**WTMS Blog Today = What’s up in Mortgage Today (AM) – 06/09/2026**

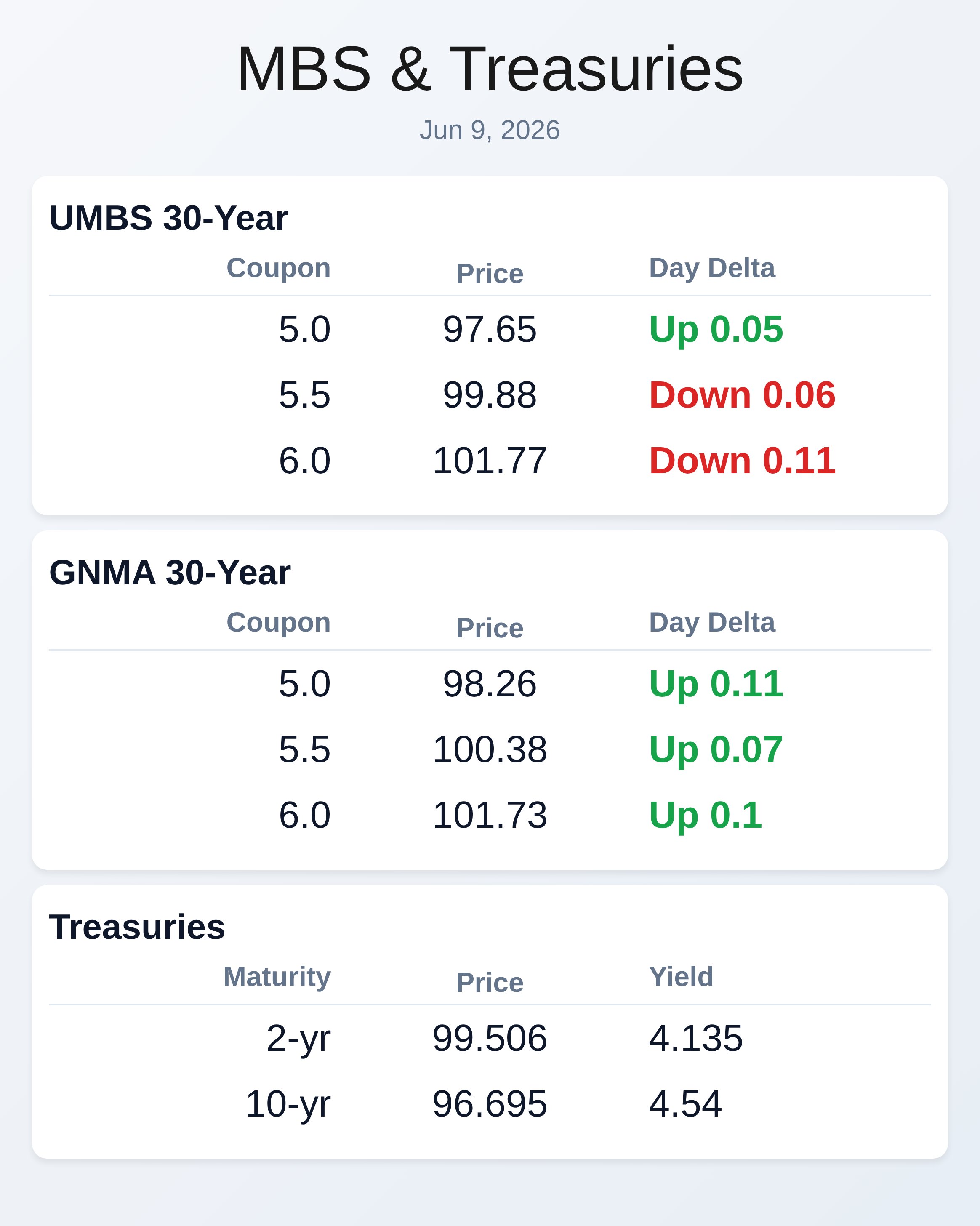

Bonds faded into the afternoon despite oil prices recovering, leaving mortgage originators watching mixed signals from Treasury yields that dipped 2 basis points to 4.54 percent on softer equities and reduced Fed rate-hike expectations. UMBS 30-year 5.0 coupons held steady at 97.65 with intraday gains of 5 basis points, while GNMA 30-year securities showed stronger performance with the 5.0 coupon climbing 11 basis points to 98.26. The broader market wrestled with conflicting forces: tech stocks rebounded on artificial intelligence optimism, oil slid 2.1 percent to $89.39 on Middle East de-escalation, and the dollar faced its biggest two-day retreat in a month.

Mortgage spreads remain defensive after last week’s strong jobs beat that triggered rate volatility, and traders are cautious ahead of Wednesday’s inflation data and mid-June Fed decisions. The industry’s longer-term outlook shows stabilization, with first-quarter profitability marking the longest positive streak since 2021–22. Weak employment data arrived ahead of schedule this morning, with ADP employment change clocking just 29,000 jobs versus the prior week’s 35,750 and signaling softer labor demand than recent trends suggested.

NFIB Business Optimism declined to 95.3 from 96.0 expected and 95.9 previously, suggesting small business confidence is eroding as hiring pressures ease. The U.S. trade deficit narrowed to $55.9 billion in April as exports accelerated at 2.6 percent while imports rose just 2 percent, beating forecasts and pointing to healthier demand dynamics abroad.

These three datapoints together paint a portrait of cooling but resilient growth that favors rate stability rather than aggressive Fed tightening. For mortgage sellers, softer employment and reduced business confidence could translate into slower application volume in the coming weeks. Mortgage market profitability has stabilized on the back of modest refinancing activity and origination discipline across most lenders, with three consecutive quarters of positive earnings marking a psychological turning point after years of contraction.

Refinance share has already faded sharply from its February peak, and refi-driven MBS issuance has retreated to its lowest level since November, signaling that the brief rate-cut rally has exhausted itself. Employment across the mortgage sector has stopped contracting, which signals the industry’s painful right-sizing phase is largely behind it. Housing inventory remains below historical norms and affordability sits near multi-decade lows, yet the industry is transitioning from recovery mode into normalization—constrained growth but no longer in crisis.

Originators should prepare for slower but steadier demand as the market finds its equilibrium. Lenders and brokers are doubling down on technology and operational excellence as competition for qualified borrowers intensifies and borrower retention moves center stage. Inside Real Estate’s new BoldTrail lending-lead platform is generating buzz by connecting lenders directly with borrowers actively seeking both financing and real estate agent partnerships, with some lenders reporting qualified applications within the first week.

Class Valuation’s CVUE underwriting platform is reducing appraisal repurchase risk by assuming liability and cutting turn time by two to three days per file, saving lenders roughly $100 per file. AI-driven verification and compliance tools like Truework are cutting verification costs by up to 50 percent while improving accuracy and reducing manual back-and-forth between loan officers and underwriters. Down payment assistance programs are becoming loan closers: Click n’ Close lowered its SmartBuy second-lien rate to 7.99 percent, directly addressing affordability and borrower purchasing power.

The fastest-growing lenders are not working harder—they are working smarter through data, automation, and systems that keep them present with borrowers at every financial inflection point. Industry leadership and employment turnover continued this week with FHA Commissioner Frank Cassidy resigning after his temporary leave in April to return to private-sector deal work, citing excitement to support the Trump administration’s housing agenda from outside government. Maryland mortgage veteran Mike Sterner, former President and CEO of Susquehanna Mortgage and founder of Mortgage Department Services, passed away after battling cancer; Sterner was a 2003 MMBBA Mortgage Banker of the Year and 2021 Hall of Fame inductee.

The Chrisman Job Board remains active with new openings for account executives across the West Coast and emerging opportunities in technology and operations roles, reflecting the industry’s ongoing rebalancing. STRATMOR Group’s latest capital markets analysis indicates pricing trends remain supportive for borrowers willing to shop and compare, while broader mortgage intelligence systems are becoming table-stakes for competitive lenders. These transitions underscore the industry’s maturation and the premium placed on talent, systems, and strategic positioning in a normalized lending environment.

A critical question emerged this week from MISMO’s President Brian Vieaux: do borrowers want a lower rate or a better house? In the 2020–21 boom, historically low rates masked brutal inventory constraints, forcing buyers into bidding wars and appraisal gap negotiations with limited choice. Today, inventory is gradually improving, rates are higher, but borrowers have negotiating power and can actually choose their homes rather than accept whatever they can get.

Most effective mortgage advisors have shifted their conversation opener from rates to goals, understanding that while mortgages can be refinanced, the home itself is a much more durable life decision. This philosophical reorientation—from rate focus to outcome focus—matters profoundly for loan officer retention, borrower satisfaction, and long-term pipeline health in a normalized market where choice has returned.

**Locking vs Floating**

Defend your rate locks in this volatile environment until you see clearer evidence of support in the bond market.

After last week’s strong jobs print drove rates higher, short-term momentum has stabilized but oil price recovery did not translate into the closer bond market closes you might have expected. Remain cautious and wait for better technical evidence of support before shifting back to a neutral stance.

**Today’s Events**

NFIB Business Optimism Index (May): 95.3 vs.

96.0 forecast, 95.9 prior

ADP Employment Change Weekly: 29K vs. prior week 35.75K

Trade Gap (Apr): -$55.90B vs. -$56.1B forecast, -$60.3B prior

Later today: Redbook same-store sales, existing home sales for May, Treasury auctions (6-week, 1-year, 3-year)

**Bond Pricing**

**UMBS 30 yr**

| Coupon | Price | Intra-Day Change |

**GNMA 30 yr**

| Coupon | Price | Intra-Day Change |

**Treasuries**

| Term | Yield | Price | Intra-Day Yield Change |

**UMBS 30yr**

| Coupon | Price | Intra-Day Change |

|—:|—:|—:|

| 5.0 | 97.65 | 0.05 |

| 5.5 | 99.88 | -0.06 |

| 6.0 | 101.77 | -0.11 |

**GNMA 30yr**

| Coupon | Price | Intra-Day Change |

|—:|—:|—:|

| 5.0 | 98.26 | 0.11 |

| 5.5 | 100.38 | 0.07 |

| 6.0 | 101.73 | 0.1 |

**Treasuries**

| Term | Yield | Price | Intra-Day Yield Change |

|—|—:|—:|—:|

| 2yr | 4.135 | 99.506 | -0.023 |

| 3yr | 4.19 | 98.073 | -0.027 |

| 5yr | 4.266 | 98.256 | -0.026 |

| 7yr | 4.398 | 99.115 | -0.026 |

| 10yr | 4.54 | 96.695 | -0.024 |

| 30yr | 5.017 | 95.882 | -0.02 |

Stay informed and subscribe free at WellThatMakesSense.com.