**WTMS Blog Today = What’s up in Mortgage Today (AM) – 06/23/2026**

Tech stocks tanked overnight as Wall Street questions whether AI spending hype is justified, dragging down equity futures and shifting focus back to fixed income. The Nasdaq 100 futures fell 2.9% with semiconductor giants like SK Hynix and Samsung sliding over 10%, while the broader selloff pulled S&P 500 contracts down 1.3%. This pullback follows a spectacular first-half rally that left valuations stretched and retail investors nervous.

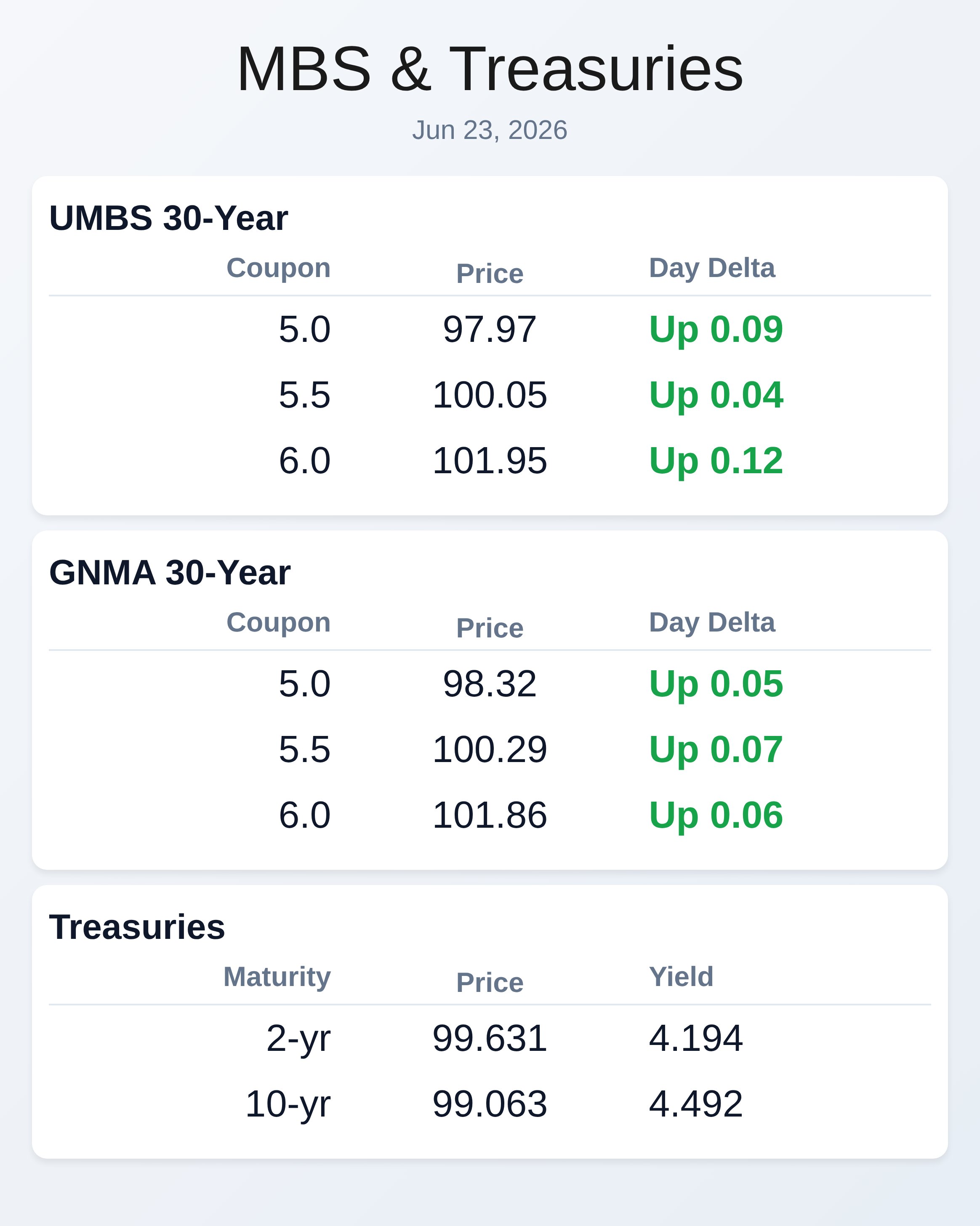

Meanwhile, Treasuries found relief as traders dialed back rate-hike expectations, with the 10-year yield dropping 2.2 basis points to 4.49%. Agency MBS prices ticked higher on the equity weakness, posting gains of roughly an eighth of a point. The U.S.

Senate passed the bipartisan 21st Century ROAD to Housing Act with strong momentum toward House passage later this week, aiming to lower housing costs and restrict institutional investors from outbidding families. The legislation, which pairs supply-side reforms with restrictions on Wall Street home buying, represents a rare moment of agreement in Congress driven partly by midterm election concerns. JPMorganChase released a policy brief showing how innovative construction methods including modular and manufactured homes can slash building costs by 20-30% and timelines by 30-50%, addressing the affordability crisis.

Key state examples like Maryland, Colorado, and Texas are testing zoning reforms, building code changes, and permitting streamlining to enable faster housing development. For mortgage lenders, this legislative momentum signals potential demand shifts as supply increases and affordability improves. A notable disconnect emerged in bond markets as the 10-year Treasury weakened while related assets diverged, reinforcing a bearish technical picture despite modest intraday gains.

The bond market remains unwilling to break through key technical support floors, keeping the “bearish until proven bullish” narrative alive for lock-and-float traders. Heavy stock selling is providing some support to MBS and Treasuries, but this relief appears fragile given the geopolitical backdrop and rate-hike concerns. Treasury auctions today include $69 billion in 2-year notes, which will test demand after recent auctions showed notable tailing.

The economic calendar features ADP employment data at 8:15 AM and preliminary June PMIs at 9:45 AM, though neither is expected to move rates significantly. The AI adoption gap is widening rapidly across the mortgage industry, with most lenders still in pilot phase while a select few are operationalizing AI at scale. According to MISMO leadership, the difference between workflow acceleration (doing tasks faster) and operational intelligence (making better decisions at scale) will separate winners from losers over the next three to five years.

Lenders experimenting with tools are missing the bigger opportunity: redesigning business processes around AI capabilities. This distinction matters for competitive positioning as the industry evolves beyond proof-of-concept stages. For originators and servicers, the message is clear—moving from testing to implementation determines survival.

Iran sanctions easing through a temporary U.S. Treasury waiver created initial upward pressure on bond yields, though actual oil market impact remains modest with Brent trading around $77.30 per barrel. The geopolitical uncertainty from negotiations between the U.S.

and Iran in Switzerland created volatility early in the week but has since settled as traders focus on economic data and Fed rhetoric. With Chair Kevin Warsh’s recent hawkish commentary on inflation fighting, markets shifted expectations upward on rate hikes, pressuring long-duration assets like technology stocks and extending MBS duration risk. The Fed’s dot plot projections added to rate-hike concerns despite the central bank cutting 175 basis points since mid-2024.

Mortgage originators should monitor next week’s PCE inflation report closely, as it represents the Fed’s preferred inflation gauge. Market positioning favors mid-stack MBS coupons over higher-duration securities as investors adopt a “wait-and-see” stance toward rate decisions and geopolitical news. Despite MBS appearing attractive relative to investment-grade corporate bonds on a relative value basis, participants remain cautious given double uncertainty from Fed policy and global tensions.

The bull-steepening Treasury curve reflects the equity selloff and reduced rate-hike expectations, providing some relief for mortgage servicers and portfolio managers. Mortgage lender hiring remains robust with firms like EPM experiencing record growth and actively recruiting underwriters, account managers, and entire teams. Verification and employment validation technology continues advancing, with platforms like Truework and Kind Lending offering cost savings of 20-50% on income documentation.

**Locking vs Floating**

Bond weakness persists despite modest intraday strength as the market refuses to challenge key technical support levels. Early-week momentum turned bearish as traders reassessed Fed rate-hike odds and digested hawkish Chair Warsh commentary. Lock strategy remains prudent until bond technicals prove strength, while floaters expose borrowers to lingering geopolitical and inflation risks.

**Today’s Events**

8:15 AM — ADP Employment Change (June preliminary)

9:45 AM — Markit Purchasing Managers’ Indices (June preliminary)

11:30 AM — 6-Week Treasury Bill Auction

1:00 PM — 2-Year Treasury Note Auction ($69 billion)

**Bond Pricing**

**UMBS 30 yr**

| Coupon | Price | Intra-Day Change |

**GNMA 30 yr**

| Coupon | Price | Intra-Day Change |

**Treasuries**

| Term | Yield | Price | Intra-Day Yield Change |