**WTMS Blog Today = What’s up in Mortgage Today (AM) – 06/11/2026**

War headlines and producer inflation sent mortgage markets into a tailspin this morning before bonds recovered most losses by mid-morning. May’s producer prices rose 1.1% month-over-month, well above the 0.7% forecast, driven largely by energy costs tied to escalating Iran tensions. Trump’s comments about attacking Kharg Island oil infrastructure rattled traders moments before the data hit, amplifying the initial selloff in both stocks and bonds.

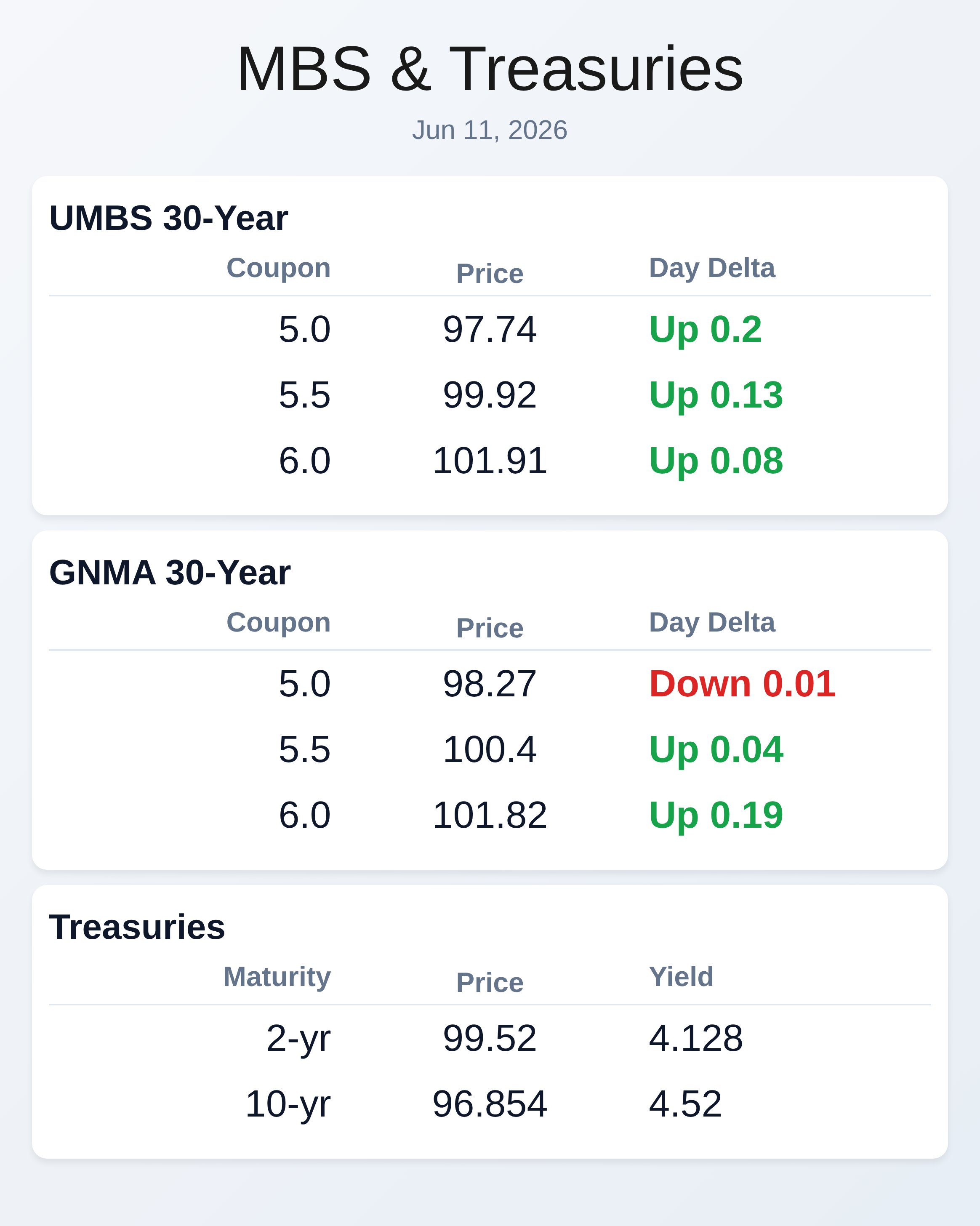

Core PPI came in softer at 0.4% versus 0.5% expected, suggesting energy remains the primary inflation culprit. Markets ultimately interpreted the data as manageable if geopolitical tensions ease. UMBS mortgage-backed securities stabilized after touching intra-day lows, with the 5.0 coupon climbing 0.15 points by late morning.

GNMA securities showed more resilience, with the 6.0 coupon gaining 0.19 points even as the broader market digested inflation concerns. Agency MBS prices found footing six minutes after the PPI release, signaling traders believe elevated wholesale prices could be temporary if oil supplies normalize. The bid-ask spreads tightened as confidence returned, though volatility remained elevated throughout the session.

The 10-year Treasury yield fell 3.5 basis points overnight to 4.517% before climbing back near 4.52% by mid-session. The European Central Bank’s first rate hike since 2023, raising its key rate to 2.25%, added pressure to global bond markets early but failed to derail the Treasury recovery. Jobless claims printed at 229,000 versus a 219,000 forecast, sitting between prior weeks’ readings and suggesting labor markets remain tight.

A $22 billion 30-year Treasury bond auction was scheduled for later in the day, with market participation dependent on how traders view inflation trajectory.

**Locking vs Floating**

Risk-tolerant borrowers should continue using an overhead lock trigger near 4.57%, as bonds have shown evidence of stabilizing after last week’s aggressive selling. Risk-averse clients still lack sufficient support levels to justify a more neutral floating stance.

The resilience in mortgage prices despite inflation surprises suggests the market believes these shocks are energy-driven and potentially transitory.

**Today’s Events**

Continued Claims (May)/30: 1,795K vs 1,780K forecast, 1,777K prior

Core PPI m/m (May): 0.4% vs 0.5% forecast, 1% prior

Core PPI y/y (May): 4.9% vs 5.4% forecast, 5.2% prior

Jobless Claims (Jun)/06: 229K vs 219K forecast, 225K prior

PPI m/m (May): 1.1% vs 0.7% forecast, 1.4% prior

PPI y/y (May): 6.5% vs 6.4% forecast, 6% prior

**Bond Pricing**

**UMBS 30 yr**

| Coupon | Price | Intra-Day Change |

**GNMA 30 yr**

| Coupon | Price | Intra-Day Change |

**Treasuries**

| Term | Yield | Price | Intra-Day Yield Change |