**WTMS Blog Today = What’s up in Mortgage Today (AM) – 06/26/2026**

New home sales collapsed 7.3% in May, marking the lowest pace since January as affordability crises overwhelm buyers and builders alike. The annualized sales rate fell to 580,000 units, well below the 640,000 expected, while inventories spiked to 10.3 months of supply—the highest level since 2009. The West saw the steepest decline at 26.9%, while the South dropped to a seven-year low despite being the nation’s largest homebuilding region.

Median prices edged up to $424,900 even as developers slashed prices and offered mortgage rate buydowns. This inventory glut is forcing builders to pull back on new construction to clear the backlog. Mortgage payments hit a one-year high in May at $2,198 on new purchase loans, up 2.1% from April and rising for three consecutive months.

Affordability collapsed in 33 states as rising rates combined with elevated home prices to push monthly obligations skyward across all loan types. Conventional loan payments jumped to $2,211 while FHA payments surged 2.4% to $1,873. Although current payments remain below last May’s $2,211 peak, the recent three-month trend signals sustained pressure on borrowers and originators facing tighter pipelines.

Rate hold at current levels would continue dampening origination volumes through the summer. Agency MBS prices started Friday sideways with minimal momentum as the economic calendar remains quiet ahead of weekend quarter-end positioning flows. The 10-year Treasury moved down 1.7 basis points overnight but bounced back near yesterday’s close, creating technical uncertainty around the 4.42% resistance level tested this week.

UMBS 5.0 coupons sat at 98.62 with intraday gains modest at +0.02, while GNMA 5.0s traded slightly better at 98.94. The broader market awaits the final University of Michigan Consumer Sentiment reading, expected to be revised higher on lower gasoline prices and strong stock-market gains. Quarter-end rebalancing among portfolio managers could trigger random volatility spikes through next Wednesday.

Buydown mortgages have become a critical tool for survival, now representing $41.7 billion or 1.6% of the Ginnie Mae universe as affordability pressures persist. Concentrated in FHA and VA lending, these loans temporarily reduce borrower rates for one to three years while requiring qualification at the fully indexed payment. Investors value buydowns for prepayment protection during the subsidy period since borrowers have less incentive to refinance, though activity typically accelerates once the buydown expires.

This product segment is likely to remain significant as originators battle higher rate environments and buyer resistance. For lenders, buydowns represent both a competitive necessity and a source of longer-duration cash flow. Fifteen-year UMBS pools continue outperforming their 30-year counterparts despite representing a much smaller market share due to declining refinance activity.

The 30-year UMBS universe has exploded 141% since 2019 to $5.3 trillion, while 15-year issuance contracted sharply after rates rose in 2022. Faster prepayment speeds on 15-year pools reflect borrower quality and curtailment behavior that appeals to investors seeking principal return and duration control. The shrinking supply of 15-year pools combined with favorable borrower profiles creates a diversified investment case that compares favorably in higher-rate environments where cash-in-hand carries premium value.

Forward issuance trends suggest this relative scarcity will persist, supporting relative value. Global markets are struggling to find footing as technology stock weakness spreads across equities while bond markets gain traction. Nasdaq 100 futures fell 1.3% Friday morning following a New York Times report that OpenAI may delay its public offering until 2027.

Investors pulled money from U.S. equities for the first time in three months with record withdrawals from tech, signaling potential rotation away from crowded trades. Oil prices resumed their decline to below $71 per barrel, supporting bond rallies as inflation fears ease.

The dollar held onto year-to-date gains as Federal Reserve Chairman Kevin Warsh signaled commitment to price stability, potentially supporting continued accommodative market sentiment.

**Locking vs Floating**

Rates confirmed a break below the 4.42% technical level Thursday with modest strength, marking the best showing in recent weeks. However, the fragile nature of the breakdown means quarter-end volatility could easily erase gains or push rates higher into next week.

MBS price movements remain the most reliable intraday hedging tool, while longer-term momentum direction tracks the 10-year Treasury yield ceiling-floor band that signals bigger market picture trends.

**Bond Pricing**

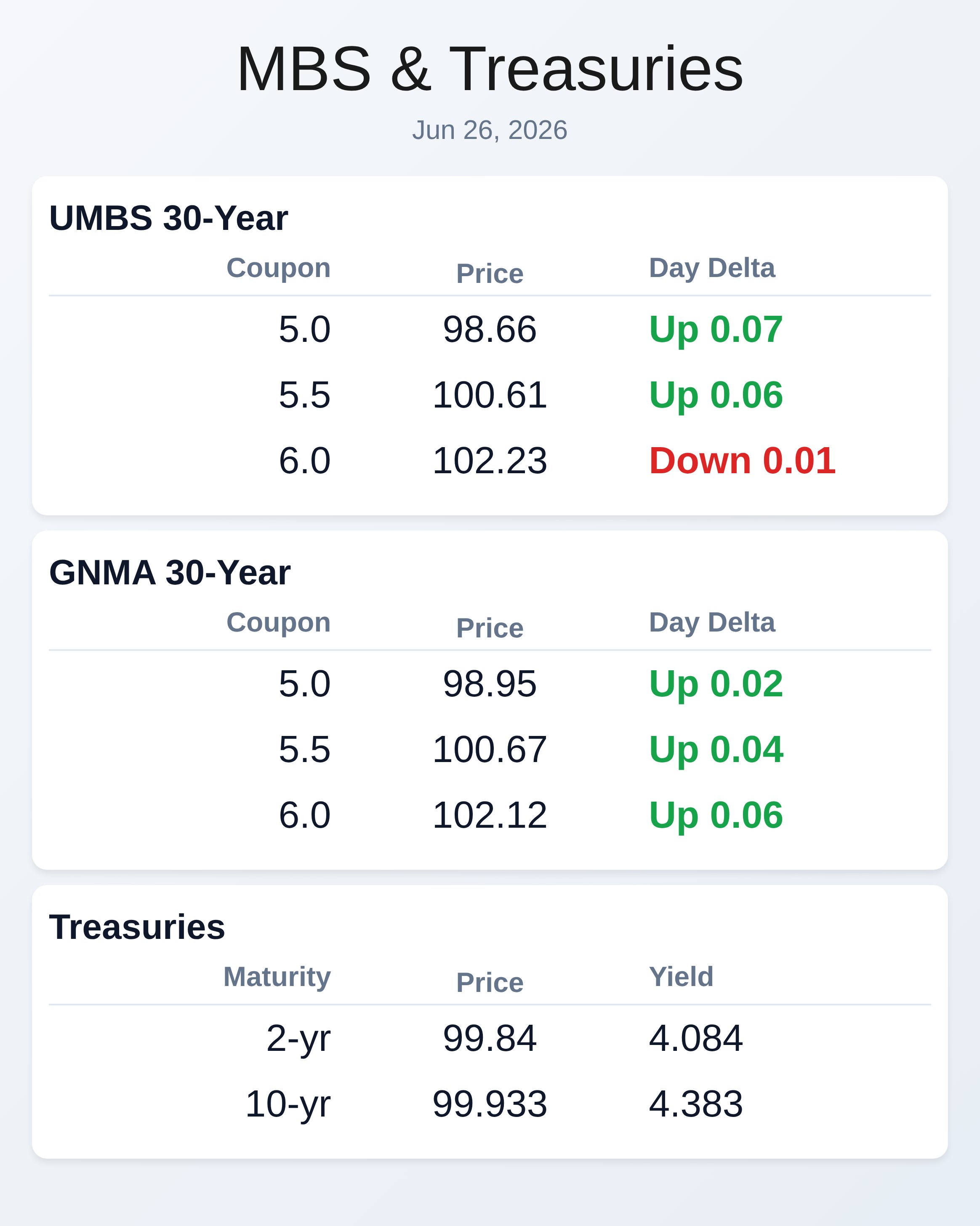

**UMBS 30 yr**

| Coupon | Price | Intra-Day Change |

| 5.0 | 98.66 | 0.07 |

| 5.5 | 100.61 | 0.06 |

| 6.0 | 102.23 | -0.01 |

**GNMA 30 yr**

| Coupon | Price | Intra-Day Change |

| 5.0 | 98.95 | 0.02 |

| 5.5 | 100.67 | 0.04 |

| 6.0 | 102.12 | 0.06 |

**Treasuries**

| Term | Yield | Price | Intra-Day Yield Change |

| 2yr | 4.084 | 99.84 | -0.038 |

| 10yr | 4.383 | 99.933 | -0.008 |

| 30yr | 4.875 | 101.963 | 0.012 |