**WTMS Blog Today = What’s up in Mortgage Today (AM) – 06/17/2026**

Retail sales punched above expectations this morning, rising 0.9 percent in May versus a forecast of 0.5 percent, signaling consumer resilience that could complicate the Fed’s rate-cutting narrative. The control group—a key inflation measure stripped of autos and gas—also beat estimates at 0.7 percent versus 0.4 percent expected. This stronger-than-anticipated demand data arrives on a critical day: the Federal Reserve’s first policy decision under new Chair Kevin Warsh, whose communication style and stance on inflation could reshape market expectations for the remainder of 2026.

Treasuries are already pricing in a more balanced or slightly hawkish Fed, with the 10-year yield holding near 4.43 percent after touching a recent floor of 4.42 percent yesterday. Warsh’s press conference this afternoon will be closely watched for clues on the future policy path and whether his approach diverges from his predecessors. MBS prices remain essentially flat on the day, with UMBS gaining modest ground while Ginnie Mae securities underperformed ahead of settlement positioning.

The 10-year Treasury is unchanged at 4.43 percent, showing investors are in a wait-and-see posture before the Fed decision. Agency MBS in the middle coupon stack tightened spreads slightly, but higher and lower coupons lagged the rally as the yield curve flattened. Oil prices fell below $80 per barrel on optimism surrounding a potential U.S.-Iran agreement to reopen the Strait of Hormuz, though broader market response has been muted as traders remain skeptical about the durability of any peace deal.

The combination of easing energy concerns and lingering geopolitical uncertainty has left rates near the lower end of their recent range. Technical resistance levels remain critical for mortgage originators deciding on rate-lock strategies. Yesterday’s test of the 4.42 percent floor on the 10-year yield sparked multiple bounces before the afternoon bounce higher, suggesting traders are cautious about pushing yields decisively below this level.

For loan officers managing pipelines, this technical resistance means borrowers with 4.57 percent lock triggers may be inclined toward more defensive positioning until the 4.42 percent level is conclusively broken. Bond market momentum—tracked through these 10-year yield ceilings and floors—helps originators understand whether recent rate moves signal broader structural shifts or are simply intraday noise. With major economic data and Fed policy decisions still ahead, tactical positioning becomes essential for managing pipeline risk.

Non-QM originations are projected to reach $150 billion to $180 billion this year, while HELOC volume grew nearly 6 percent year-over-year in Q3 2025, reflecting borrower demand for alternative products. However, point-of-sale platforms must keep pace with this product complexity, and mortgage companies are increasingly turning to dynamic app configurations that eliminate the need for custom coding or lengthy development cycles. Capital markets teams are also modernizing their hedge operations through AI-powered tools that provide real-time visibility into margin performance, reduce manual work, and improve settlement accuracy.

Servicing portfolios are evolving from back-office functions into strategic customer intelligence hubs, with firms using advanced data infrastructure to identify emerging borrower needs before they appear in traditional data sets. Lenders that invest in these operational tools and data capabilities are positioning themselves to remain competitive in an increasingly complex origination and servicing landscape. Fraud detection is becoming an essential early-stage screening tool as mortgage fraud grows more sophisticated and subtle.

New solutions that centralize fraud risk scoring and property research into user-friendly dashboards allow underwriters to investigate potential issues faster without navigating multiple vendor portals. Settlement risk is also declining as lenders improve reporting accuracy and internalize TBA trading operations, reducing back-office work and operational complexity. These infrastructure improvements—from dynamic application platforms to AI-assisted margin management to consolidated fraud monitoring—represent the operational investments that separate efficient lenders from struggling competitors.

The mortgage industry is shifting from manual, disconnected processes toward integrated, intelligent workflows that deliver faster decisions and lower operational costs. Today’s calendar brings several data releases and events that could move rates further: mortgage applications data has already come in down 3.8 percent week-over-week, April Business Inventories, May Pending Home Sales, weekly crude oil inventories, and the June Federal Open Market Committee rate decision are all scheduled. Markets are also monitoring the Strait of Hormuz reopening agreement set to be formally signed on June 19, which could reshape energy price expectations and inflation outlook over the next several quarters.

Chair Warsh’s first press conference following the Fed decision will be the most closely watched event, as traders decode whether his communication strategy mirrors his predecessors or signals a material shift in the central bank’s bias. Benchmark Treasury yields have edged 2 to 3 basis points lower while MBS prices gained roughly a quarter point, reflecting modest risk-off sentiment ahead of these catalysts. The combination of strong retail sales, technical resistance in yields, and uncertainty around Fed messaging creates a day of significant positioning decisions for mortgage originators and capital markets teams.

**Locking vs Floating**

Borrowers and originators holding 4.57 percent lock ceilings should monitor whether the 10-year yield definitively breaks below 4.42 percent before committing to floating positions. Yesterday’s technical test at 4.42 percent generated multiple bounces, signaling trader caution about pushing yields lower without confirmation. A decisive break below 4.42 percent—backed by Fed dovishness or weaker economic data—would justify floating; a retreat back above 4.50 percent would favor locking.

Today’s FOMC decision and Chair Warsh’s messaging are the primary catalysts that could break this technical standoff. Until the 10-year yield definitively resolves above or below current resistance levels, risk-management discipline suggests a cautious stance rather than aggressive floating.

**Today’s Events**

Retail Sales (May): 0.9% vs 0.5% forecast, 0.5% prior

Retail Sales Control Group MoM (May): 0.7% vs 0.4% forecast, 0.5% prior

April Business Inventories

May Pending Home Sales

Weekly Crude Oil Inventories

June Federal Open Market Committee Rate Decision

Chair Kevin Warsh Press Conference

**Bond Pricing**

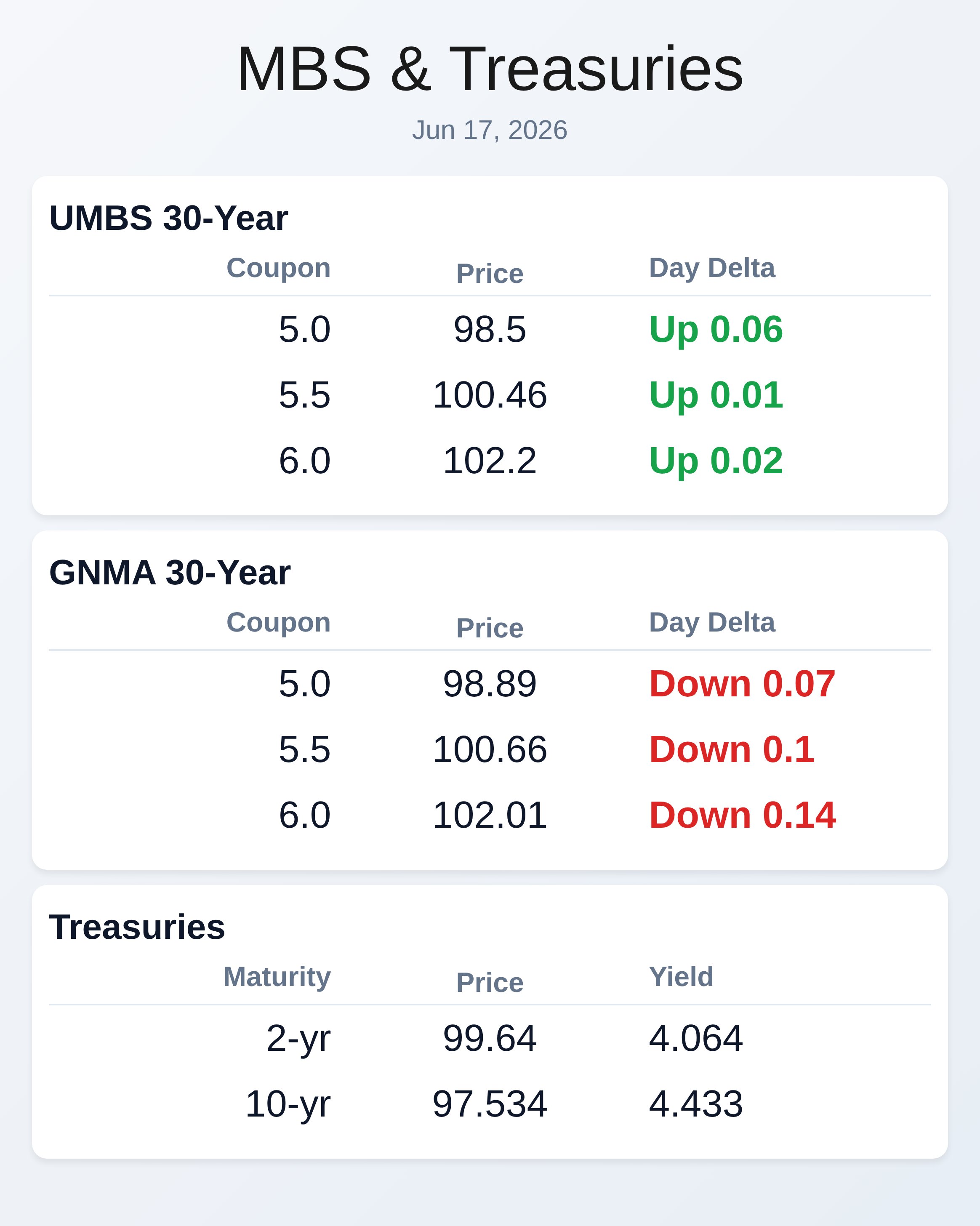

**UMBS 30 yr**

| Coupon | Price | Intra-Day Change |

| 5.0 | 98.5 | 0.06 |

| 5.5 | 100.46 | 0.01 |

| 6.0 | 102.2 | 0.02 |

**GNMA 30 yr**

| Coupon | Price | Intra-Day Change |

| 5.0 | 98.89 | -0.07 |

| 5.5 | 100.66 | -0.1 |

| 6.0 | 102.01 | -0.14 |

**Treasuries**

| Term | Yield | Price | Intra-Day Yield Change |

| 2 yr | 4.064 | 99.64 | 0.011 |

| 3 yr | 4.101 | 98.319 | 0.008 |

| 5 yr | 4.165 | 98.703 | 0.004 |

| 7 yr | 4.289 | 99.766 | -0.004 |

| 10 yr | 4.433 | 97.534 | -0.005 |

| 30 yr | 4.926 | 97.251 | -0.018 |