**WTMS Blog Today = What’s up in Mortgage Today (AM) – 06/25/2026**

Bonds rallied moderately today after the Personal Consumption Expenditures price index arrived exactly as expected, calming inflation concerns that have dominated recent trading. The 10-year Treasury fell 1.2 basis points to 4.375 percent while MBS prices climbed 6 ticks following the benign PCE print, which showed core inflation at 3.4 percent annually and monthly at 0.3 percent. These aligned forecasts suggest the Federal Reserve’s inflation trajectory remains steady despite persistent pressure from energy-related costs and broader price pressures.

Mortgage originators found modest tailwinds this morning as lender pricing had not fully caught up to yesterday’s bond rally, creating a small cushion for rate locks. The market remains cautious, however, waiting for a second close below the key 4.42 percent technical level in 10-year yields before declaring a decisive trend shift. Economic data released Thursday morning delivered a mixed picture of labor demand and consumer resilience that will shape mortgage strategy through the remainder of the quarter.

Initial jobless claims fell to 215,000 from 226,000 in the prior week, beating expectations of 225,000 and signaling tighter labor markets heading into summer. Personal income surged 0.7 percent month-over-month, outpacing the 0.4 percent forecast, while personal spending accelerated 0.7 percent against expectations of just 0.3 percent. Durable goods orders declined 4.5 percent as expected, suggesting manufacturing caution, though the broader economy expanded at an annualized 2.1 percent in Q1, beating prior estimates of 1.6 percent.

Origination teams should note that strong consumer spending paired with moderate inflation keeps rate expectations anchored near current levels rather than forcing sudden repricing. New home sales tumbled 7.3 percent month-over-month in May to an annualized rate of 580,000 units, falling well below expectations of 627,000 and marking the second-lowest sales pace in the past twelve months. Affordability constraints linked to persistent mortgage rates drove the decline, with the West region experiencing the most acute pullback as higher-priced markets face buyer resistance.

Even the South—traditionally the nation’s most resilient homebuilding region—showed meaningful weakness, suggesting pricing sensitivity is spreading beyond coastal markets. Year-over-year sales fell 6.8 percent, underscoring the cumulative headwind from elevated rates and limited inventory. For mortgage lenders, this data reinforces that rate-conscious borrowers are delaying or postponing purchases, likely transferring demand to refinance and home equity products.

The Federal Reserve’s latest stress test validated the resilience of the banking system, with all 32 large banks maintaining capital above regulatory minimums even under an extreme recession scenario featuring 10 percent unemployment, 30 percent home price declines, and 39 percent commercial real estate losses. Banks would absorb over $708 billion in losses across credit cards and commercial real estate yet retain aggregate capital ratios declining only 1.6 percentage points. This structural strength means correspondent lenders and major portfolio managers remain well-positioned to fund mortgage originations without external capital constraints.

The findings provide some assurance that mortgage funding will remain available through any economic stress, though competitive conditions may tighten. Originators can reference this stability when reassuring borrowers and investors about market liquidity. A Treasury auction of $70 billion in 5-year notes received lukewarm reception Wednesday, with investors demanding slightly higher yields than the market expected, forcing dealers to absorb an outsized share.

Although the sale “tailed,” the broader Treasury market barely reacted, suggesting dealers viewed the outcome as disappointing but not alarming for the long-term outlook. Shorter-dated Treasuries remain near 2025 highs due to lingering energy-inflation sensitivity, while longer-term bonds extended their rally as oil prices fell and demand for duration strengthened. A $44 billion auction of 7-year notes is scheduled for later today, and market observers will watch closely for any signs of persistent auction weakness.

The key takeaway for origination: secondary market demand for government debt remains adequate, stabilizing funding costs for GSE mortgages. Borrower retention strategies are increasingly shifting from broad recapture percentages toward targeted, analytics-driven outreach that identifies homeowners most likely to benefit from a new product or rate reset. Many lenders report impressive headline recapture figures without standardizing definitions—some count only rate-and-term refinances while others include streamlined government products—rendering industry comparisons nearly meaningless.

Servicers now leverage richer borrower data, updated tax and insurance information, and behavioral analytics to distinguish between borrowers worth pursuing versus those better left alone. This evolving sophistication means retention success no longer tracks with call volume but instead reflects the quality of pre-outreach decision-making. Originators seeking competitive advantage should audit whether their recapture efforts emphasize contact quantity or borrower fit, as the latter increasingly determines market share gains.

**Locking vs Floating**

Lenders face a measured backdrop for lock-versus-float decisions given modest tailwinds from pricing that hasn’t caught up to yesterday’s bond rally coupled with a potential technical breakdown if 10-year yields close below 4.42 percent. The risk-on environment that allowed intraday bond gains reflects rebalancing between stocks and bonds rather than a fundamental shift in Fed policy expectations. Building a small cushion for rate locks makes sense until the market confirms the technical level breaks on a second consecutive close.

**Today’s Events**

Jobless Claims (Jun 20): 215,000 versus 225,000 forecast

Personal Income (May, m/m): 0.7% versus 0.4% forecast

Personal Spending (May, m/m): 0.7% versus 0.3% forecast

Core PCE (May, m/m): 0.3% versus 0.3% forecast (in line)

Core PCE (May, y/y): 3.4% versus 3.4% forecast (in line)

PCE (May, y/y): 4.1% versus 4.1% forecast (in line)

Durable Goods (May): -4.5% versus -4.5% forecast (in line)

GDP Q1: 2.1% versus 1.6% forecast

Treasury Auction (7-year, $44 billion): Scheduled for 1:00 PM ET

**Bond Pricing**

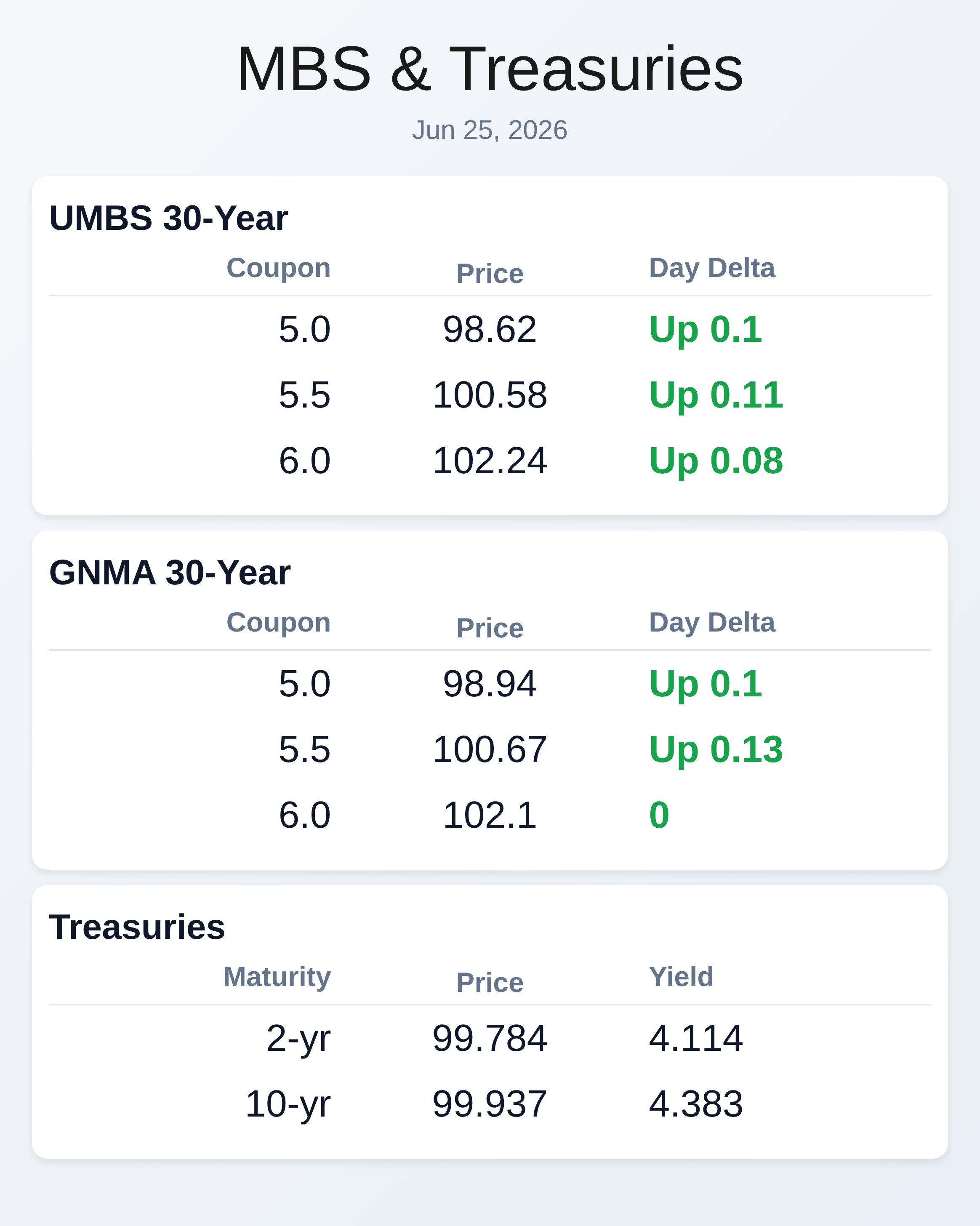

**UMBS 30 yr**

| Coupon | Price | Intra-Day Change |

| 5.0 | 98.62 | 0.1 |

| 5.5 | 100.58 | 0.11 |

| 6.0 | 102.24 | 0.08 |

**GNMA 30 yr**

| Coupon | Price | Intra-Day Change |

| 5.0 | 98.94 | 0.1 |

| 5.5 | 100.67 | 0.13 |

| 6.0 | 102.1 | 0 |

**Treasuries**

| Term | Yield | Price | Intra-Day Yield Change |

| 2 yr | 4.114 | 99.784 | -0.034 |

| 3 yr | 4.116 | 100.025 | -0.03 |

| 5 yr | 4.157 | 99.857 | -0.022 |

| 7 yr | 4.256 | 99.963 | -0.02 |

| 10 yr | 4.383 | 99.937 | -0.004 |

| 30 yr | 4.84 | 102.525 | -0.008 |