**WTMS Blog Today = What’s up in Mortgage Today (AM) – 06/18/2026**

Trump’s Iran deal signature late Wednesday sparked an overnight bond rally that mortgage originators are watching closely, as UMBS securities climbed back into positive territory by mid-morning trading.

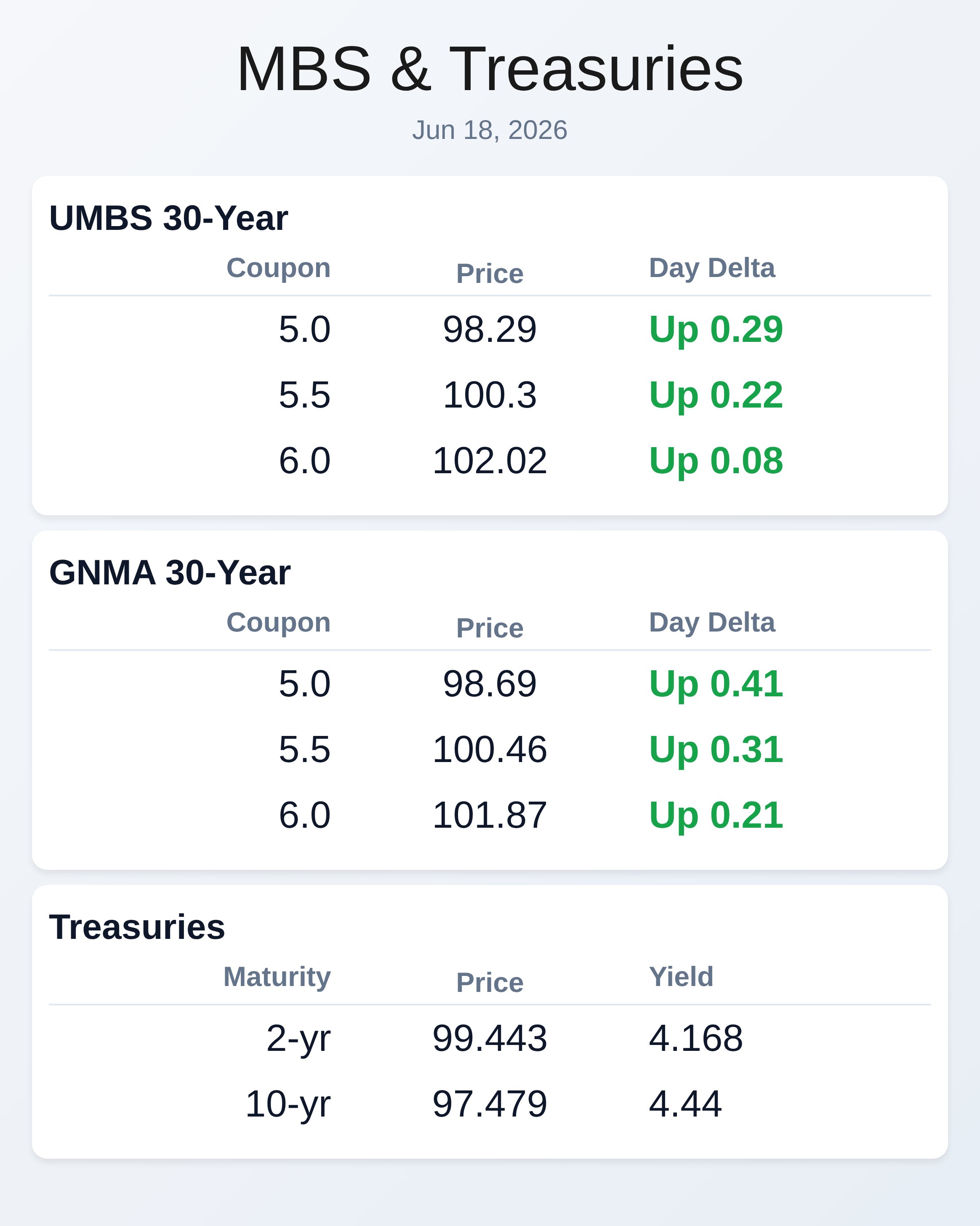

The 10-year Treasury yield dipped to 4.44 percent—down 5 basis points from Wednesday’s close at 4.49 percent—providing temporary relief after Tuesday’s post-Warsh sell-off rattled the MBS market. GNMA 5.0 securities outperformed UMBS, rising 41 basis points to 98.69, signaling continued demand for government-backed pools. Federal Reserve Chair Kevin Warsh’s debut meeting sent mixed signals: he held rates steady at 3.5-3.75 percent but signaled the central bank remains laser-focused on inflation without committing to a rate path.

Bond traders are now pricing in a 25-basis-point rate hike as soon as October, reflecting Warsh’s hawkish inflation rhetoric. Jobless claims came in at 226,000—exactly in line with forecasts—while continuing claims ticked up slightly to 1.81 million, suggesting the labor market remains steady but not accelerating. The Philadelphia Fed’s June manufacturing index surprised to the upside at 10.3 versus forecasts of 10.0, but prices paid surged to 53.20, marking a significant jump in inflationary pressure at the regional level.

These economic readings keep the Fed’s attention on inflation rather than employment, reinforcing Warsh’s message that rate cuts are off the table. For mortgage sellers, a data-dependent Fed means every CPI print and jobs report will swing Treasury yields and MBS valuations sharply. Markets are closed tomorrow in observance of Juneteenth, removing a full trading day from the week.

Geopolitical de-escalation in the Middle East—the US-Iran memorandum of understanding restores Strait of Hormuz traffic within 30 days—is easing oil-supply anxiety and pushing crude prices lower. West Texas Intermediate slid to $75.29 per barrel on the Iran deal news, helping gasoline prices dip below $4 per gallon for the first time since March. Lower energy costs could theoretically reduce inflation pressures, but the Fed and markets are skeptical that oil alone will cool the sticky 4.2 percent inflation still running well above the 2 percent target.

Any sustained relief at the pump may provide modest tailwinds to mortgage demand if consumers feel less financial pressure at the checkout counter. Warsh’s refusal to provide forward guidance leaves traders guessing about the Fed’s next move, creating intraday volatility in MBS. Technical levels matter right now for hedging and positioning decisions, so originators should watch the 10-year yield’s 4.42 percent floor—where bonds rejected hard on Wednesday morning before recovering most losses.

The 2-year yield, however, lost more ground than longer maturities, steepening the yield curve slightly as traders price in eventual rate hikes while longer bonds rally on disinflationary hopes tied to artificial intelligence and tech productivity gains. UMBS 5.0 settled at 98.29 (up 29 basis points), while 6.0 coupons climbed to 102.02, indicating strong repricing across the coupon stack. If the 10-year breaks back above 4.50 percent, expect MBS to weaken sharply, particularly shorter-duration coupons.

Conversely, a hold below 4.45 percent keeps the overnight recovery intact.

**Locking vs Floating**

Economic data remains mixed: labor markets are holding steady (jobless claims on forecast), but regional inflation signals are flashing red (Philly Fed prices paid surged 11 percent month-over-month). Rate-hike bets have shifted from “unlikely” to “possible by fall” after Warsh’s hawkish debut, making float positioning risky for borrowers who assumed the Fed was done.

Originators should counsel rate-sensitive customers to lock sooner rather than later, as the cost to float is rising with each inflation print and each Fed speaker emphasizing inflation discipline. The Iran deal may buy two to three weeks of relative calm, but the technical rejection at 4.42 percent suggests bond market confidence remains fragile.

**Today’s Events**

Jobless Claims (Jun/13): 226K vs.

225K forecast, 229K prior

Continued Claims (Jun/06): 1,810K vs. 1,800K forecast, 1,795K prior

Philly Fed Business Index (Jun): 10.3 vs. 10.0 forecast, -0.4 prior

Philly Fed Prices Paid (Jun): 53.20 vs.

no forecast, 47.90 prior

Conference Board Leading Index (May): 0.1% MoM (released 10:00 AM)

**Bond Pricing**

**UMBS 30 yr**

| Coupon | Price | Intra-Day Change |

| 5.0 | 98.29 | 0.29 |

| 5.5 | 100.3 | 0.22 |

| 6.0 | 102.02 | 0.08 |

**GNMA 30 yr**

| Coupon | Price | Intra-Day Change |

**Treasuries**

| Term | Yield | Price | Intra-Day Yield Change |

**GNMA 30 yr**

| Coupon | Price | Intra-Day Change |

|—:|—:|—:|

| 5.0 | 98.69 | 0.41 |

| 5.5 | 100.46 | 0.31 |

| 6.0 | 101.87 | 0.21 |

**Treasuries**

| Term | Yield | Price | Intra-Day Yield Change |

|—|—:|—:|—:|

| 2 yr | 4.168 | 99.443 | -0.016 |

| 3 yr | 4.181 | 98.099 | -0.032 |

| 5 yr | 4.22 | 98.459 | -0.04 |

| 7 yr | 4.319 | 99.587 | -0.048 |

| 10 yr | 4.44 | 97.479 | -0.045 |

| 30 yr | 4.882 | 97.932 | -0.046 |

Subscribe free to receive market updates each morning at WellThatMakesSense.com.