**WTMS Blog Today = What’s up in Mortgage Today (AM) – 06/16/2026**

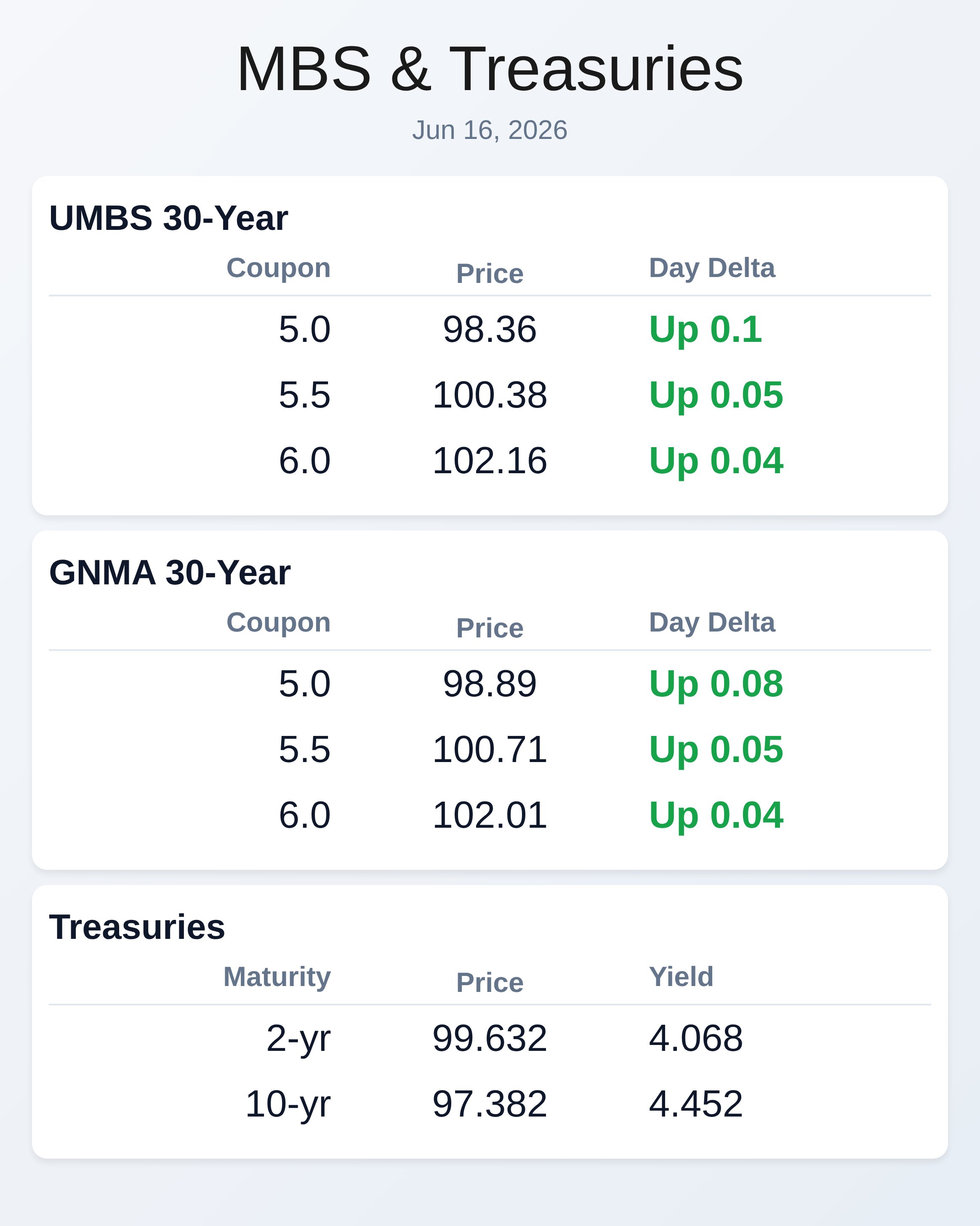

Markets rallied overnight on Iran peace deal optimism as the U.S. and Iran agreed to reopen the Strait of Hormuz and begin nuclear negotiations, sending oil to three-month lows and reshaping investor expectations around inflation. MBS gained six ticks with UMBS 5.0 coupons reaching 98.36, while GNMA 5.5 coupons hit 100.71 as Treasuries rallied across the curve.

The 10-year Treasury yield fell four basis points to 4.438 percent, driven by expectations that lower energy costs will ease inflation pressures. Geopolitical developments, not economic data, are now the primary driver of near-term bond performance, according to capital markets strategists. This momentum could persist through Friday’s formal Iran agreement signing, though some uncertainty remains about deal implementation.

May housing data came in weak across the board, signaling continued headwinds for the construction sector and residential mortgage demand. Housing starts collapsed 15.4 percent month-over-month to 1.177 million annualized, missing the 1.430 million forecast and falling well below the 1.370 to 1.497 million economist range. Building permits declined 0.7 percent to 1.413 million, essentially in line with expectations but reflecting tepid builder confidence.

Completions dropped to 1.313 million from 1.429 million the prior month, suggesting a slowdown in pipeline activity. Higher mortgage rates and lingering economic uncertainty continue to weigh on housing production, keeping pressure on originator volumes. Import price inflation accelerated to 1.9 percent month-over-month in May, meeting analyst expectations and matching the prior month’s reading, while export prices unexpectedly fell to 1.3 percent from 3.3 percent previously.

ADP employment growth decelerated sharply to 25.5 thousand last week, falling well below the prior month’s 29 thousand gain and suggesting labor market momentum is slowing. These softer economic readings reinforce the market narrative that the Fed will pause rate hikes and remain patient, even as inflation concerns linger. Investors are now awaiting Kevin Warsh’s first Federal Reserve meeting on Wednesday, where policymakers are expected to hold rates steady.

The Fed’s updated economic projections will likely signal higher inflation expectations and a slight shift toward the possibility of future rate hikes, though messaging should remain dovish.

**Locking vs Floating**

Lock or float decisions remain balanced at this moment, with meaningful uncertainties surrounding the Iran peace deal execution hanging over markets through Friday’s formal agreement signing. The downside risk is that the deal falls apart, pushing yields higher and hurting borrowers who waited; the upside is that a finalized agreement could push yields even lower as energy inflation expectations decline further.

Current positioning suggests defending against a move above Friday’s highs in the 10-year yield, with particular caution needed if yields approach 4.42 percent and bounce hard. For now, neither aggressive locking nor floating has a clear edge given geopolitical headline risk and thin economic data.

**Today’s Events**

ADP Employment Change Weekly: 25.5K vs.

prior 29K

Building Permits (May): 1.413M vs. forecast 1.42M, prior 1.423M

Housing Starts (May): 1.177M vs. forecast 1.43M, prior 1.465M

Import Prices (May): 1.9% vs.

forecast 1.0%, prior 1.9%

Export Prices (May): 1.3% vs. prior 3.3%

20-Year Treasury Bond Auction: $13 billion

**Bond Pricing**

**UMBS 30 yr**

| Coupon | Price | Intra-Day Change |

| 5.0 | 98.36 | 0.10 |

| 5.5 | 100.38 | 0.05 |

| 6.0 | 102.16 | 0.04 |

**GNMA 30 yr**

| Coupon | Price | Intra-Day Change |

| 5.0 | 98.89 | 0.08 |

| 5.5 | 100.71 | 0.05 |

| 6.0 | 102.01 | 0.04 |

**Treasuries**

| Term | Yield | Price | Intra-Day Yield Change |

| 2 yr | 4.068 | 99.632 | -0.001 |

| 3 yr | 4.109 | 98.298 | -0.023 |

| 5 yr | 4.177 | 98.652 | -0.014 |

| 7 yr | 4.305 | 99.672 | -0.018 |

| 10 yr | 4.452 | 97.382 | -0.021 |

| 30 yr | 4.951 | 96.87 | -0.023 |