. Oil prices surged to week-high levels overnight before settling, confirming that geopolitical anxiety remains the dominant driver of daily volatility. Despite the weakness, markets remain contained within the established trading corridor, limiting panic-driven repricing.

Economic data delivered mixed signals but failed to dominate price action. ADP employment came in at 122,000 versus a 117,000 forecast and 109,000 prior reading, showing resilience in private hiring activity. ISM Non-Manufacturing PMI expanded to 54.5 against expectations of 53.8, while services new orders jumped to 57.3 from 53.5, indicating solid business activity momentum.

However, services employment data declined slightly to 47.9, and services prices pushed higher to 71.3, suggesting some inflationary pressure persists in the labor market. The positive jobs data complicates the case for lower rates, as strong employment typically justifies holding interest rates firm or keeping them higher longer. Treasury volatility remains driven by geopolitical headlines rather than fundamental economic shifts.

The 2-year yield gained 3.2 basis points, the 5-year climbed 4.5 basis points, and the 10-year rose 4.3 basis points throughout the session. Longer-dated bonds like the 30-year added only 2.7 basis points, showing the curve’s typical response to near-term risk events. War-related sensitivity continues accounting for 90% of forward-looking volatility, leaving economic data and Fed policy guidance in secondary positions.

This pattern makes overnight floating an unpredictable proposition for lenders managing rate locks and closing pipelines.

**Locking vs Floating**

Overnight floating has become increasingly risky as geopolitical events trigger sharp intraday moves with minimal notice. War headlines are producing 50-basis-point swings within windows of just 15 to 20 minutes, making it difficult for loan officers to time market windows.

The sensitivity level remains lower than two weeks ago, but the willingness to react on each new headline suggests continued volatility ahead. For borrowers on the fence, locking now provides certainty that protects against Iran escalation risk or unexpected military developments. Those within the 4.43 to 4.51 yield range should consider this a defensible entry point for longer-term lock commitments.

**Today’s Events**

ADP employment (May): 122K vs. 117K forecast, 109K prior

ISM Non-Manufacturing PMI (May): 54.5 vs. 53.8 forecast, 53.6 prior

ISM Services Employment (May): 47.9 vs.

prior 48.0

ISM Services New Orders (May): 57.3 vs. 53.5 prior

ISM Services Prices (May): 71.3 vs. 70.7 prior

**Bond Pricing**

**UMBS 30 yr**

| Coupon | Price | Intra-Day Change |

**GNMA 30 yr**

| Coupon | Price | Intra-Day Change |

**Treasuries**

| Term | Yield | Price | Intra-Day Yield Change |