**WTMS Blog Today = What’s up in Mortgage Today (AM) – 06/15/2026**

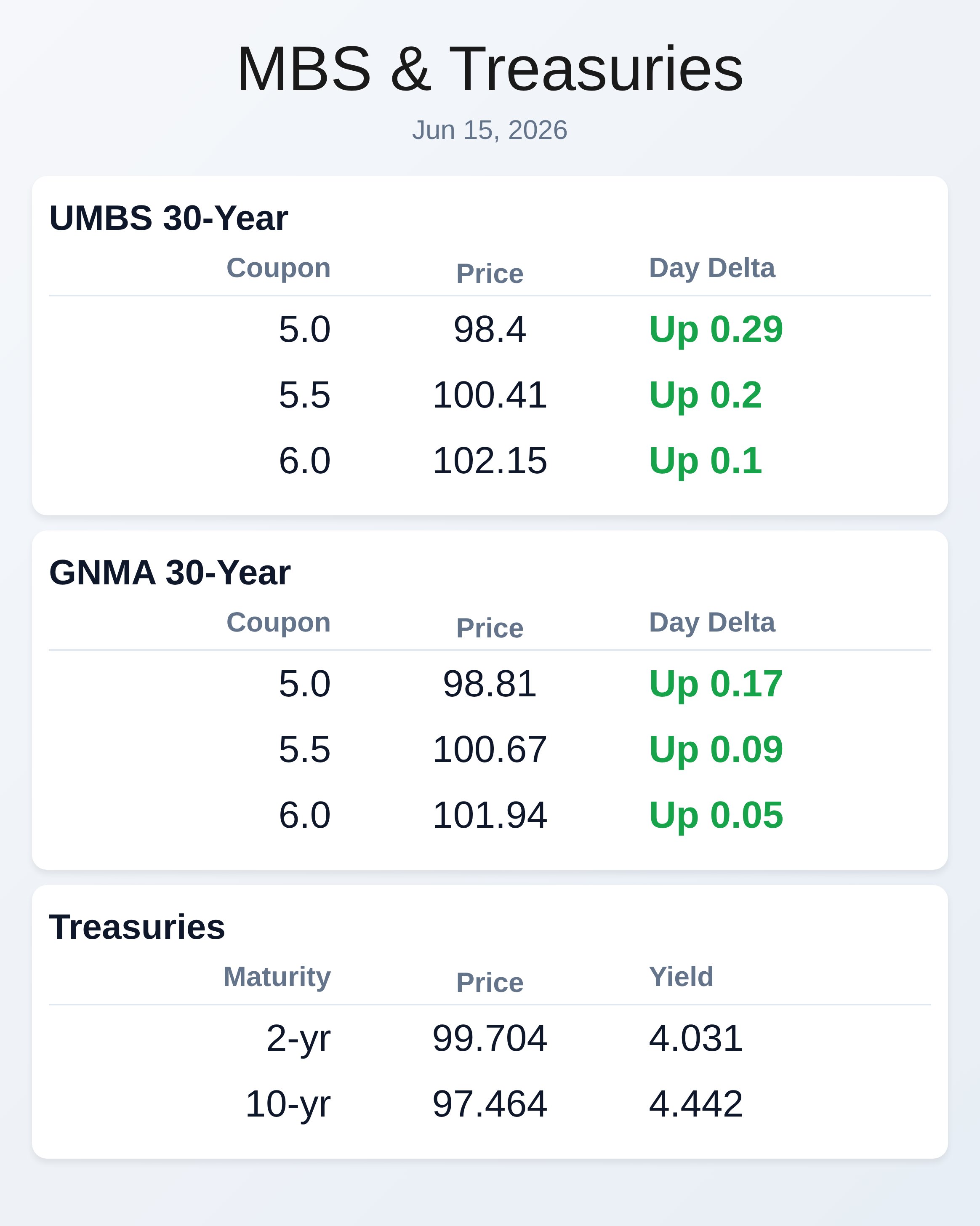

Peace deal news sent MBS securities sharply higher and Treasury yields tumbling by 3 to 6 basis points this morning as markets priced in falling energy costs. The U.S.-Iran agreement to reopen the Strait of Hormuz signals relief from inflation pressure, with oil dropping 5% to near three-month lows and the 10-year Treasury sliding to 4.44%. UMBS 5.0 coupons rallied nearly 0.30 points while 5.5 coupons gained 0.22 points, indicating strong appetite for mortgage securities as Fed rate-hike expectations dial back.

GNMA securities followed suit with similar strength across coupons. Market analysts expect the Fed’s Wednesday decision will hold rates steady at 3.5% to 3.75%, with momentum now favoring patience over tightening. Weaker economic data reinforced the dovish shift overnight.

The June Empire State Manufacturing index collapsed to 5.7, far below the 14.0 forecast and a dramatic drop from May’s 19.6 reading. Industrial production in May came in at 0.1%, missing expectations of 0.3% and suggesting cooling economic momentum. New orders tumbled to 3.5 versus 22.7 prior, signaling a sharp pullback in manufacturing confidence.

These misses, combined with softening consumer expectations, give the Fed cover to remain patient despite elevated inflation readings that would normally trigger tightening. For mortgage originators, this means rate environment is likely stabilizing, though refinance activity remains muted given current 4.4% to 4.5% levels still elevated versus borrower expectations. Fed Chairman Kevin Warsh faces his first rate decision this week as markets obsess over whether the Iran deal sticks or unravels.

Traders are pricing only a 70% to 75% chance of a December rate hike, down from 80% on Friday, reflecting genuine shift in expectations. The curve is steepening with shorter maturities outperforming longer ones, a classic sign investors see lower rates ahead. Treasury two-year yields fell as much as 7 basis points to 4.01%, while 30-year yields sank to 4.92%, their lowest since May 7.

The Strait of Hormuz reopens Friday, but Iran has only committed to 60 days of free passage, creating tail risk if negotiations break down. For mortgage sellers locking long-term production, this window of lower rates presents fleeting opportunity before deal uncertainty resurfaces. AI-powered automation is reshaping mortgage underwriting workflows as startups race to compress document review timelines.

Copperlane, a $4.1 million seed-funded startup, autonomously scans thousands of pages of borrower documents, identifies suspicious deposits, flags underwriting conditions, and drafts explanatory letters—all before human review. The company, founded by two 21-year-olds from Princeton and Penn, targets compression of four-plus hours of per-file work down to minutes. Industry conversations are gravitating toward affordability, AI adoption, and regulatory change as lenders chase sustainable growth models.

Mortgage originators should monitor AI underwriting tools closely, as early adopters gain processing speed advantages in volume-constrained markets. Two Harbors allowed UWM’s direct negotiation window to expire without a revised bid, leaving the CrossCountry merger on track for a June 23 shareholder vote. UWM CEO Mat Ishbia discussed structural changes on a June 11 video call but declined written proposals, signaling either confidence in CrossCountry terms or strategic retreat.

The inability to force a competitive bid means UWM stock remains near all-time lows at $2.38, reflecting investor skepticism about standalone prospects. For mortgage dealers and service providers, the CrossCountry consolidation path suggests continued industry concentration among larger platforms. Regulatory approvals stand at 46 of 53, with voting imminent.

Consumer comfort with AI-driven mortgage decisions has crossed a psychological threshold, with 53% of homebuyers willing to complete purchases without human involvement according to Veterans United. Nearly 90% of buyers trust AI for financial advice and 76% would let algorithms shop lenders, though only 25% feel very comfortable with fully automated closings. Veterans show higher AI trust at 77% versus 59% for civilian buyers, signaling generational shifts in borrower behavior.

The caveat remains critical: buyers want AI handling research and paperwork but demand humans for actual decisions. This bifurcation reshapes loan officer roles from processors toward hybrid advisors managing AI-assisted workflows rather than performing repetitive document work.

**Locking vs Floating**

Economic data deterioration and geopolitical de-escalation have shifted the rate trajectory downward, favoring float strategies for new production locks.

Near-term economic momentum appears genuinely softening with manufacturing surveys and production data disappointing consensus, reducing inflation persistence risk and supporting Fed patience. The Iran deal, if sustained through Friday signing, removes a material upside risk to energy costs that would otherwise keep rate yields higher. Lock economics improve for borrowers if current uncertainty persists into next week, but floating offers optionality if deal negotiations falter or inflation surprises return.

Originators with existing commitments should monitor Fed statement language Wednesday for any hints on tightening bias—removal of easing language would mark critical pivot.

**Today’s Events**

NY Fed Manufacturing (Jun): 5.70 vs 14.0 forecast, 19.6 prior

Industrial Production (May): 0.1% vs 0.3% forecast, 0.7% prior

NAHB Housing Market Index (Jun): Coming later today

**Bond Pricing**

**UMBS 30 yr**

| Coupon | Price | Intra-Day Change |

**GNMA 30 yr**

| Coupon | Price | Intra-Day Change |

**Treasuries**

| Term | Yield | Price | Intra-Day Yield Change |

| 2 yr | 4.031 | 99.704 | -0.056 |

| 3 yr | 4.079 | 98.381 | -0.055 |

| 5 yr | 4.157 | 98.738 | -0.051 |

| 7 yr | 4.29 | 99.759 | -0.041 |

| 10 yr | 4.442 | 97.464 | -0.043 |

| 30 yr | 4.945 | 96.961 | -0.026 |