“Damn, there is so much great knowledge out there. Did you know that “BOOKS” are full of smart?? No, I mean like life changing, I-wish-I-knew-that-years-ago type stuff.

I know that I was waaaayyy late to the game figuring it out. And I know that a lot of you are too busy to read as much as you ‘should’. And that is why you need me.

I still remember how it started for me. It started in June of 2008. After 11 years …..Click to continue

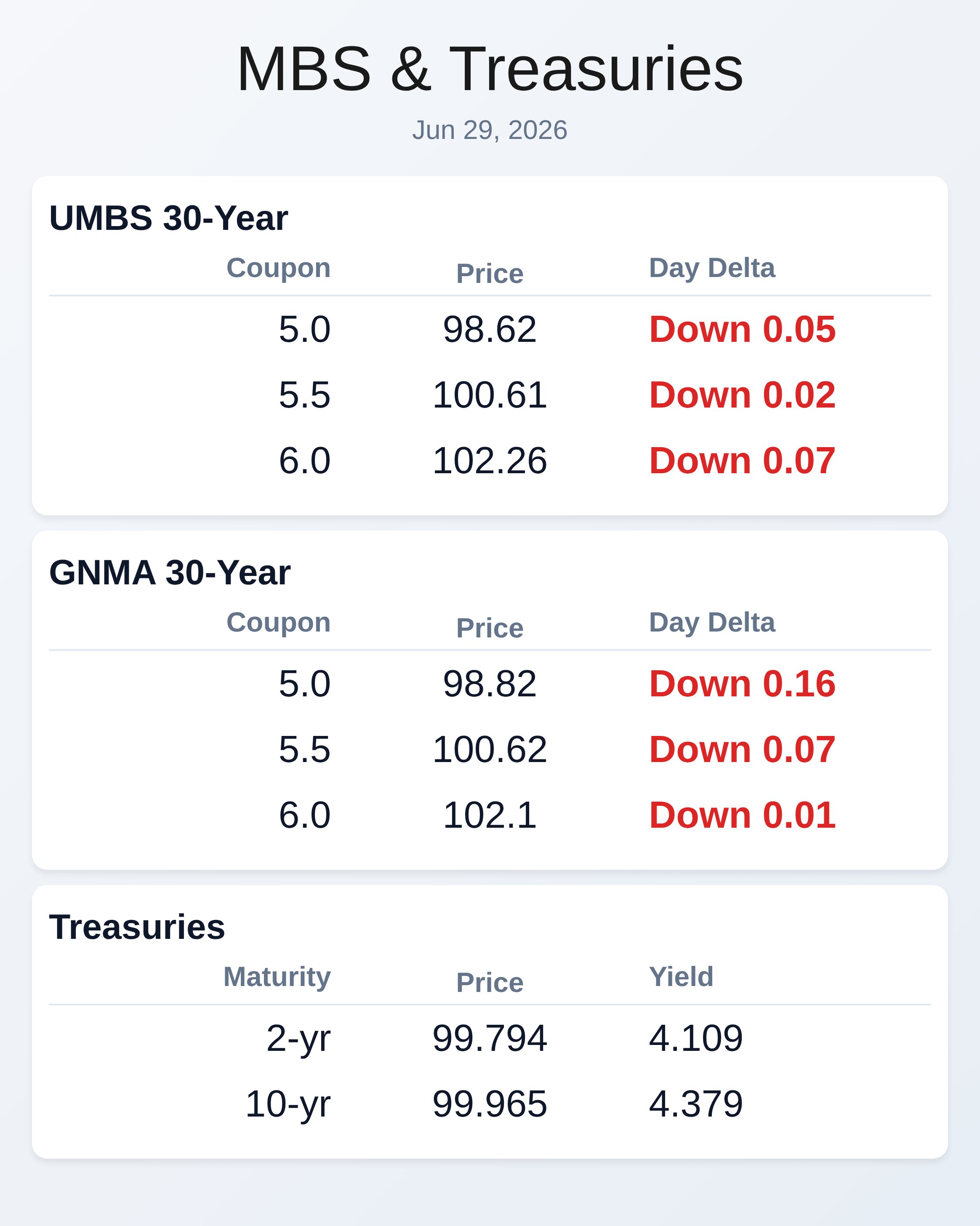

June 29, 2026

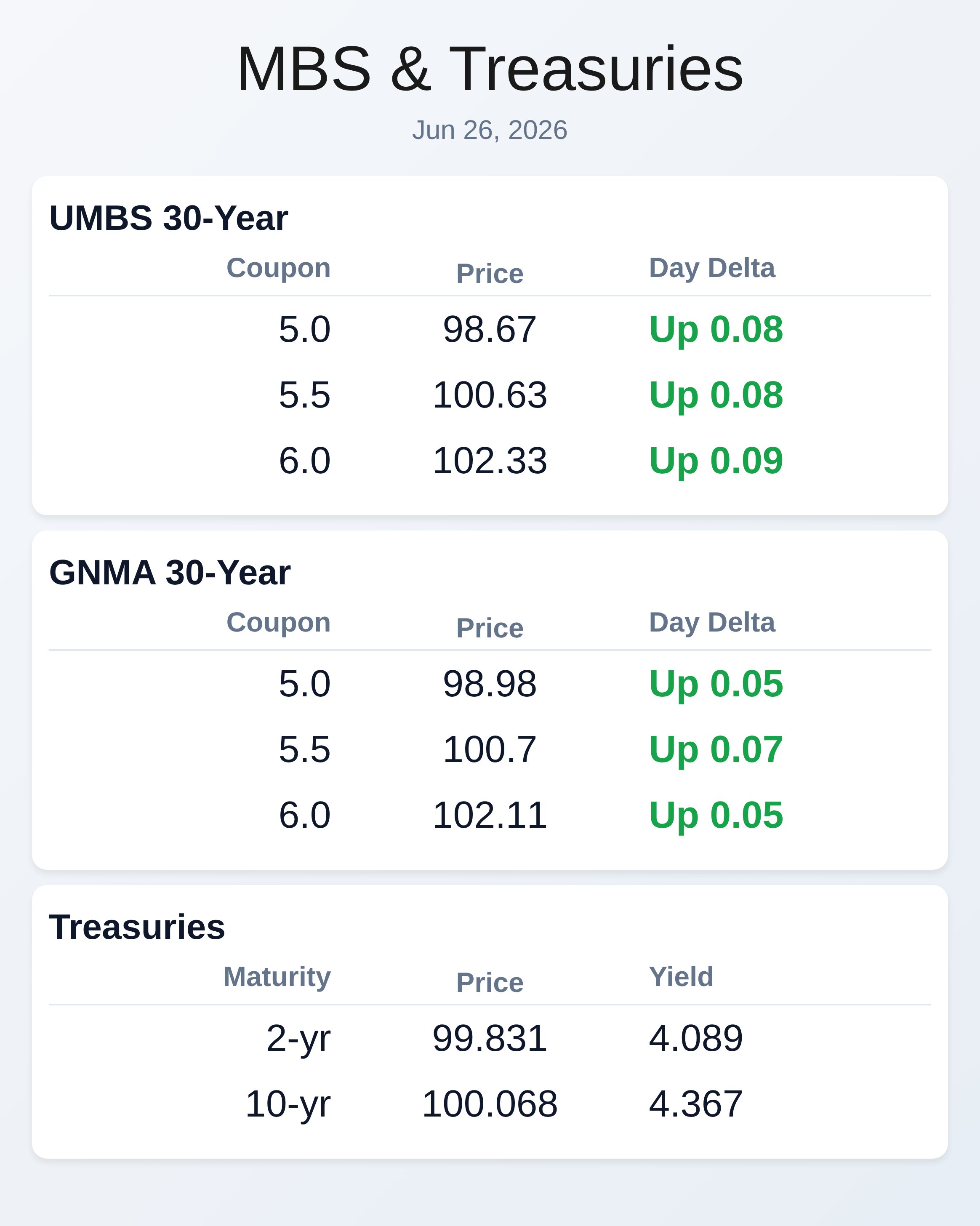

June 26, 2026

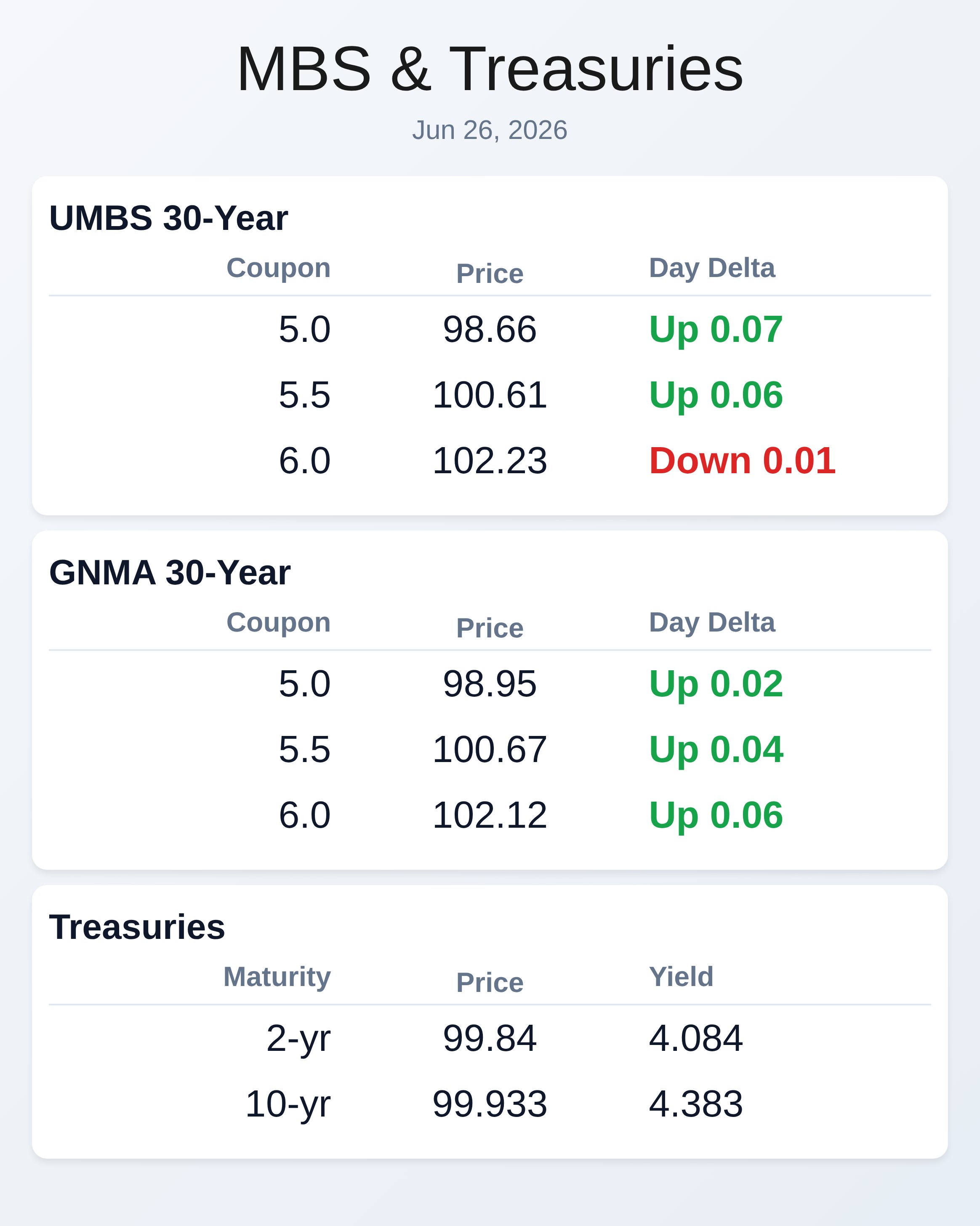

June 26, 2026

RECENT ARTICLES

Traction 1

Post #1 in a mult-part series from the excellent book Traction by Gino Wickman Every Corporation has 6 components. Vision: You must create a compelling vision and be able to communicate it clearly. [...]

What’s up in Mortgage Today – 1.9.23

Monday - January 9, 2023 UMBS up 19 bps early. 10y flat. Stocks extended global gains in risk assets, driven by China’s reopening trade and expectations of slower rate hikes. The dollar weakened [...]

Mortgage Market Week in Review – Week of 1.6.23

Monday - January 2, 2023 Tuesday - January 3, 2023 European bond markets rallied yesterday and again in the overnight session. Reports are showing that European inflation is moderating. This resulted in our [...]

Article Archive